Most advice on how to open Emirates NBD account gets one thing wrong. It treats the process like a form-filling exercise.

That's fine if you're a straightforward UAE resident with a salary, a clean document set, and a profile the bank can verify in one pass. It's not fine if you're a founder, shareholder, consultant, free zone operator, or non-resident trying to open an account while your wider UAE setup is still taking shape.

The issue isn't whether the app works. It does. The issue is whether your profile matches the account path you've chosen, whether your documents tell one consistent story, and whether the bank can complete KYC and AML checks without having to chase you for clarifications. In 2026, that gap between marketing and reality matters more, not less. Banks are faster with clean files and stricter with ambiguous ones.

If you want a practical answer to how to open Emirates NBD account without wasting weeks on avoidable rejection points, start from the bank's perspective. Eligibility comes first. Document quality comes second. Channel choice comes third. Everything else follows from that.

Table of Contents

- Beyond the App The Realities of Opening a UAE Bank Account

- Choosing Your Account Path Personal vs Corporate vs Non-Resident

- Your Document Checklist for a First-Time Approval

- Application Channels Digital Speed vs In-Branch Clarity

- Common Rejection Reasons and How to Avoid Them

- The Inpro Advantage Streamline Your Corporate Account Opening

- Frequently Asked Questions

- Can I open an account before residency is stamped

- What is the typical initial deposit for a new corporate account

- How long does it take to receive the debit card and chequebook after approval

- Do I need a UAE mobile number to open an account online

- Can I use a personal account for company transactions

- What if my company is new and has no transaction history yet

Beyond the App The Realities of Opening a UAE Bank Account

“Open in minutes” is marketing language, not a reliable planning assumption for every applicant.

That promise can hold for a straightforward retail profile. It breaks down quickly for founders, non-residents, and applicants whose source of funds, ownership structure, or expected account activity needs closer review. In 2026, UAE banks are applying tighter onboarding checks, stronger KYC controls, and sharper transaction-risk screening at the entry stage, not only after the account is live.

The gap usually appears after the first submission. A founder may complete the form correctly and still face delays because the bank cannot classify the business clearly, verify shareholder information across documents, or reconcile the intended account use with the licence and commercial profile. A non-resident may assume the same process applies to them, then find that extra scrutiny is routine.

Why founders and non-residents get slowed down

For the bank, this is a regulated relationship first and a product signup second.

That changes how the file is reviewed. Staff are not only checking whether documents were uploaded. They are testing whether the profile makes sense as a whole. Does the licence support the stated activity? Do shareholder names match exactly across the trade licence, passport, registry extracts, and resolutions? Does the expected payment flow fit the business model? If those points are unclear, the file moves into follow-up.

I see the same mistake repeatedly. Business owners focus on the app experience and ignore the approval logic behind it.

A fast submission does not help if the bank has to ask basic questions that should have been answered upfront. That is why technically complete files still stall. The documents exist, but the story does not hold together.

Practical rule: Prepare for review as if you are presenting a compliance case, not filling out a digital form.

What improves approval odds in 2026

Banks are rewarding clarity and consistency.

The strongest files usually include a clear account purpose, matching identity and company records, current corporate documents, and a short explanation of business activity, counterparties, and source of funds. For corporate cases, it also helps when the founder can explain expected monthly volumes and why the UAE account is commercially necessary.

Weak applications tend to share the same pattern. Wrong account route. Inconsistent names or signatures. Generic business descriptions. Missing support for source of funds. Unclear links between the company, the owners, and the expected transaction profile.

This is the practical gap between the bank's consumer-facing message and the experience many founders face. Opening an account can be quick. Getting approved without delays depends on how well the application has been prepared before it reaches the bank.

Choosing Your Account Path Personal vs Corporate vs Non-Resident

Most failed applications start with the wrong choice at the start.

Emirates NBD's published campaign guidance shows that applicants must be 21+ to open an account, and the standard resident route typically requires Emirates ID, a valid passport, and proof of address. Secondary UAE market guidance also notes that for many account types, a minimum salary of about AED 5,000 is commonly required for eligibility, as noted in Emirates NBD's public account opening campaign information. That's why eligibility matters more than how polished the application form looks.

The resident personal route

This path suits employees and residents whose income and status are easy to verify locally.

