You can open a Dubai bank account online, but the easy version is mostly for UAE residents. If you're a resident, banks may let you apply online with three core documents and often deliver cards and credentials within 3 to 5 days after approval, while non-residents often face $10,000+ funding expectations, extra checks, and approval windows of 1 to 3 weeks.

That gap is where most advice goes wrong. In Dubai, Abu Dhabi, Sharjah, and across the wider United Arab Emirates, “online account opening” isn't one process. It's three different paths: a resident personal account, a non-resident personal account, and a corporate account tied to your company structure and risk profile.

A lot of applicants don't fail because banking in the UAE is impossible. They fail because they apply for the wrong product, submit the wrong document pack, or assume “online” means “no one will ask follow-up questions”. In practice, banks still care about residency status, source of funds, business activity, and whether your profile makes sense on paper.

Table of Contents

- Who Can Actually Open a Dubai Bank Account Online

- Opening a Personal Account as a Resident vs Non-Resident

- The Process for Opening a Corporate Bank Account

- What Are the Realistic Timelines and KYC Expectations

- Why Bank Account Applications Get Rejected and How to Avoid It

- Are There Faster Alternatives and When to Seek Expert Help

Who Can Actually Open a Dubai Bank Account Online

What are the three real pathways

There are three distinct categories. A resident personal account is for someone who already holds UAE residency and usually has an Emirates ID. A non-resident personal account is for someone outside that status, often using a savings-style product with tighter screening. A corporate account is for a UAE company and is assessed based on the business, the owners, and the company's legal setup.

Most online marketing only describes the first category. That's why people get confused when the app looks simple but the bank later asks for in-person verification, business records, or proof of UAE ties.

Practical rule: Before you choose a bank, choose the correct account type. A clean application for the wrong product still gets stuck.

Why does residency change everything

Residency is the main filter. HSBC UAE's current account eligibility says applicants must be at least 18 and hold a valid UAE residency visa for most online applications. That matters because many people searching “open a Dubai bank account online” are still waiting for their visa, Emirates ID, or local mobile number.

For non-residents, the process often starts online but doesn't end there. The practical reality is that online submission may only be the first stage, with final signing or identity checks still happening in person. That is why a new arrival and a settled resident have two different banking experiences, even if they click the same “apply now” button.

What qualifies as a corporate applicant

A corporate bank account is a bank account opened in the name of a company rather than an individual. Banks don't assess it like a personal account. They look at the company's licence, business activity, ownership chain, expected transaction pattern, and whether the business has a credible operating reason to bank in the UAE.

For founders, one factor matters more than generally anticipated: your jurisdiction. In the UAE, a Mainland company is licensed to operate in the domestic market under the relevant government licensing authority. A Free Zone company is incorporated in a special economic zone with its own authority and rules. An Offshore company is typically used for holding or international structuring and usually receives heavier scrutiny from banks.

Opening a Personal Account as a Resident vs Non-Resident

The biggest mistake I see is treating resident and non-resident banking as the same process with different paperwork. They are different products, reviewed under different risk rules, and the "online" part means something different in each case.

How does the resident route work

For a UAE resident, personal banking is usually the closest thing to a true online application. Emirates NBD account opening information states that residents can apply with a valid Emirates ID, passport, and proof of address. If those records match cleanly across the bank's checks, onboarding is often straightforward and day-to-day access is activated quickly.

The practical issue is document readiness, not app availability.

Residents get delayed for ordinary reasons. Emirates ID not yet updated in the system. Mobile number not linked properly. Address document that does not match the application. A salary transfer expectation that does not fit the account selected. These are small problems, but they are the reason many "online" applications stall.

A settled resident with active UAE documents is applying for a standard retail banking product. A person who has just landed in Dubai and is still waiting for visa completion is not in the same category, even if both are trying to open a personal account from the same website.

