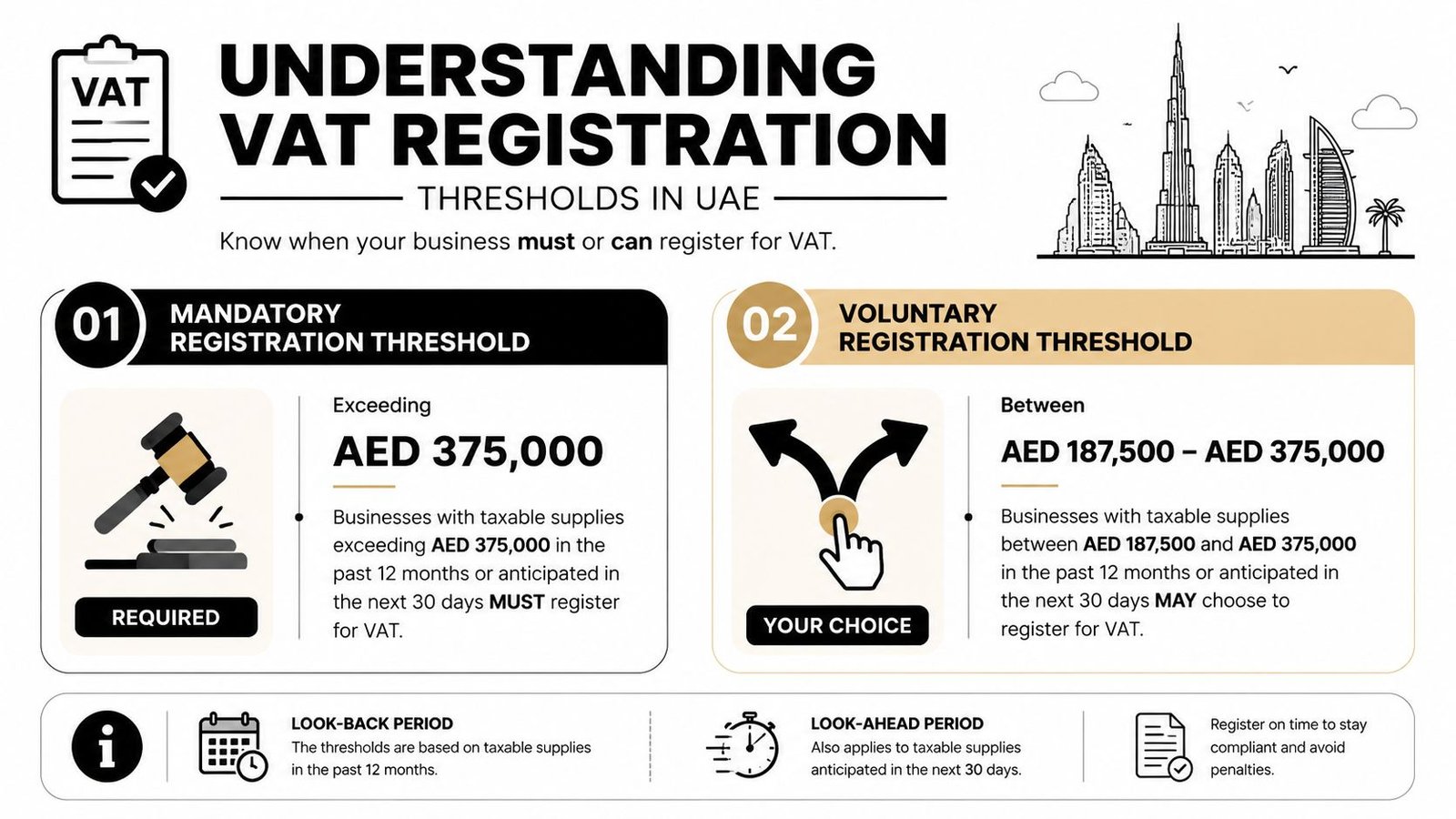

If your annual taxable turnover in the UAE is more than AED 375,000, VAT registration is mandatory. If it is between AED 187,500 and AED 375,000, you can register voluntarily, and that choice can make sense before the law forces you to do it.

That catches many founders off guard because the core question isn't only whether you've crossed the line. It's whether your business model, cost base, and sales pipeline mean you should register sooner, especially if you're building in Dubai, Abu Dhabi, Sharjah, or selling into the wider United Arab Emirates from abroad. For a young company, the VAT registration threshold UAE rules affect cash flow, pricing, invoicing, client confidence, and how much admin lands on your desk each month.

