The cheapest bookkeeping option in Dubai can be the most expensive finance decision a founder makes. That sounds backwards until you look at the actual cost structure. In the UAE, outsourced bookkeeping can start near AED 1,000 per month, while an in-house accountant can cost closer to AED 10,000 per month once salary, visa, and benefits are included, according to Escrow Consulting Group's Dubai pricing analysis. The gap matters, but the bigger issue is what that spend is buying.

In Dubai's post-Corporate Tax environment, accounting and bookkeeping services aren't just an admin line item. They are part of your compliance system. It's not just about finding someone to record invoices and reconcile a bank account. It's whether your finance setup can handle VAT, payroll, corporate tax support, reporting discipline, and the record-keeping standards your jurisdiction expects.

That's why founders searching for accounting and bookkeeping services Dubai need a different lens. Price still matters. But service design matters more. A low monthly fee is useless if the provider can't support filings, explain reporting gaps, or keep your records clean enough for lenders, investors, auditors, or the authorities who may ask for them.

Table of Contents

- The End of Just Bookkeeping in Dubai

- The New Financial Blueprint Scope of Services

- Jurisdictional Compliance Mainland Free Zone and Offshore

- How Accounting Services Are Priced in Dubai

- A Founder's Checklist for Choosing Your Accounting Partner

- From Setup to Scale How Inpro Supports Your Journey

The End of Just Bookkeeping in Dubai

Cheap bookkeeping is no longer a harmless cost-saving decision in Dubai. In the post-Corporate Tax environment, it is a risk decision.

Many founders still treat bookkeeping as back-office data entry that can be bought on price and reviewed only when a VAT return is due. That approach belongs to an earlier stage of the market. Today, the finance provider handling your records also influences whether your business can defend its numbers, meet filing obligations on time, and produce reports management can trust.

That is the key shift. The conversation is no longer about who can post transactions at the lowest monthly fee. It is about who can help the business maintain clean records, keep supporting documents in order, and reduce avoidable compliance exposure as the company grows.

Practical rule: If your accountant only talks about posting entries and year-end statements, you are buying a record-keeping service. If they also ask about filing calendars, payroll controls, tax support, and management reporting cadence, you are choosing a compliance partner.

Small weaknesses in the books rarely stay small. A missing invoice becomes a VAT issue. Weak payroll records create salary reconciliation problems. Late bank reconciliations delay management accounts, and founders start making decisions from cash in the bank instead of actual performance. By the time filing season arrives, the work is no longer routine bookkeeping. It is cleanup.

I see three mistakes repeatedly:

- Buying on headline price alone: Low-fee packages often leave out reconciliations, VAT support, payroll processing, or month-end reporting.

- Waiting until a deadline is close: Tax and compliance problems usually start months earlier with incomplete records and poor document control.

- Separating finance from operations: Invoicing, collections, expense approvals, payroll inputs, and tax readiness are connected in practice.

The better buying question is not, "What does bookkeeping cost?" It is, "What level of finance support reduces compliance risk without forcing us to build a full in-house team too early?"

For many SMEs in Dubai, that is why outsourced accounting now works best as a risk-management choice, not just an operational expense. The right provider gives the business more than posted entries. It gives structure, accountability, and cleaner decision-making.