What changes for non-residents

Non-residents face a narrower set of options and a higher level of scrutiny. Banks often restrict product choice, ask for a larger relationship balance, and examine source of funds more closely than they do for resident current accounts. RAKBANK's non-resident account route referenced in this Dubai banking guide is one example of how minimum balance expectations can be materially higher for this category.

The online form is usually only the front end of the process. Final review may still depend on manual compliance checks, additional documents, or an in-person meeting.

For document expectations, non-resident applications commonly involve home-country bank statements, proof of income or wealth, and sometimes a bank reference. Mashreq's non-resident banking page reflects this more limited and selective route. In practice, the bank is asking a simple question: why does a person without UAE residency need a UAE account, and does the profile support that explanation?

| Applicant type | Typical route | Core friction | Common expectation |

|---|---|---|---|

| Resident individual | App or web-based onboarding | Matching Emirates ID, mobile, and address records | Faster processing once residency documents are active |

| Non-resident individual | Online enquiry or application followed by manual review | Source of funds, banking profile, and UAE rationale | More selective review, with possible in-person completion |

Online application and online approval are not the same thing. In UAE banking, digital submission often comes first and compliance sign-off comes later.

Which route makes sense for new arrivals

New arrivals waste time here more than anywhere else. If residency is still in process, many mainstream resident current accounts are still out of reach, even if the person already has a tenancy contract, employer paperwork, or a newly formed company.

The right question is status, not speed. If UAE residency is active and your Emirates ID is issued, apply as a resident. If it is not, expect to be treated as a non-resident or wait until the file qualifies for the resident route. That one distinction saves a lot of failed applications.