Table of Contents

- Your Guide to UAE VAT Registration

- Understanding the Core VAT Registration Thresholds

- What Counts Towards the VAT Threshold

- The Critical Timing of Your VAT Registration

- The Strategic Choice of Voluntary VAT Registration

- VAT Rules for Non-Residents and Group Companies

- Penalties for Non-Compliance and How to Deregister

- Your VAT Registration Questions Answered

Your Guide to UAE VAT Registration

VAT registration in the UAE becomes a business decision before it becomes a legal event. If you leave it too late, the result is usually the same. avoidable admin pressure, cash flow disruption, and a rushed filing setup at the exact point your business is already growing.

The Federal Tax Authority, or FTA, administers VAT in the UAE. For resident businesses, the practical starting point is straightforward. track taxable turnover against the two key thresholds, AED 187,500 and AED 375,000, and make a decision early enough to stay in control.

Founders often assume VAT only starts to matter once the company looks established on paper. In practice, I see the opposite. Digital agencies, consultants, e-commerce sellers, SaaS businesses, and solo operators can reach the threshold faster than expected because the test looks at taxable turnover, not profit, and not how much cash you keep after costs.

Practical rule: If you wait until your accountant tells you that you should have registered last month, you have already left it too late.

VAT has been part of standard UAE business operations since January 1, 2018, with a 5% standard rate applying to most goods and services. For a founder, the fundamental point is simpler than the legislation. VAT is now built into how suppliers bill, how customers assess credibility, and how finance teams manage reporting across mainland businesses and many free zone structures.

That changes the question. It is not only "Do I have to register?" It is also "When does registration help the business?" Register too late and you risk penalties and messy corrections. Register too early and you take on filing, record-keeping, and compliance work before the benefit justifies the effort.

A good VAT decision balances three things at once. legal thresholds, cash flow, and operational readiness. That is the standard founders should use throughout the rest of this guide.

Understanding the Core VAT Registration Thresholds

What is the mandatory registration threshold

AED 375,000 is the line where VAT stops being a planning question and becomes a legal obligation. If a UAE resident business exceeds AED 375,000 in taxable supplies and imports over a 12-month period, it must register for VAT. The registration deadline is 30 days from crossing that threshold.

For founders, the practical risk is simple. The threshold is based on taxable turnover, so a business can trigger registration while margins are still thin or cash collection is uneven. I see this regularly with service firms and online businesses that grow quickly on invoiced revenue but still feel early-stage internally.

VAT has applied in the UAE since January 1, 2018, with a standard rate of 5% on most goods and services. Some supplies fall under a 0% rate. The point here is not the history. Once your business crosses AED 375,000, delay creates exposure. You may need to correct invoices, account for VAT on past sales, and deal with penalties on top of the tax itself.

What is the voluntary registration threshold

AED 187,500 is the point where registration becomes a business choice. If taxable turnover is between AED 187,500 and AED 375,000, a business may register voluntarily instead of waiting until registration becomes compulsory.

Founders need judgment, not just rule-following, in such situations. Voluntary registration can make sense if the business has meaningful VAT-bearing costs and sells mainly to VAT-registered clients who expect proper tax invoices. It can also help with credibility in larger B2B deals, especially where procurement teams prefer suppliers that are already registered.

There is a cost to registering early. You take on filing deadlines, bookkeeping discipline, invoice formatting rules, and the usual admin that comes with compliance. For a lean founder-led business with light expenses and mostly end consumers as customers, early registration may add work before it adds value.

Why do these thresholds matter beyond compliance

The threshold affects more than legal timing. It shapes pricing, cash flow, and how ready the business looks to customers and partners.

A founder deciding whether to register voluntarily should usually ask three questions. Can the business recover enough input VAT to justify the admin? Will charging VAT create friction with customers or can it be passed on cleanly? Is the finance setup ready to handle returns and record-keeping without creating a monthly mess?

A simple comparison helps:

| Situation | VAT position |

|---|---|

| Above AED 375,000 | Registration is required |

| Between AED 187,500 and AED 375,000 | Registration is optional |

| Below AED 187,500 | Keep monitoring, unless special rules apply |

Good VAT timing protects compliance, preserves cash flow, and avoids adding admin before the business is ready.

What Counts Towards the VAT Threshold

What is taxable turnover

Founders often check profit, bank balance, or cash collected. The VAT threshold test looks at taxable turnover instead.