If you're opening a current, salary, or savings account for personal use, the bank usually wants a standard resident profile. The strongest fit is someone living in the UAE with local identification, stable address proof, and income evidence that matches the intended account use.

This route is efficient when your salary is the primary source of funds and there's no need to explain business ownership, foreign counterparties, or multi-jurisdiction income.

The corporate route

A corporate account is the right route when the account is for a licensed UAE business. That includes free zone entities, mainland companies, and structures with multiple shareholders or authorised signatories.

This isn't a personal account with business activity running through it. The bank will usually look deeper into the company itself, not just the applicant. It may ask for licence documents, incorporation records, ownership information, and authority documents showing who can open and operate the account.

A founder often loses time by trying the faster personal route first, then having to restart once the bank sees the account will be used for company activity.

The non-resident route

Yet, public advice is usually too simplistic.

Non-residents face a different onboarding reality. The account may still be possible, but the review is stricter, the supporting papers are broader, and the bank often wants more comfort around identity, address, and banking history. If you don't hold a UAE resident profile yet, don't assume the app-based resident flow applies to you.

Here's the practical comparison.

| Attribute | Personal Account (Resident) | Corporate Account (Resident) | Non-Resident Account |

|---|---|---|---|

| Best fit | Salaried UAE resident | UAE-licensed company | Individual without UAE residency, or applicant outside standard resident route |

| Core identity documents | Emirates ID, passport, proof of address | Company and shareholder identity documents, plus company records | Passport and expanded supporting papers, subject to review |

| Main review focus | Personal eligibility and income fit | Business activity, ownership, authority, source of funds | Identity, address outside UAE, banking background, profile risk |

| Typical use | Salary, spending, savings | Operating business funds | Limited personal banking access, subject to stricter checks |

| Fastest channel | Digital if profile is simple | Usually assisted, often with branch or relationship manager input | Often benefits from direct clarification and full pre-check |

| Common mistake | Applying without proving salary fit | Submitting licence papers without a clear operating story | Using a resident-style checklist |

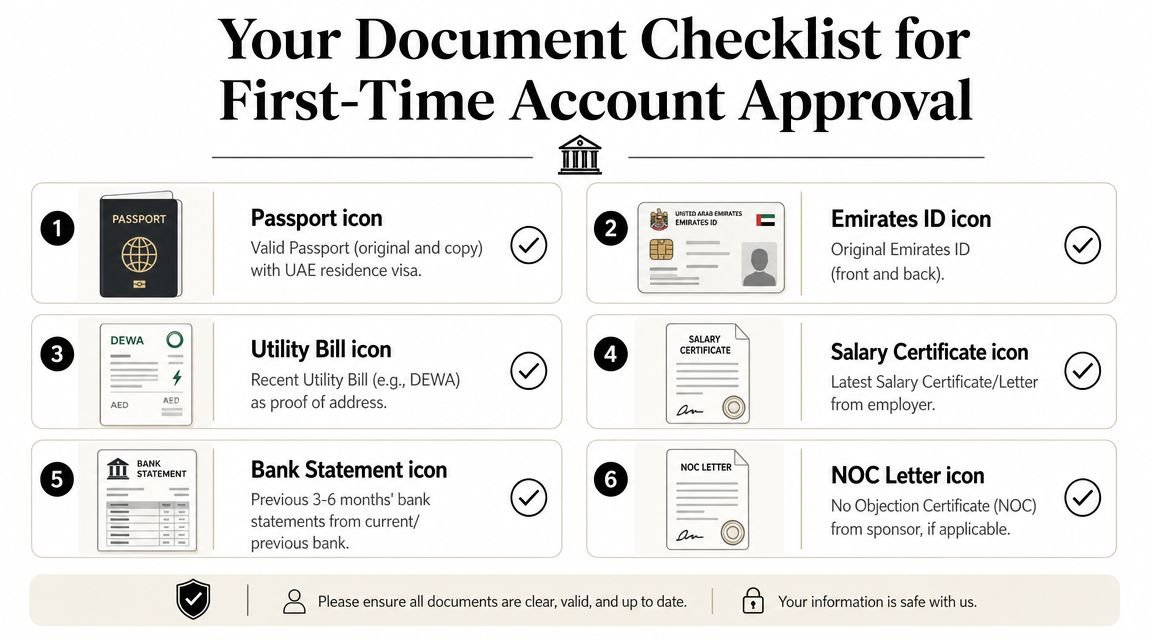

Your Document Checklist for a First-Time Approval

First-time approval usually comes down to file quality, not intent. A bank officer can work with a straightforward profile. They will slow down or reject a file that leaves gaps around identity, address, income, ownership, or authority.