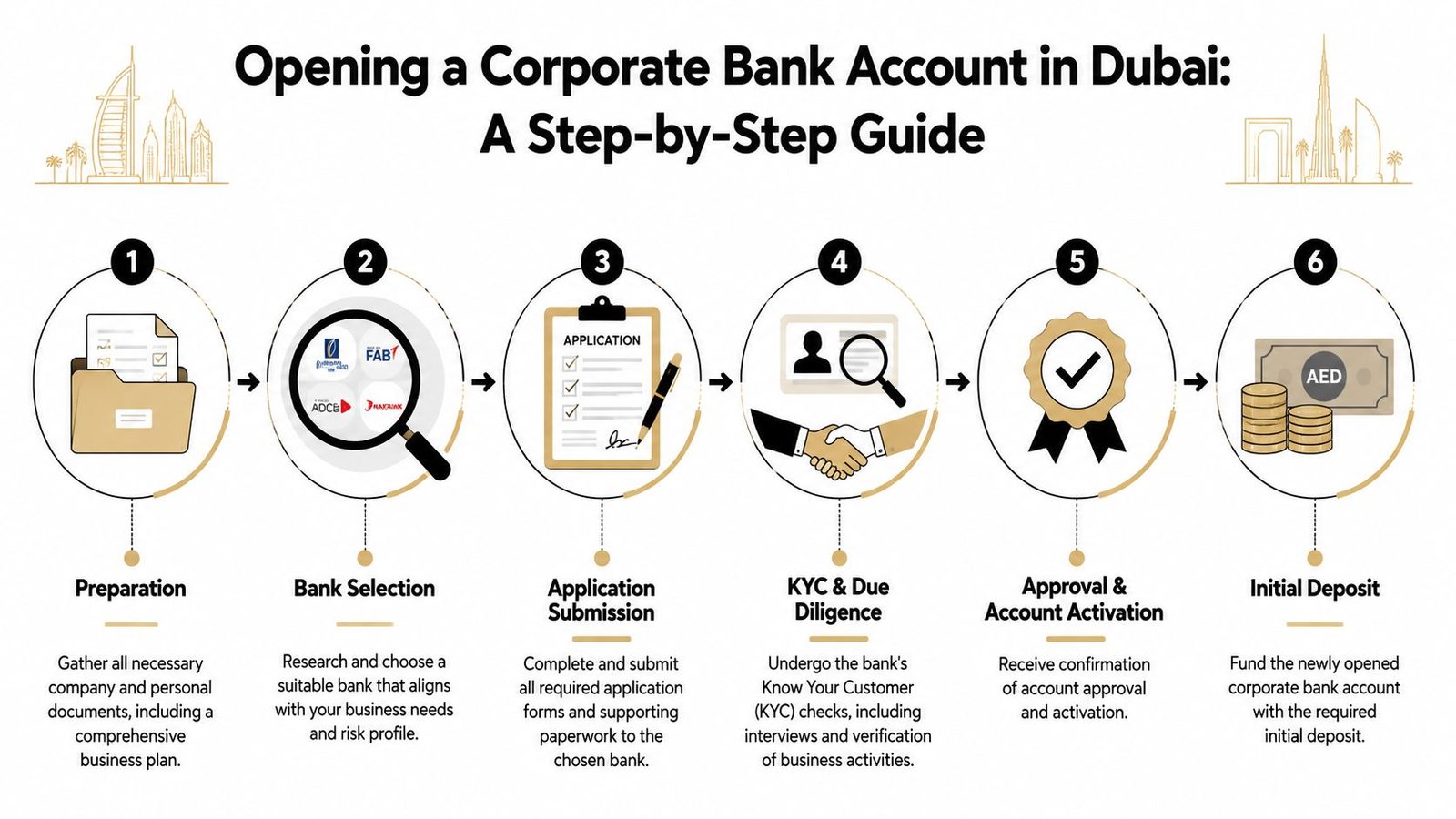

The Process for Opening a Corporate Bank Account

Corporate banking in the UAE is not a one-click product. It's a risk review wrapped around a bank application. The form is the easy part. The hard part is proving that the company, the ownership, and the expected transaction activity all make sense together.

Why is corporate banking a separate process

A corporate account is subject to Know Your Customer (KYC) and anti-money laundering review at both company and shareholder level. KYC is the bank's legal process for understanding who owns the business, what it does, where its money comes from, and how it plans to use the account.

Banks want a consistent story. If your licence says consultancy, but your projections imply high-volume goods trading, the file looks weak. If your company exists on paper but you can't explain customers, suppliers, or operational flow, the bank will pause or decline.

How does your jurisdiction affect approval

Your jurisdiction is often the strongest predictor of how smooth corporate banking will feel.

A Mainland company usually looks more straightforward to banks when it has a clear domestic trading purpose, a real office arrangement, and directors who can explain the business clearly. A Free Zone company can also bank successfully, but banks often look more closely at the actual substance of operations, especially if the company is aimed at international services, cross-border consulting, or holding activity. An Offshore company tends to receive the highest level of caution because banks usually want stronger evidence of legitimate purpose, ownership transparency, and transaction rationale.

Banks don't open accounts because a licence exists. They open accounts when the licence, ownership, and business activity form a believable operating picture.

What documents do banks usually expect

There is no single universal checklist across all banks, but the same core set appears repeatedly in real applications. For most companies, banks commonly ask for:

- Trade licence: The active UAE company licence showing the approved business activity.

- Constitutional documents: This usually includes the memorandum of association or equivalent incorporation records.

- Shareholder and signatory IDs: Passport copies, visa copies where relevant, and Emirates ID for resident parties.

- Address evidence: Office lease documents, tenancy evidence, or Free Zone facility records where applicable.

- Business profile: A short summary explaining what the company does, who it serves, and why it needs a UAE account.

- Source-of-funds support: Evidence showing where initial funding and operating income come from.

- Commercial proof: Draft contracts, invoices, client lists, supplier information, or other proof that the business is real.

The point isn't volume. It's coherence. A short, accurate file is stronger than a large folder full of unrelated attachments.