Taxable turnover is the gross value of taxable supplies and relevant imports used to assess whether VAT registration is required. It does not shrink because margins are thin, customers pay late, or operating costs are high. A business can feel tight on cash and still be over the line for VAT.

This catches growing companies more often than expected. I see it with trading businesses, agencies, and consultancies that are busy, collecting unevenly, and assuming VAT can wait until the business feels more stable.

Which supplies count and which do not

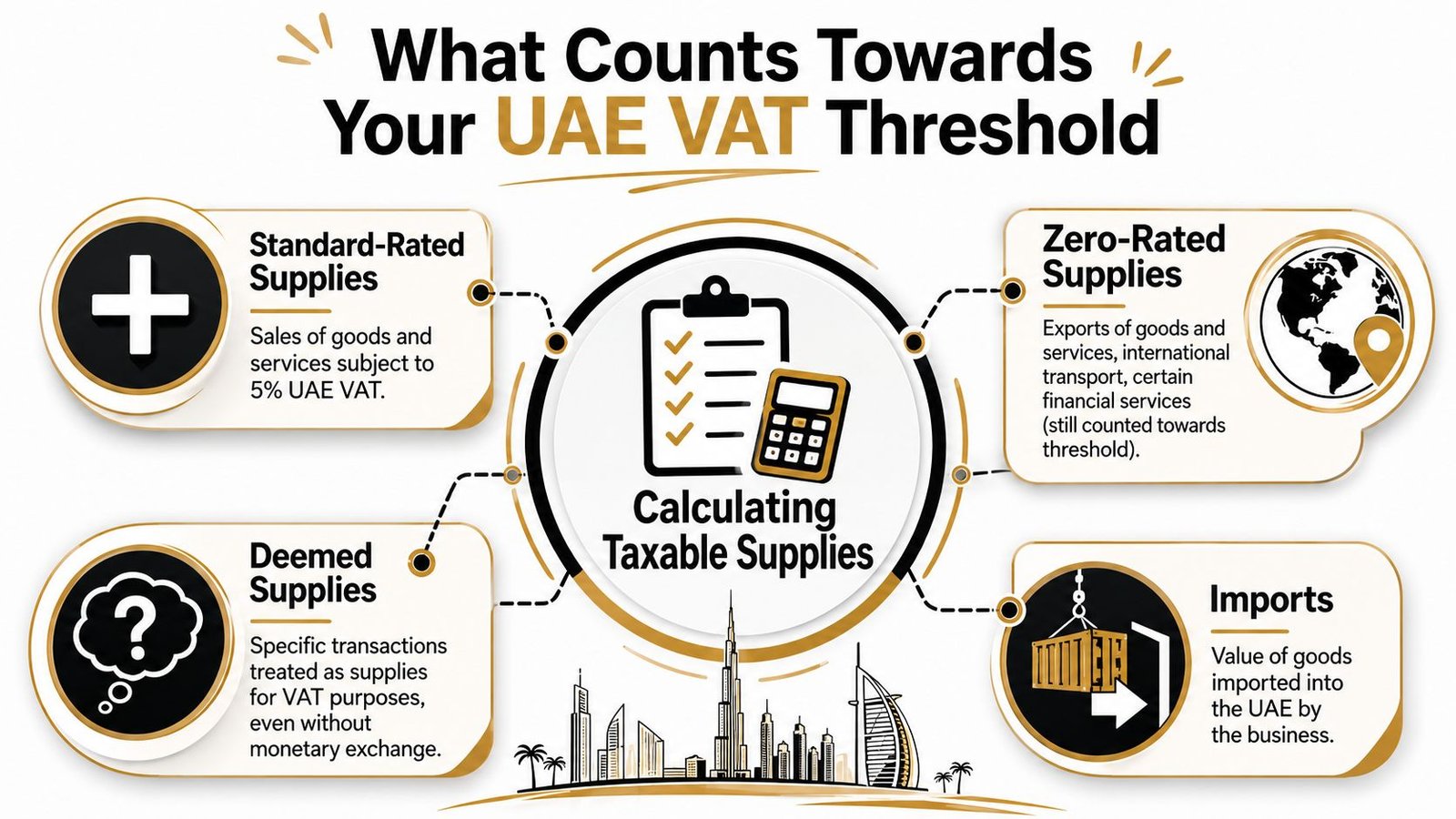

For threshold purposes, founders should separate revenue into three practical categories:

- Standard-rated supplies: Most UAE sales of goods and services fall here and generally attract 5% VAT.