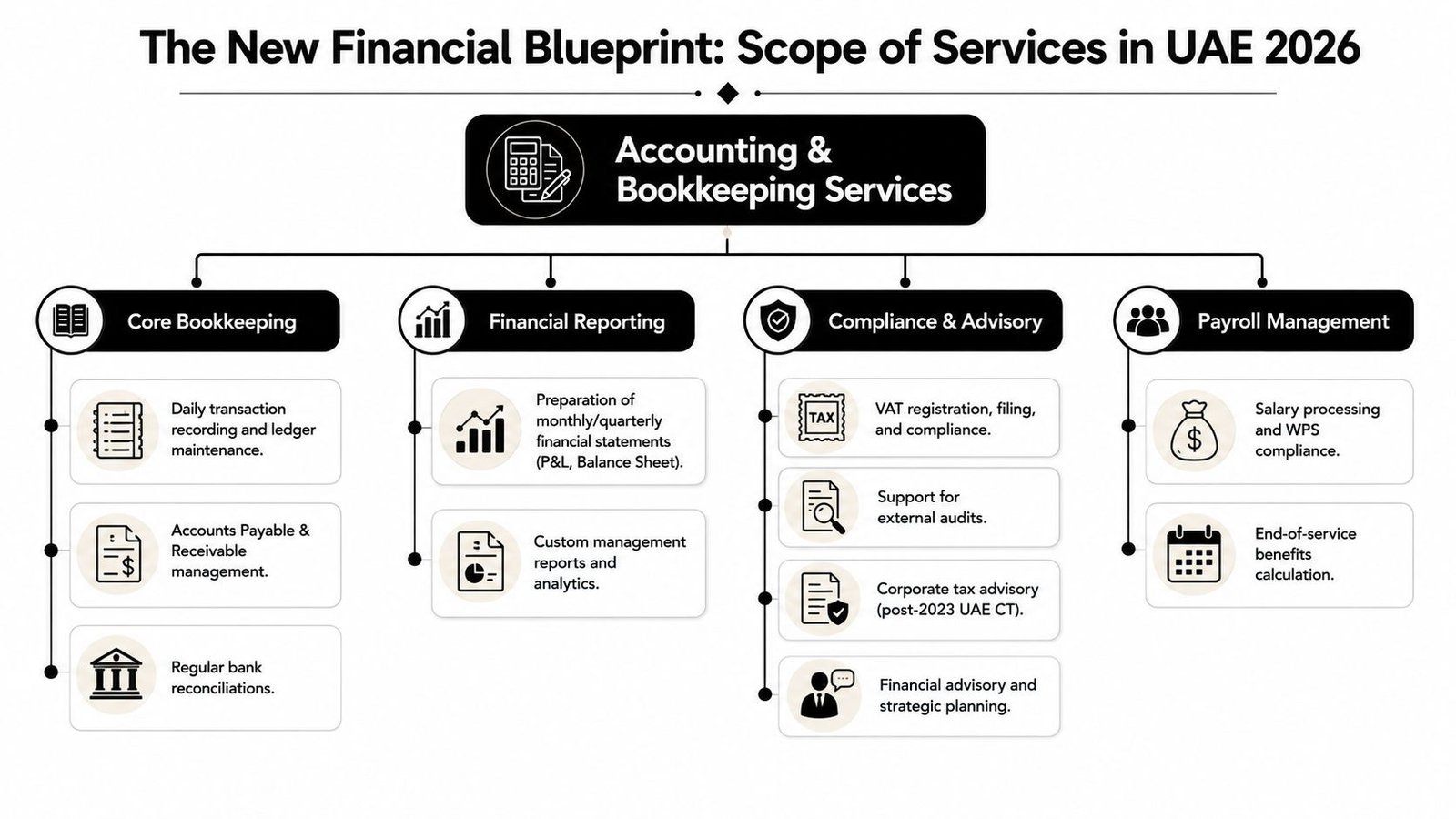

The New Financial Blueprint Scope of Services

Dubai bookkeeping on its own is no longer enough. Founders now need a finance function that can keep records clean, support tax positions, run payroll accurately, and produce reporting that stands up to scrutiny. The buying decision is no longer about who can post entries at the lowest monthly fee. It is about who can reduce compliance risk while giving management reliable numbers.

Bookkeeping is the base layer

Bookkeeping handles the raw financial record. Sales invoices, supplier bills, receipts, expense claims, bank movements, and ledger coding all sit here. If this layer is weak, every service built on top of it becomes slower, more expensive, and less reliable.

The problem is not only accuracy. It is timing and control. A founder can survive a late posting or two, but repeated delays distort VAT treatment, leave receivables unresolved, and make month-end reporting hard to trust.

A workable bookkeeping scope in Dubai usually covers:

- Transaction recording: Sales, costs, payments, receipts, and journal entries are posted consistently.

- Payables and receivables tracking: Supplier balances and customer collections are monitored before they become disputes.