Corporate Account Document Checklist by Jurisdiction

| Document | Mainland Company | Free Zone Company | Offshore Company |

|---|---|---|---|

| Trade licence or registration proof | Usually required | Usually required | Usually required |

| Memorandum or incorporation documents | Usually required | Usually required | Usually required |

| Passport copies for shareholders and signatories | Usually required | Usually required | Usually required |

| Visa and Emirates ID where applicable | Often requested for resident parties | Often requested for resident parties | Requested if any authorised person is resident |

| Office or address evidence | Commonly expected | Commonly expected, based on facility type | Often reviewed closely |

| Business plan or company profile | Often requested | Often requested | Usually more important |

| Source-of-funds explanation | Important | Important | Usually more important |

| Proof of business activity | Helpful to strong | Helpful to strong | Often essential |

What actually works in practice

The strongest corporate applications do four things well:

- They match the licence to the story. The business activity on the licence, the bank form, and the commercial explanation all say the same thing.

- They show a believable UAE reason. That could be local clients, regional expansion, staff relocation, property ties, or operating presence.

- They explain ownership clearly. If there are multiple shareholders, nominee layers, or overseas parent companies, the structure needs to be easy to follow.

- They answer compliance questions before the bank asks them. A short source-of-funds note and a simple transaction summary can save days of back-and-forth.

A weak application usually does the opposite. It relies on generic language, hides the commercial model behind broad words like “services”, and assumes the bank will figure out the rest.