- Zero-rated supplies: These are still taxable supplies, even though the VAT rate is 0%. Qualifying exports are a common example.

- Exempt income: This does not follow the same counting logic as taxable supplies and needs to be reviewed carefully.

The main point is simple. Zero-rated does not mean ignored.

A Dubai software company selling to UAE customers and also making qualifying overseas sales may reach the threshold even if part of its invoicing carries no output VAT. Founders who only monitor local 5% invoices can miss that exposure.

Exempt income is where the analysis often gets messy. If the business has a mix of exempt and taxable activity, the threshold review should be done against the actual nature of each supply, not a headline revenue figure pulled from management accounts.

How founders usually get this wrong

The mistake is usually operational, not technical. The business uses the wrong report.

A founder might review collections, the profit and loss statement, or a dashboard built for sales performance. None of those reports are designed to answer a VAT threshold question cleanly. The right review pulls out taxable supplies, checks relevant imports, and tests them at the legal entity level.

Common errors include:

- Using profit instead of turnover: Low-margin businesses can cross the threshold early.

- Leaving out imports: Imported goods and some imported services can affect the position.

- Ignoring zero-rated revenue: It can still count toward the threshold.

- Combining multiple companies informally: Separate entities are reviewed separately unless a formal VAT group applies.

There is a strategic angle here as well. If the business is nearing the threshold, the issue is not only whether registration will become mandatory. It is whether the company is ready for VAT invoices, bookkeeping discipline, and the cash flow effect of collecting tax on sales while waiting to recover input VAT on costs.

The FTA tests taxable business activity, not whether the founder feels the company is still in its early stage.

The Critical Timing of Your VAT Registration

A founder can miss VAT registration even while checking revenue every month. The reason is timing. The UAE test looks backward and forward, not only at what has already happened.