- Bank and ledger reconciliations: Records are matched regularly so the books reflect reality, not assumptions.

- Document organisation: Invoices, receipts, and support files are stored in a way that can be retrieved during review or filing.

VAT and payroll sit inside the control environment

Founders often treat VAT and payroll as add-ons. In practice, both test whether the accounting process is disciplined.

VAT depends on correct classification, complete records, and a clear audit trail. Payroll depends on approved inputs, accurate calculations, and consistent posting into the accounts. If either process breaks, the issue rarely stays isolated. Payroll errors affect leave balances, accruals, and staff confidence. VAT errors create rework, clarification requests, and unnecessary exposure during a review.

This is why I tell founders to examine the provider's process, not just the service list. Ask who reviews VAT coding. Ask how payroll changes are approved. Ask when reconciliations are completed relative to filing deadlines. Those answers tell you more than a package label ever will.

A provider that cannot control payroll inputs or close reconciliations on time will struggle to support tax and reporting deadlines with any consistency.

Management reporting turns finance into a decision tool

Clean books matter, but they are not the end product. Management needs reporting that explains performance in plain terms and highlights risks early enough to act.

That usually means a monthly reporting pack with a profit and loss statement, balance sheet, cash position, and supporting schedules where needed. For a trading business, inventory and supplier ageing may matter most. For a service company, utilisation, collections, and margin by client may be more useful. Good reporting is not about more pages. It is about whether the numbers answer the decisions management has to make.

True value lies in interpretation. Why are margins slipping if revenue is up? Why is cash tight if profit looks healthy? Why are receivables growing faster than sales? Those are operating questions, and a serious accounting partner should be able to answer them from the records.

A proper scope works as one system

Founders get into trouble when bookkeeping, payroll, VAT, and reporting are sold as separate tasks with no ownership between them. The handoffs create delays. Errors sit unresolved because each party assumes someone else is handling them. By quarter-end, the business is paying for cleanup instead of paying for control.

A stronger service model connects the full cycle. Transactions are recorded properly. Reconciliations are completed on schedule. VAT treatment follows the underlying records. Payroll flows into the accounts correctly. Management receives numbers that can be used with confidence.

That is the new blueprint. In Dubai's post-Corporate Tax environment, the right scope of services functions as risk management first, and bookkeeping second.