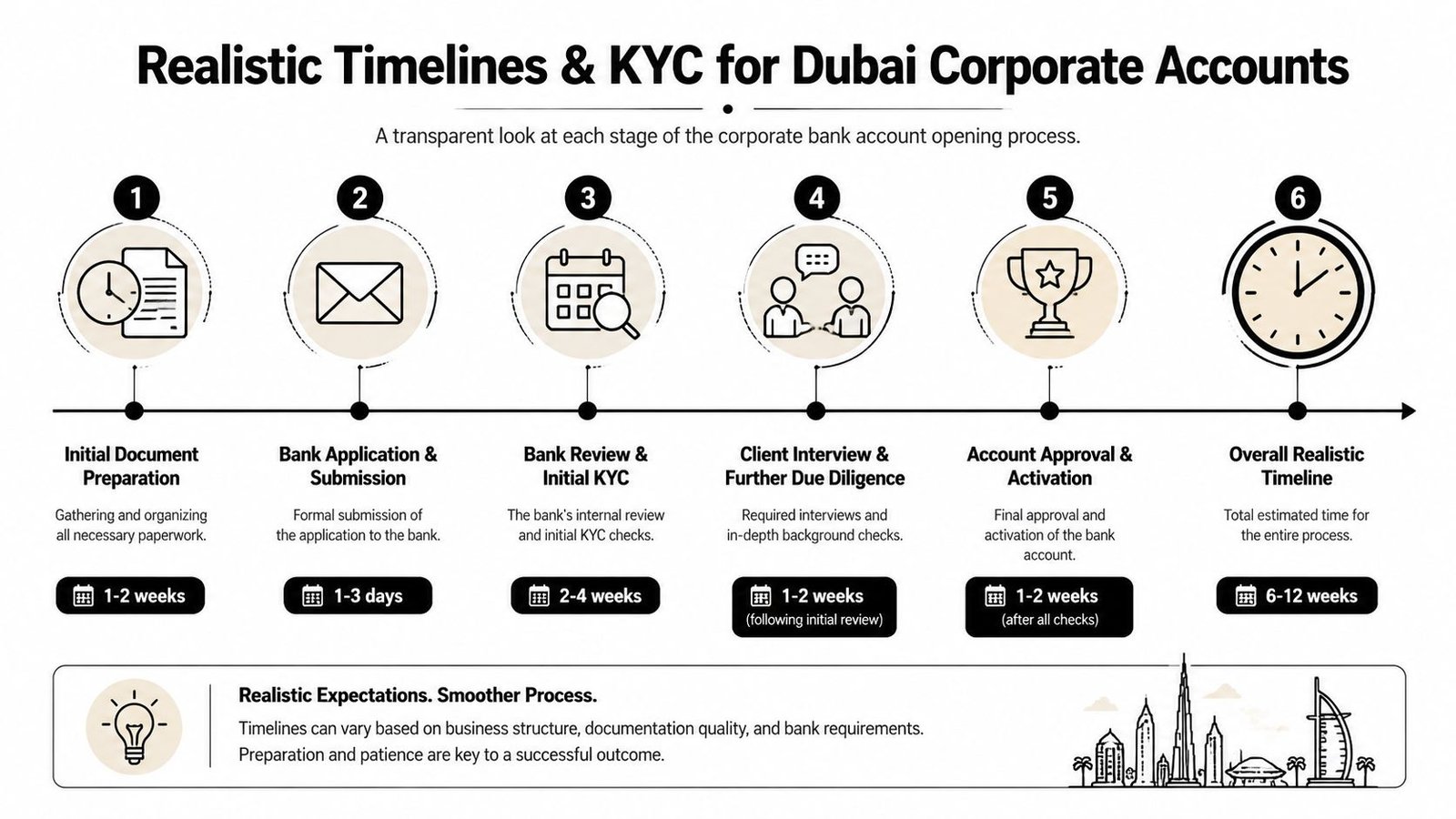

What Are the Realistic Timelines and KYC Expectations

Banks do not open Dubai accounts on your schedule. They open them when the file makes sense, the risk team is satisfied, and the applicant can answer follow-up questions without delay.

Why do some approvals take days and others take weeks

The main driver is compliance review. The app interface matters far less than the applicant type.

A resident employee with a salary transfer, Emirates ID, and a clean personal profile can move through onboarding much faster than a non-resident applying from abroad. A non-resident file usually gets extra questions about tax residency, source of income, overseas banking history, and the practical reason for needing a UAE account. Corporate files take longer again because the bank is reviewing both the people behind the company and the company itself.

In practice, the three timelines usually look different:

- Resident personal accounts: Often the fastest, if the applicant already holds a valid UAE visa and Emirates ID and can show salary or regular income.

- Non-resident personal accounts: Usually slower, with more scrutiny around account purpose, home-country banking records, and expected balance.

- Corporate accounts: Commonly the slowest, especially for newly incorporated companies, Free Zone entities without a clear operating footprint, or structures with foreign shareholders and layered ownership.

The mistake is treating all three as one process. They are not.

What banks review during KYC

KYC in the UAE is broader than identity checks. The bank wants to understand whether the account activity will match the person or business applying for it.

For personal accounts, that usually means identity, residency status, employment or business income, tax residence, and expected use of the account.

For corporate accounts, the review goes further:

- Ownership and control: Shareholders, ultimate beneficial owners, directors, and signatories all need to be clear.

- Business model: The bank needs a plain explanation of what the company sells, who pays it, and where suppliers or clients are based.

- Source of funds: This includes startup capital, shareholder injections, and the origin of the first incoming transfers.

- Jurisdiction logic: Mainland companies often have an easier commercial story than some Free Zone setups, especially if the bank cannot see a clear UAE operating reason.

- Transaction pattern: Expected monthly volume, currencies, transfer corridors, cash use, and whether the account will receive local revenue, international payments, or both.

A short, factual explanation beats a polished but vague one.

What applicants should prepare for

Banks often ask follow-up questions after the first submission. That is normal. Delays usually happen when the applicant submits basic documents but leaves the commercial story half-explained.

A realistic file should be ready to support points such as:

- why the account must be in the UAE

- where the first funds will come from

- who the main customers or counterparties are

- whether the business has staff, office space, or contracts in the UAE

- how much money is expected to move through the account in the first few months

For corporate applicants, jurisdiction matters a lot here. A Mainland trading company with local contracts is easier to place than a newly formed Free Zone consultancy with no invoices, no office evidence, and overseas shareholders who cannot explain why Dubai is the banking base.