For a standard UAE resident application, the core pack is simple enough on paper. In practice, approval depends on whether each document supports the same story. That is the gap many applicants miss, especially founders who have seen the bank's fast onboarding marketing and assume the review will stay equally simple once a real compliance check starts.

What the bank needs for a standard resident file

A clean resident file usually includes four document groups:

- Passport: Submit a valid copy with the same spelling, sequence of names, and nationality details used across the application.

- Emirates ID: Provide a current, clear copy on both sides. If renewal is in process, expect follow-up questions.

- Proof of address: Use a recent document that clearly matches the address you entered on the form.

- Income support: If the account will receive salary, business income, or regular transfers, include documents that make the source of funds easy to verify.

That last point matters more in 2026 than many applicants expect. UAE banks are applying sharper source-of-funds checks, especially where the profile includes self-employment, foreign income, multiple jurisdictions, or shareholder ties to a business account.

The infographic below captures the right approach. Build a file that answers the compliance review before the reviewer has to ask.

What founders usually miss

Founders and non-resident applicants often submit documents that are individually valid but collectively weak. That is enough to trigger delays.

For business-related reviews, the bank may ask for trade licence copies, incorporation records, shareholder registers, and signatory authority documents. The real test is consistency. Business activity, ownership percentages, signing authority, and expected account use must line up across every page.

The rejection points I see most often are predictable:

- Expired or stale records: Old Emirates IDs, previous address documents, expired licences, or outdated shareholder records.

- Name mismatch: Different spellings or name order across passport, visa, licence, utility bill, and application form.

- Missing authority: No board resolution, no POA where needed, or no clear proof that the applicant can act for the company.

- Weak funds trail: Real income, but no clean paper trail showing how money is earned, paid, and transferred.

- Activity mismatch: A licence says one thing, invoices and website say another, and the stated account purpose sits somewhere in between.

A stronger file is usually shorter than a messy one.

For first-time applicants, I advise preparing the minimum core documents plus targeted support for any obvious risk point. If you are a founder, that may mean adding a short ownership chart, a recent invoice, a tenancy document, or a bank statement that confirms normal activity. If you are a non-resident, it often means giving more comfort on overseas address history and banking background from day one.

Submit the documents the bank expects, then add only the records that close a real compliance gap. That approach gets faster decisions than uploading a large but unfocused file.