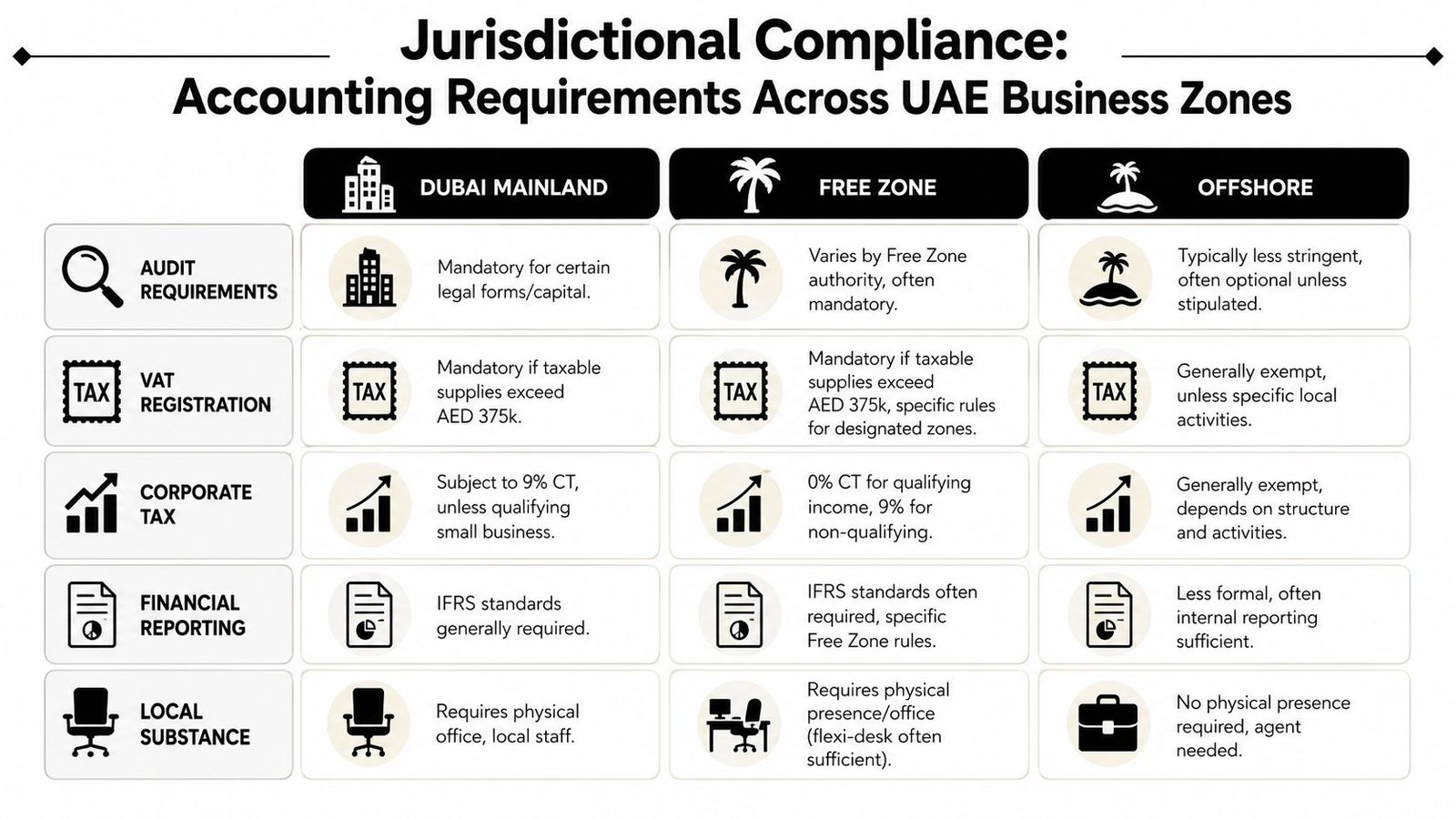

Jurisdictional Compliance Mainland Free Zone and Offshore

One of the biggest mistakes I see is founders buying the same finance package regardless of where the company sits. Mainland, Free Zone, and Offshore structures don't carry the same operating reality. The books may look similar at first glance, but the compliance expectations behind them are not.

Mainland businesses need broader operating discipline

Mainland companies usually face the widest practical compliance footprint. They're often dealing with local commercial activity, staff, supplier relationships, lease commitments, and a more active transaction profile. That means the accounting function has to support more than filings. It has to support operations.

For these businesses, weak bookkeeping tends to show up in obvious places:

- Tax support problems: Records aren't ready when VAT or corporate tax work needs to be done.

- Payroll friction: Salary processing and finance records don't match.

- Reporting gaps: Management gets delayed or inconsistent numbers.

Mainland founders should think less about the lowest-cost package and more about whether the provider can keep the finance engine organised every month.

Free Zone entities need evidence not assumptions

Free Zone founders often focus on structure at setup and underestimate record-keeping after incorporation. That's risky. If the company expects tax advantages tied to its Free Zone position, the records have to support that status in a disciplined way.

Many generic providers often fall short. They can enter transactions, but they can't explain how reporting, classification, and documentation support the company's wider compliance position.

A better operating approach for Free Zone entities includes:

- Clear revenue mapping: The company should know how income is classified internally.

- Consistent expense coding: Mixed or vague expense treatment makes later review harder.

- Monthly document control: Contracts, invoices, and bank support need to be easy to retrieve.

Free Zone accounting isn't complicated because the books are different. It's complicated because the consequences of weak evidence are different.

Offshore structures still need organised records

Offshore owners sometimes assume lighter day-to-day operating requirements mean bookkeeping can be minimal. In reality, offshore structures still benefit from clean records, especially when they're used for holdings, cross-border ownership, asset protection, or treasury functions.

The style of reporting may be simpler, but disorder still creates problems. Banks ask questions. Counterparties ask for support. Internal stakeholders want visibility. If records are reconstructed only when someone requests them, the structure becomes harder to manage than it should be.