Set timelines conservatively. Keep alternative payment arrangements in place until the account is active, funded, and tested with live transfers.

Why Bank Account Applications Get Rejected and How to Avoid It

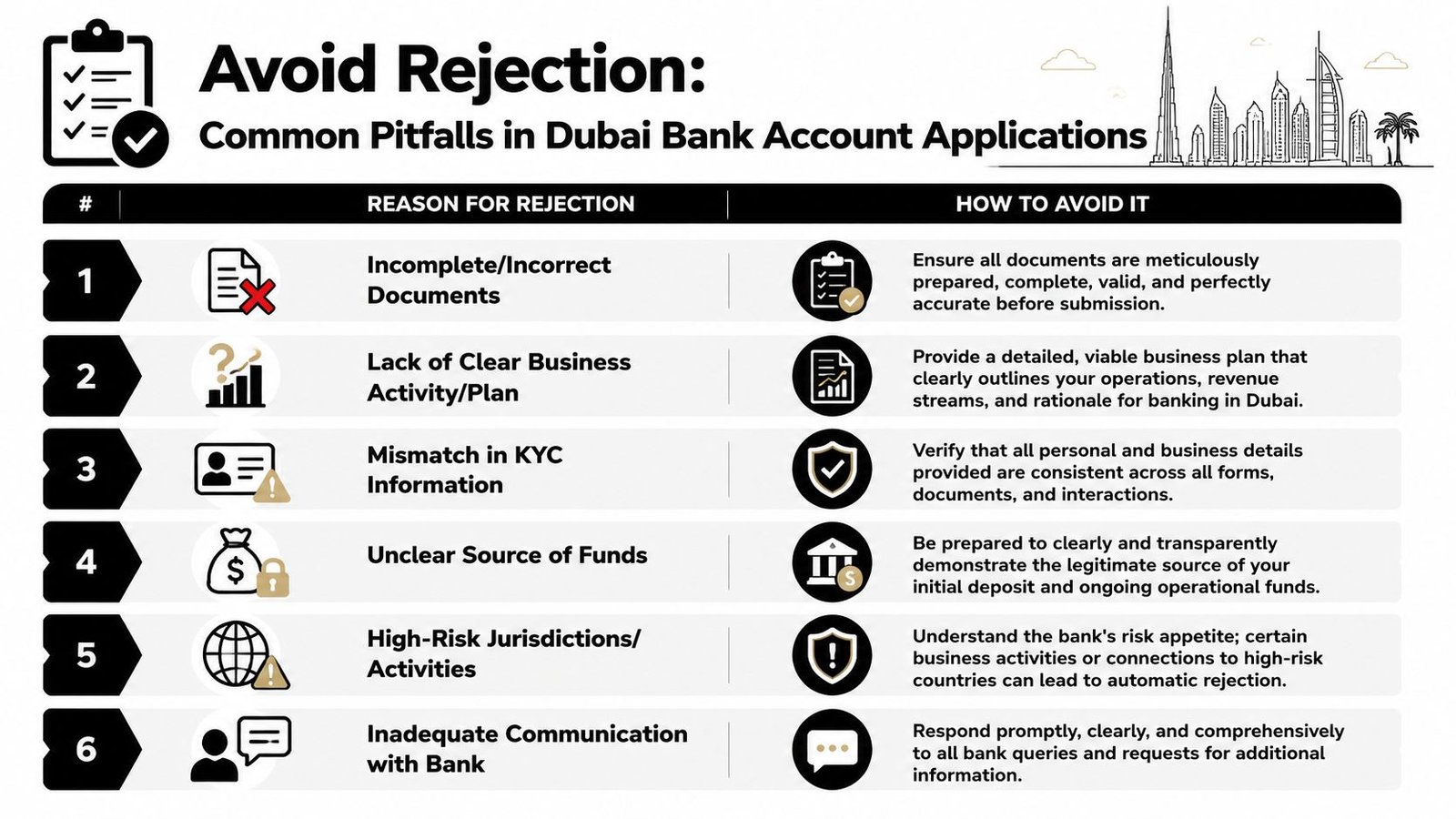

Banks rarely say “rejected” because of one small issue alone. More often, they see a file that feels incomplete, inconsistent, or commercially weak. Most failed applications show warning signs long before submission.