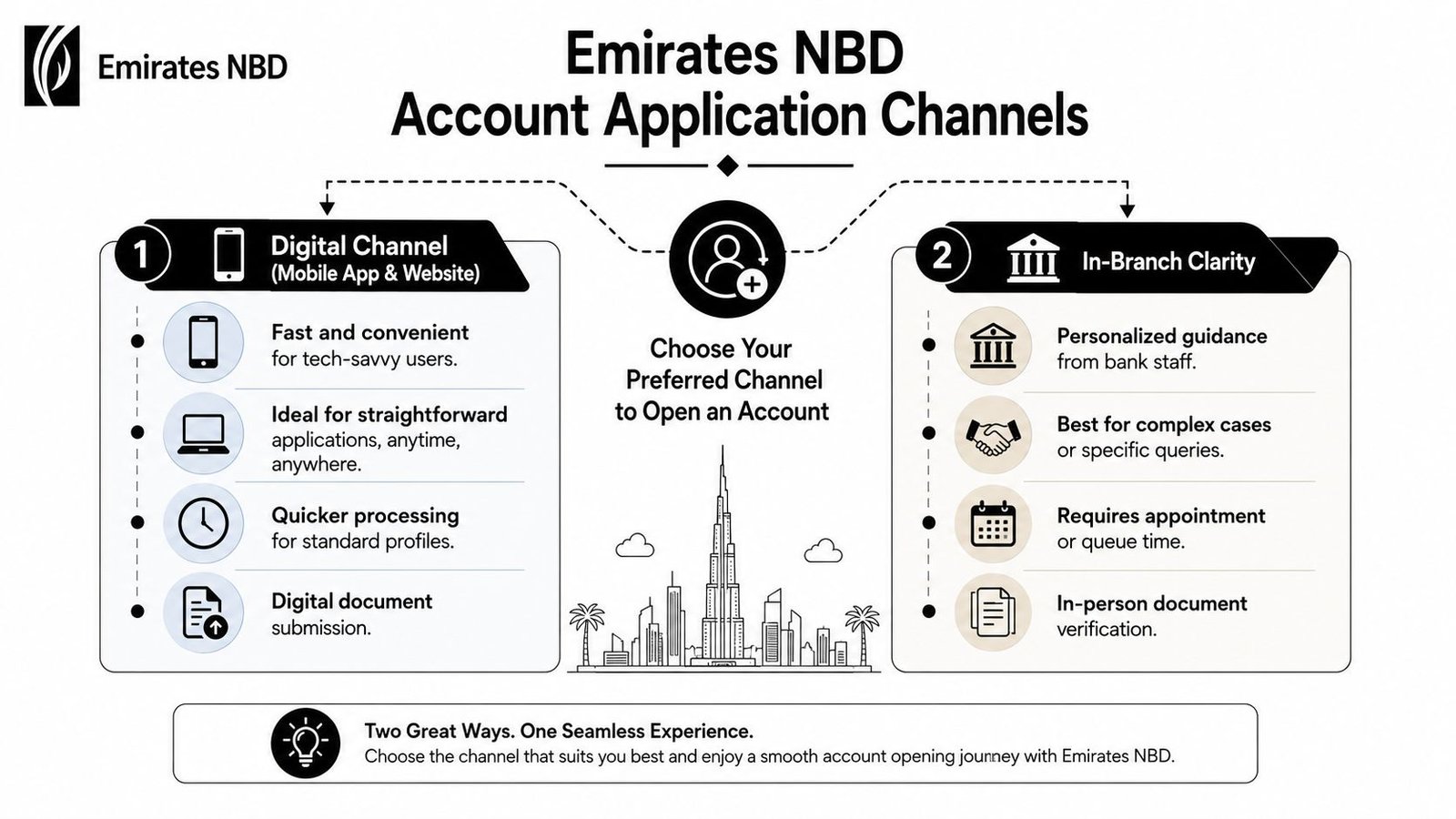

Application Channels Digital Speed vs In-Branch Clarity

The right channel depends on your profile, not your preference.

Digital application is efficient when the bank can verify you with standard resident documents and a simple account purpose. Branch interaction is often better when the profile involves shareholders, company activity, foreign address history, or any fact pattern that needs explanation.

When digital works best

If you're a standard UAE resident, digital usually gives you the cleanest path. You move faster, upload documents directly, and avoid branch scheduling.

This route works best when:

- Your profile is local and simple: Resident status, salary-backed use, no unusual ownership links.

- Your documents are already aligned: No mismatched names, no pending updates, no missing address support.

- Your purpose is obvious: Personal current, salary, or savings use.

The attraction of digital isn't just convenience. It reduces conversation points. When the file is simple, fewer human handoffs usually means fewer chances for confusion.

When branch conversations save time

A more complex file often benefits from being explained properly at the start.

External UAE market guidance notes that residents typically need to be 21+ for standard account opening, while some account types accept 18+. The same guidance also notes stricter onboarding for non-residents, including higher minimum balance expectations and additional documents such as home-country proof of address and a bank reference letter. It also points out that while same-day opening is the target for eligible applicants, activation can still take 1–3 business days when validation or review is pending, according to this UAE market guide on Emirates NBD account opening.

That's why branch support can be useful for:

- Corporate applicants: Someone needs to explain the business, ownership, and expected transactions clearly.

- Non-residents: A live discussion helps clarify what extra documents are likely to be requested.

- Edge cases: Freelancers, founders without regular salary slips, and applicants mid-transition into residency.

A branch visit isn't automatically slower. For some profiles, it prevents a digital stall that would have taken longer to unwind.