Here's the practical comparison:

| Jurisdiction | What works | What fails |

|---|---|---|

| Mainland | Monthly close, payroll coordination, filing-ready records | Treating finance as occasional admin |

| Free Zone | Documentation discipline tied to reporting | Assuming setup structure alone solves compliance |

| Offshore | Lean but organised record-keeping | Keeping records only when requested |

The conclusion is straightforward. There is no one-size-fits-all accounting package in Dubai. The right provider should understand how your jurisdiction changes the reporting burden, the document burden, and the level of operational support your team needs.

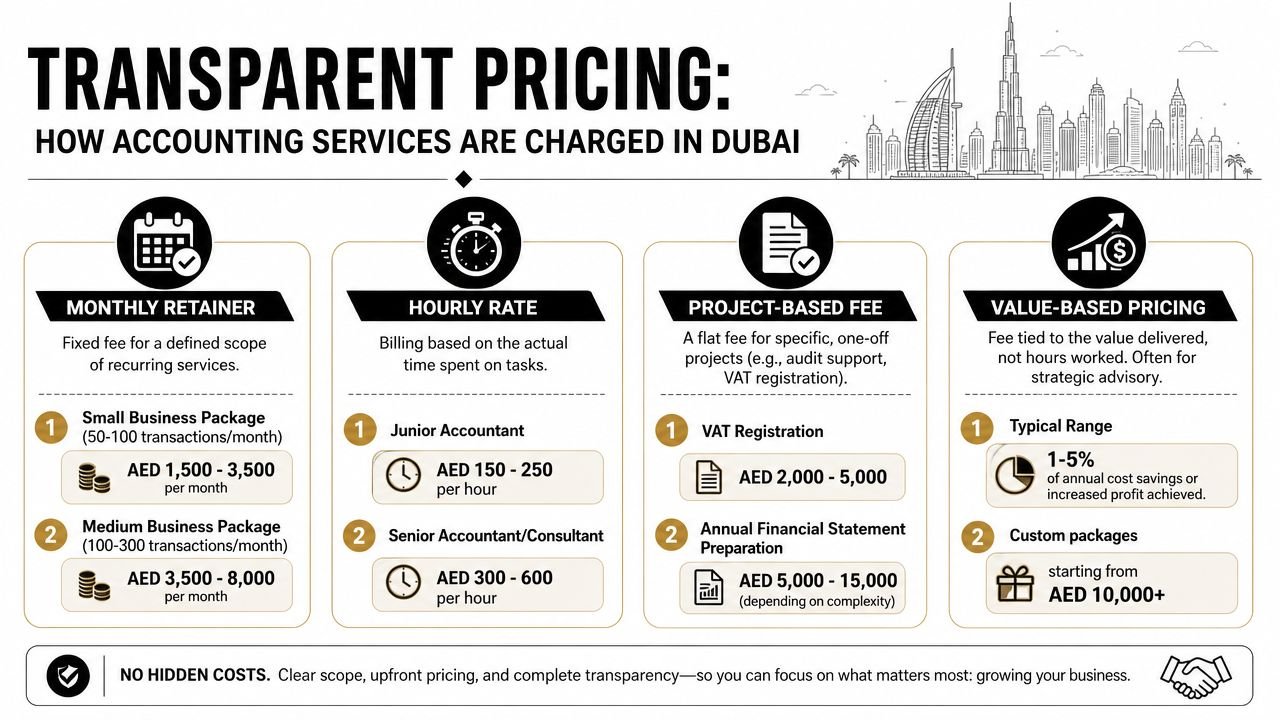

How Accounting Services Are Priced in Dubai

The cheapest accounting quote in Dubai often leaves the founder holding the risk. Pricing is rarely about data entry alone. It reflects how much compliance responsibility the provider is prepared to own, how often they review the books, and how quickly they can turn records into filing-ready outputs.

What drives the monthly fee

In Dubai, fees usually follow two structures. A monthly retainer covers recurring bookkeeping and compliance support. Hourly billing is more common for tax advice, cleanup work, system setup, or one-off reviews.