What usually goes wrong

These are the problems that come up most often in practice:

- Incomplete documents: A passport scan is cut off, a licence copy is outdated, or the address document doesn't match the application form.

- Weak business explanation: The company describes itself in broad terms but never shows what it sells, to whom, and how money flows.

- Mismatch across forms: The shareholder story, activity description, and expected turnover pattern don't line up consistently.

- Unclear source of funds: The founders can fund the business, but they haven't documented where the money comes from.

- Jurisdiction and activity risk: Some structures and business models receive closer review than others.

- Slow or vague replies: Banks ask follow-up questions, and the applicant answers partially or too late.

A bank officer doesn't need proof that your business will be famous. They need enough evidence that it is lawful, understandable, and properly documented.

The same principle applies to personal applicants. If a non-resident cannot show a clear wealth trail, or if a new arrival tries to force a resident product before eligibility is complete, the application can stall without ever reaching activation.

How do you reduce rejection risk before submission

The easiest way to improve your odds is to prepare for the bank's second question before you send the first form.

Try this pre-submission checklist:

- Check identity consistency: Make sure names, dates, passport numbers, and addresses match across every document.

- Write a plain business summary: One page is enough if it clearly explains services, clients, geography, payment flow, and reason for banking in the UAE.

- Map the source of funds: Show where startup capital, shareholder injections, or early revenue come from.

- Match the account type to your status: Resident, non-resident, and corporate products are not interchangeable.

- Prepare supporting commercial evidence: Contracts, invoices, property ties, or operating records help banks see substance.

- Answer fast and fully: If the bank asks for clarification, reply in one complete package instead of five partial emails.

If a bank has to reconstruct your story from scattered documents, approval gets harder.

One more point matters for founders choosing where to incorporate. A company's legal setup affects banking outcomes long after the licence is issued. People often spend weeks comparing setup costs and only a few minutes thinking about bankability. That is backwards. A licence that is cheap and fast to obtain can still create a slower, harder banking path if the structure doesn't fit the business.

Are There Faster Alternatives and When to Seek Expert Help

What can you use while waiting for a full bank account

Some founders use digital payment platforms or non-bank business accounts as an interim step while a traditional UAE bank application is under review. These can help with early collections or operational flexibility, especially for international businesses that need to receive funds before the main corporate account is active.

But these tools are not always a full substitute for a proper UAE corporate banking relationship. Many businesses still need a traditional account for day-to-day operations, local credibility, payroll handling, or broader banking services inside the United Arab Emirates. The right question isn't whether an alternative exists. It's whether it fits your actual operating model.

When is expert help worth it

If you are a straightforward UAE resident opening a personal account after your Emirates ID is active, you may not need much help. If you are a non-resident, a Golden Visa applicant waiting on status completion, a founder with multiple shareholders, or a company choosing between Mainland and Free Zone setup, expert input usually saves time because it prevents category mistakes.

This matters most for corporate files. A bank application is easier when the company was structured with banking in mind from the start. That includes the activity description, jurisdiction choice, shareholder documentation, and the business summary the bank will eventually read.

The practical lesson is simple. If you want to open a Dubai bank account online, start by asking which banking lane you belong in. That answer determines the documents, the timeline, the need for in-person steps, and the chance of approval.

Not sure where to start? Inpro Corporate Services L.L.C. helps founders, investors, and growing companies set up in the UAE, prepare the right banking file, and choose the structure that gives them the best chance of approval. Book a free strategy call if you want a clear plan before you apply.