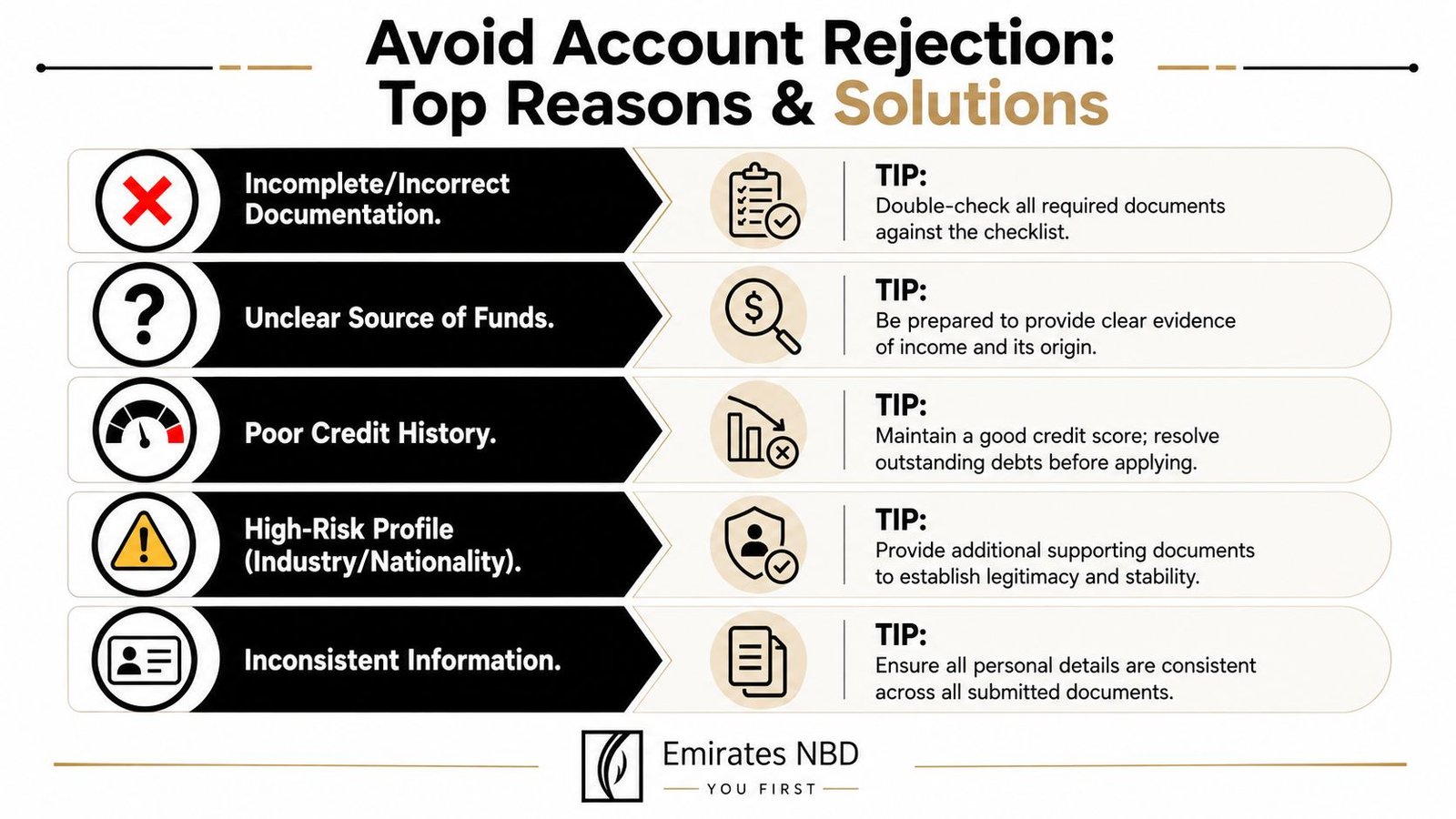

Common Rejection Reasons and How to Avoid Them

Banks rarely reject a file because the applicant filled in one field badly. They reject because the risk picture is incomplete.

For non-standard profiles, that means KYC and AML questions start early. Emirates NBD's document guidance says requirements depend on whether the applicant is an individual, joint applicant, non-individual, or company, and that additional documents may be required under KYC and AML checks, as stated in Emirates NBD's document requirements guidance. That single point explains a lot of confusion in the market. People search for one universal checklist when the bank is sorting applicants into risk and entity categories.

KYC gaps and mismatched records

The most common practical problem is inconsistency.

A passport says one thing. The licence says another. The address on one document doesn't match the address on the form. The shareholder list is technically right but not presented in a way that makes beneficial ownership obvious. None of these issues look dramatic to the applicant. To the bank, they create work and uncertainty.

Fix them before submission:

- Standardise names: Use one spelling everywhere, including initials and middle names.