Market ranges cited by SS&CO Global's Dubai bookkeeping cost guide place smaller businesses with fewer than 50 monthly transactions at around AED 1,500 to 2,500 per month, while businesses with more than 100 transactions can fall into the AED 3,000 to 7,000 per month range. The same source notes hourly advisory rates of AED 500 to 2,500.

Those gaps reflect workload, but they also reflect exposure. More transactions create more reconciliations, more exceptions, and more chances for VAT errors, timing issues, or unsupported balances. Once Corporate Tax enters the picture, weak bookkeeping stops being an admin problem and becomes a filing problem.

Three factors usually move the fee:

- Transaction volume: More invoices, supplier payments, bank entries, and expense claims increase processing and review time.

- Compliance scope: VAT returns, payroll, corporate tax support, ESR-related recordkeeping where relevant, and audit support add technical work.

- Reporting standard: Founders who need monthly packs, cash flow visibility, margin analysis, or board-ready numbers are buying review discipline, not just posting entries.

Typical accounting service tiers in Dubai

A better way to compare providers is to look at service depth and accountability.

| Service Tier | Core Services Included | Ideal For | Estimated Monthly Cost (AED) |

|---|---|---|---|

| Basic bookkeeping | Transaction entry, bank reconciliations, ledger maintenance | Early-stage firms with light activity and limited reporting needs | Entry-level packages can start from AED 500 per month in some market guides, though many UAE providers price basic monthly support higher once scope and transaction count are defined |

| SME compliance package | Bookkeeping, monthly or periodic reporting, VAT support, routine finance coordination | SMEs that need records kept current and filing deadlines managed | Mid-range packages commonly sit between AED 1,500 and 5,000 per month |

| Outsourced finance function | Bookkeeping, VAT, corporate tax support, payroll, management reporting, advisory input, month-end oversight | Businesses with growth, multiple entities, investor reporting, or tighter control needs | Higher-touch support can reach AED 15,000+ per month, as noted in Risians Accounting's 2026 Dubai pricing guide |

The right comparison is not “bookkeeping versus accounting.” It is “data processing versus compliance support versus finance oversight.”

That distinction matters more now than it did a few years ago.

A low-fee package can work for a small business with clean activity, one bank account, limited invoices, and no serious reporting expectations. It becomes poor value the moment the provider is slow to close the books, cannot support VAT positions, or hands tax questions back to management. At that point, the business is paying less each month and carrying more risk each quarter.

Why outsourcing usually wins for SMEs

For many SMEs, outsourced support is the more disciplined choice before a full internal finance hire makes sense. Market guides often show outsourced accounting costing materially less than employing an in-house accountant once salary, visa, insurance, gratuity, and software are included.

The trade-off is straightforward. An employee gives daily proximity. An outsourced team can give broader technical coverage across bookkeeping, VAT, payroll, and tax support, but only if the scope is clearly defined and the firm has a proper review process.

What usually works:

- Outsource early with a clear scope: Buy the controls and compliance coverage the business needs now.

- Add services in stages: Expand into payroll, tax support, forecasting, or cleanup as complexity increases.

- Use advisory hours with intent: Reserve specialist time for structuring decisions, tax reviews, and problem areas.

What fails is buying a low-cost package and expecting CFO-level attention. If the business needs reliable reports, filing support, and someone to identify issues before they become penalties, the provider must be priced and structured to deliver that level of responsibility.

A Founder's Checklist for Choosing Your Accounting Partner

Choosing an accounting partner in Dubai is now a risk decision before it is a price decision. A firm that keeps records tidy but misses filing dependencies, weakens audit readiness, or responds slowly during a tax query can cost far more than its monthly fee suggests.

Sales calls rarely reveal this. Pressure does. A true test comes at month end, during a VAT review, or when management needs reliable numbers for banking, investor discussions, or corporate tax decisions. Founders should assess accounting firms as compliance partners with operating discipline, not as low-cost back-office vendors.

A useful market reference is the broader service model described by Oncount's overview of UAE accounting service design. The firms gaining traction are no longer selling data entry alone. They are combining bookkeeping, tax support, payroll coordination, reporting, and process control because those functions now affect each other.