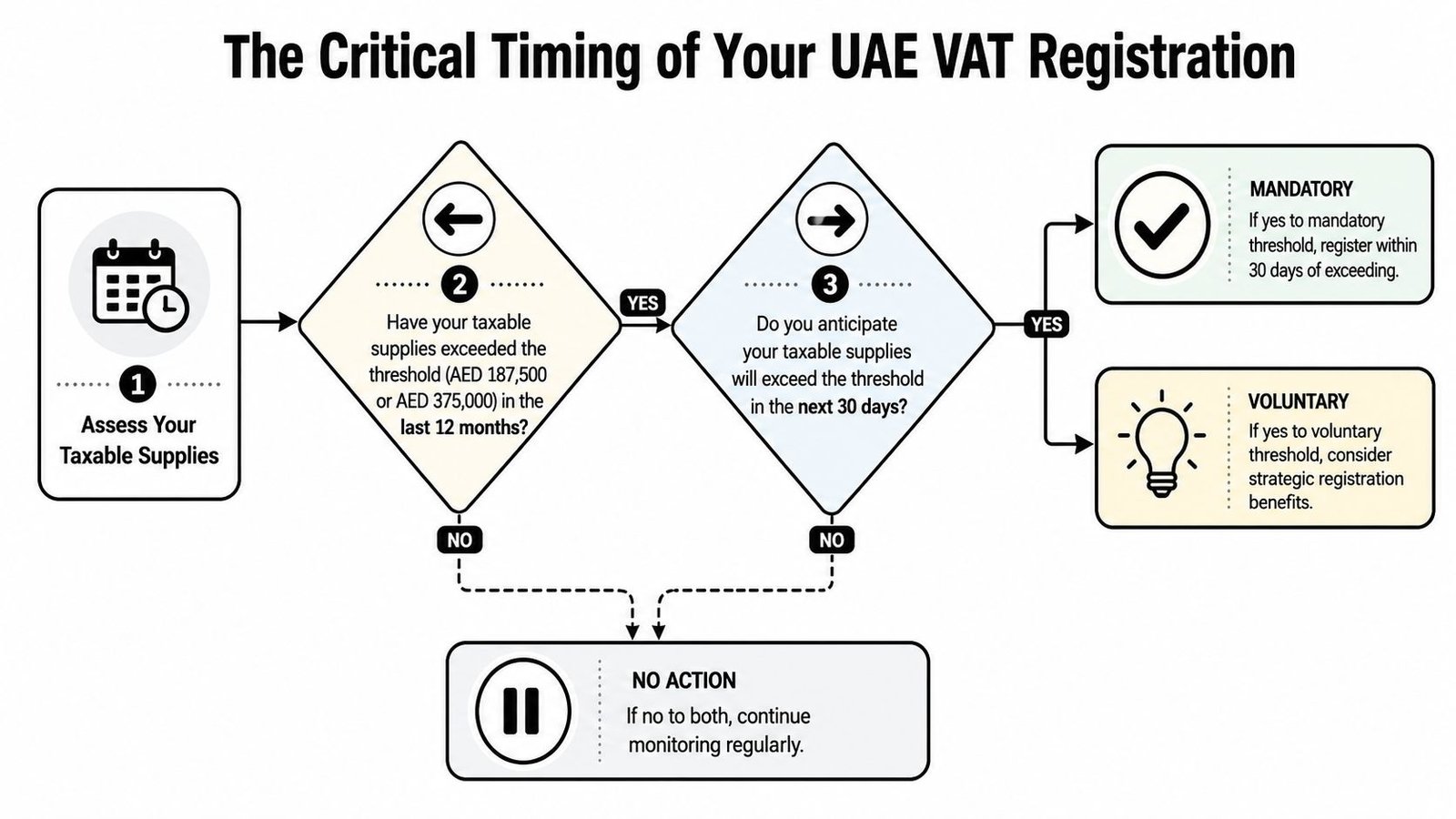

How does the 12 month test work

The first test is a rolling look-back. You review the last 12 months of taxable supplies and imports and check whether you have gone past the threshold.

This rolling approach catches businesses that grow gradually. A freelance designer in Abu Dhabi or a consultancy in Sharjah might not notice the tipping point if they only review numbers at year end.

How does the 30 day forward test work

The second test is where many founders slip. The FTA applies a 30-day look-ahead test, meaning that if your taxable supplies or imports are expected to exceed AED 375,000 in the next 30 days, you are already treated as having crossed the threshold and must register immediately, according to ClearTax's summary of UAE VAT registration rules.

That means one signed enterprise contract can change your VAT status at once. If your business runs on annual retainers, implementation projects, or prepaid subscriptions, forecasted revenue matters as much as closed historic revenue.

To see the logic in another format, this overview is useful:

What timing mistakes create problems

The pattern is usually the same. A founder wins a large client, issues a commercial invoice, and only then asks whether VAT applies. By that stage, pricing may already be locked.

Here's what works better:

- Review pipeline, not just booked revenue. If one contract is enough to tip you over, check VAT before signing.

- Set a monthly threshold review. Keep a rolling tracker for the last 12 months and the next 30 days.

- Update proposals early. If registration is likely, make sure your pricing language reflects VAT correctly.

One large deal can move you from “not yet registered” to “registration required now”. Founders who forecast sales usually avoid the messy version of VAT.

The Strategic Choice of Voluntary VAT Registration

When does voluntary registration help

Voluntary VAT registration is often a commercial decision before it becomes a tax decision.

For many early-stage UAE businesses, the essential question is not just "Can we register?" It is "Will registration put us in a better position with clients, cash flow, and internal controls?" That matters for agencies hiring locally, software companies paying VAT on tools and contractors, and founders spending heavily on office setup or launch costs before revenue is consistent.

As noted earlier, resident businesses can qualify for voluntary registration once taxable supplies or taxable expenses reach the lower registration threshold. In practice, the expense route is what catches founders' attention. A pre-revenue company with meaningful setup costs may be able to register and recover input VAT before sales ramp up, provided those costs relate to future taxable business activity.

That can help cash flow. It can also help with perception. Larger B2B clients often expect a proper tax invoice and may view VAT registration as a sign that the business is set up seriously.

When is voluntary registration a bad fit

Voluntary registration can create more friction than value if the business is still small, loosely organised, or selling mainly to end consumers.

If your customers are individuals or very small buyers who care about final price, VAT can make your offer harder to sell. Sometimes founders absorb the VAT instead of adding it on top, which protects sales but cuts margin. That trade-off needs to be priced deliberately.

Admin is the second pressure point. Once registered, the business needs proper tax invoices, organised records, and timely return filing. Founders who register early without a bookkeeper or a clean invoicing process usually regret doing it for a modest input VAT refund.

How should founders make the decision

I usually ask founders to test voluntary registration against three practical questions.

- Will the VAT recovery be material? If input VAT on setup and operating costs is small, the benefit may not justify the extra compliance work.