- Align addresses: If your address has changed, update supporting records before you apply.

- Clarify ownership: Present shareholder and signatory authority cleanly.

- Prepare source-of-funds support: Don't wait to be asked if your income structure is not obvious.

If an underwriter has to guess what your company does or who controls it, your file is already weaker than it should be.

Risk signals for non-residents and founders

Non-resident onboarding has its own friction. The presence of a separate Dubai government service for Emirates NBD non-resident accounts signals that this is a distinct process, not just a resident application without an Emirates ID. That matters because many applicants still approach it with the wrong expectations.

Founders run into a different version of the same problem. A free zone company may be properly formed, but the bank still wants comfort that the business has substance. If the company has no clear operating narrative, no obvious commercial logic, or no straightforward explanation of expected incoming and outgoing funds, the application can stall.

A stronger file usually includes:

- A simple business summary: What you sell, to whom, and from where.

- Commercial coherence: Activity on the licence should match the business model.

- Document discipline: Company records and personal records should support one another.

- A realistic banking purpose: Operating account, receivables, payroll, or reserve funds. Pick your actual purpose.

The Inpro Advantage Streamline Your Corporate Account Opening

Corporate bank account opening in the UAE is slowest when founders treat it as an admin task. It moves better when someone manages it like a regulated project.

Why founders get stuck

The problem usually isn't effort. It's sequencing.

A founder forms the company, gets the licence, and assumes banking should follow automatically. Then the bank asks questions the founder didn't prepare for. Who are the beneficial owners. What is the exact source of initial funds. Why is the applicant using this entity structure. How will the company operate in practice. Which counterparties will send money. These are ordinary questions, but they delay the file if the answers arrive piecemeal.

That friction gets worse when:

- The company structure is layered: Holding entities, multiple shareholders, or overseas ownership links.

- The activity is cross-border: Revenue sources and counterparties aren't purely local.

- The founder is between statuses: Residency, address proof, or signatory arrangements are still changing.

What professional preparation changes

A specialist team improves the odds by reducing ambiguity before the file reaches the bank.

That means checking whether the company structure fits the intended account use, assembling a decision-ready document pack, and presenting the business in terms that a relationship manager and compliance team can assess quickly. It also means spotting weak points early, such as authority gaps, vague source-of-funds support, or documents that technically exist but don't answer the underlying question behind the review.

Good support doesn't “guarantee approval”. No serious adviser should say that. What it does is remove avoidable friction, sharpen the file, and keep communication with the bank organised.

For founders launching in the UAE, that's often the difference between a delayed commercial start and a cleaner operational setup from day one.

Frequently Asked Questions

Can I open an account before residency is stamped

Sometimes a non-resident path may be available, but it's a different route with stricter review. Don't assume a visit-visa or pre-residency applicant will be treated like a UAE resident. In practice, resident personal account opening is far smoother once local identification and address proof are in place.

What is the typical initial deposit for a new corporate account

Banks may discuss funding expectations during review, but there isn't a universal public figure you should rely on across every profile. The right approach is to ask for the requirement tied to your exact account type and company profile, then prepare documentary support showing where the initial funds come from.

How long does it take to receive the debit card and chequebook after approval

That varies by account type, fulfilment method, and whether the account is fully activated without pending checks. Don't plan critical payments around card or chequebook delivery until the bank confirms the account is active and the issuance process has started.

Do I need a UAE mobile number to open an account online

For digital banking in the UAE, local mobile access is commonly important because banks use it for OTPs, security messages, and account activation steps. If you're trying to complete the process remotely or before your local setup is final, check this operational detail early.

Can I use a personal account for company transactions

That's a bad idea. If the primary purpose is business banking, use the corporate route. Mixing company activity into a personal account can create compliance issues and often leads to avoidable questions later.

What if my company is new and has no transaction history yet

That doesn't automatically prevent account opening. It does mean the file has to explain the business more clearly. The bank will usually want to understand the planned activity, ownership, commercial logic, and expected source of funds with more precision.

If you're opening a company in the UAE or trying to get a business banking file accepted without repeated back-and-forth, Inpro Corporate Services L.L.C. can help you structure the process properly. Their team supports founders with company formation, documentation, compliance preparation, and corporate bank account coordination so you can approach the bank with a cleaner file and fewer avoidable delays.