Questions that expose weak providers quickly

Ask for operating detail, not broad assurances. Good firms can explain their process clearly. Weak firms stay general because the handoffs, review steps, and ownership lines are not properly defined.

- How do you coordinate bookkeeping, VAT, payroll, and corporate tax support? If the answer splits each item into separate silos, expect missed dependencies and slow issue resolution.

- What does your monthly close look like? Look for a clear timetable, bank and balance sheet reconciliations, review checkpoints, and a defined reporting pack.

- Which accounting stack do you use and how do documents flow into it? Cloud tools matter, but the key question is whether the provider has a disciplined method for approvals, backups, and audit trail retention.

- Who is accountable for communication and escalation? Founders need a named contact, response expectations, and a path for resolving urgent compliance issues.

- What is excluded from the monthly fee? Cleanup work, tax reviews, ESR-related support where relevant, historic reconciliations, and management reporting often sit outside the base scope.

A credible accounting partner can show how work moves from source document to filed return to management report, and who checks each stage.

A practical benchmark is the service mix offered by Inpro Corporate Services L.L.C., which combines company formation, visa support, banking assistance, accounting, and tax and VAT services under one operating model. That structure matters because founders usually feel the gap between setup decisions and finance execution months later, not on day one.

Here's a practical resource to review before shortlisting firms:

What good service design looks like

A capable provider usually shows five traits.

Jurisdiction awareness

They understand how Mainland, Free Zone, and Offshore structures affect records, reporting expectations, and the compliance questions founders are likely to face.System discipline

They use cloud accounting tools properly, keep supporting documents organised, and maintain a traceable record of transactions and adjustments.Close and review control

They close books on schedule, reconcile core balances, and identify exceptions before filings or management reviews force the issue.Decision-oriented communication

They do more than request documents. They tell management what is missing, what deadline is approaching, and what commercial decision may carry a tax or compliance effect.Capacity to scale with the business

They can support added transaction volume, staff payroll, multi-entity structures, or tighter reporting requirements without rebuilding the finance function from scratch.

Friendly communication matters. Low pricing matters too. But in accounting and bookkeeping services Dubai founders should judge the provider on process quality, review discipline, and ownership of outcomes. That is what reduces compliance risk after corporate tax, and that is what turns accounting from an admin expense into a practical layer of business protection.

From Setup to Scale How Inpro Supports Your Journey

The finance question in Dubai is no longer isolated from the setup question. Jurisdiction choice, licence scope, visa planning, bank account opening, payroll operations, and tax registration all affect how the accounting function needs to work later. Founders who separate these decisions too aggressively usually create clean paperwork at incorporation and messy operations afterwards.

That's why the most effective approach is integrated from the start. If your business is entering the UAE, the setup plan should already account for how records will be maintained, who will manage filings, how payroll will run if you hire staff, and how reporting will support management and compliance together.

A coordinated operating partner offers significant advantages. Instead of treating formation, PRO work, visas, banking, and finance as unrelated procurement decisions, founders can design them as one system. That reduces handoff problems. It also gives management a clearer view of who owns what when deadlines arrive.

The strategic point is simple. Accounting is no longer just post-fact reporting. In the UAE, it's part of how a company stays bankable, compliant, and operationally organised as it grows.

For founders moving into Dubai or expanding their UAE footprint, the right support model should help with three things:

- Launch cleanly: Set up the right structure and build finance processes early.

- Operate with control: Keep records, filings, payroll, and reporting aligned.

- Scale without rework: Add services and process depth as the company becomes more complex.

A fragmented support model can still work. It just demands stronger internal coordination. Most early-stage and cross-border founders don't have the time or the appetite for that. They need fewer moving parts, clearer ownership, and finance support designed around the UAE's real compliance environment rather than an outdated idea of bookkeeping.

If you're comparing UAE setup and finance options, Inpro Corporate Services L.L.C. can help you align company formation, visas, banking, accounting, and tax compliance into one operating plan, so you can choose a structure that fits both your market entry goals and your ongoing reporting obligations.