- What type of customer are you selling to? B2B buyers usually accept VAT as normal. Consumer-facing businesses feel the pricing impact much more directly.

- Can the business stay compliant every quarter? Registration is easier than staying compliant after approval.

A simple decision table helps:

| Business profile | Voluntary registration usually fits when |

|---|---|

| Pre-revenue startup | Setup costs are high and tied to future taxable sales |

| Service business selling B2B | Clients expect VAT invoices and the business wants to recover input VAT |

| Small consumer-facing business | Only if margins, pricing, and bookkeeping can support the extra compliance load |

The best decision is usually the one that preserves flexibility. If VAT recovery is meaningful and your clients are VAT-registered businesses, registering early can make sense. If recoverable VAT is modest and the business is still operationally messy, waiting is often the cleaner choice.

VAT Rules for Non-Residents and Group Companies

Who counts as a non-resident for UAE VAT

A non-resident business is a business that makes taxable supplies in the UAE without being established there in the normal resident sense. This catches many foreign founders who sell services remotely into Dubai or the wider United Arab Emirates and assume the local threshold protects them.

It doesn't.

What changes for foreign businesses selling into the UAE

For non-residents, the threshold rule falls away. PwC's UAE tax summary on other taxes states that non-resident businesses making taxable supplies in the UAE must register for VAT regardless of turnover, with no minimum threshold.

That means a foreign consultancy, software provider, or service business can trigger UAE VAT obligations from its first taxable supply into the market. If you are outside the UAE and contracting with UAE customers, the right question isn't "Have we reached AED 375,000?" It is "Are we making taxable supplies here, and who carries the VAT obligation?"

How should group companies think about VAT

Group structures create a different issue. If you operate through a holding company, a mainland trading entity, and a free zone service company, you should not assume one VAT answer fits all three.

In practice, founders should review:

- Entity-by-entity turnover: Each company may need its own threshold analysis.

- Intercompany charges: Management fees, recharges, and shared staff costs can affect VAT treatment.

- Operational reality: A structure that looks tidy on a corporate chart can create messy VAT flows if each company bills or incurs costs differently.

For companies established in the Dubai International Financial Centre and the Abu Dhabi Global Market, those acronyms matter for legal setup, not as an automatic shortcut around VAT. The Dubai International Financial Centre (DIFC) is a financial free zone in Dubai, and the Abu Dhabi Global Market (ADGM) is a financial free zone in Abu Dhabi. Both still need a proper VAT review based on the actual supplies made by each entity.

Penalties for Non-Compliance and How to Deregister

What happens if you register late

Late registration is expensive in the most frustrating way. It is avoidable.

Failure to meet the AED 375,000 threshold-based registration rule can result in an administrative penalty of up to AED 10,000, according to UAE guidance summarised earlier in this article. The bigger operational problem is that late registration often forces founders to revisit old invoices, client contracts, and pricing decisions after the fact.

When can a business deregister

Deregistration is the process of leaving the VAT system when the business no longer meets the conditions to stay registered. That can come up when a company closes, stops making taxable supplies, or its taxable activity falls and stays below the relevant level for registration.

The practical steps are usually straightforward in concept, even if the paperwork needs care:

- Confirm the reason: Business cessation and sustained lower taxable activity are the usual triggers.

- Clear filings first: Outstanding returns and records should be cleaned up before you apply.

- Keep evidence: The FTA may expect a clear explanation of why deregistration is appropriate.

Founders often treat deregistration as an afterthought. It should be handled with the same care as the original VAT application.

Your VAT Registration Questions Answered

Do these VAT rules apply to free zone companies

Yes, free zone companies still need a VAT analysis. A free zone licence in Dubai, Abu Dhabi, or another emirate doesn't automatically remove VAT obligations. The answer depends on what the company supplies, where its customers are, and whether its activity is taxable.

What should you do once VAT registration is approved

Start using your VAT status properly from day one. Update your invoices, check contract wording, brief your finance or operations team, and make sure sales staff know when VAT must be added to pricing. This is also the point to organise a clean filing routine instead of improvising later.

What records should you keep

Keep the documents that support your VAT position, not just your revenue total. In practice, that means sales invoices, purchase invoices, import records, contracts, and the working papers showing how you assessed taxable supplies and registration timing. If the FTA asks questions, a clear audit trail matters more than a rushed explanation.

Not sure where to start? Book a free strategy call with Inpro Corporate Services L.L.C. if you want help with UAE company setup, VAT registration, visas, and ongoing compliance.