You're usually asking about VAT registration at the same point in the business journey. Revenue is moving, suppliers are sending invoices with VAT, a larger client asks for your TRN, or your finance lead says the business may have crossed the line where registration is no longer optional.

That's the right time to get strategic. Founders often treat VAT registration as a form-filling task. It isn't. The way you register, when you register, and what structure you choose can affect cash flow, procurement, client onboarding, and how much compliance friction you create for the team later.

If you searched for how to register for VAT in UAE, the mechanics matter. But the better question is how to register correctly, with the least rework and the lowest compliance risk.

Table of Contents

- Determining Your VAT Registration Requirement

- Assembling Your VAT Registration Document Pack

- A Walkthrough of the EmaraTax Registration Portal

- Strategic Choices VAT Grouping and Voluntary Registration

- Life After Registration Your Ongoing VAT Obligations

- Common Pitfalls and When to Seek Expert Help

Determining Your VAT Registration Requirement

The first decision isn't how to fill the portal. It's whether you should be in the portal at all.

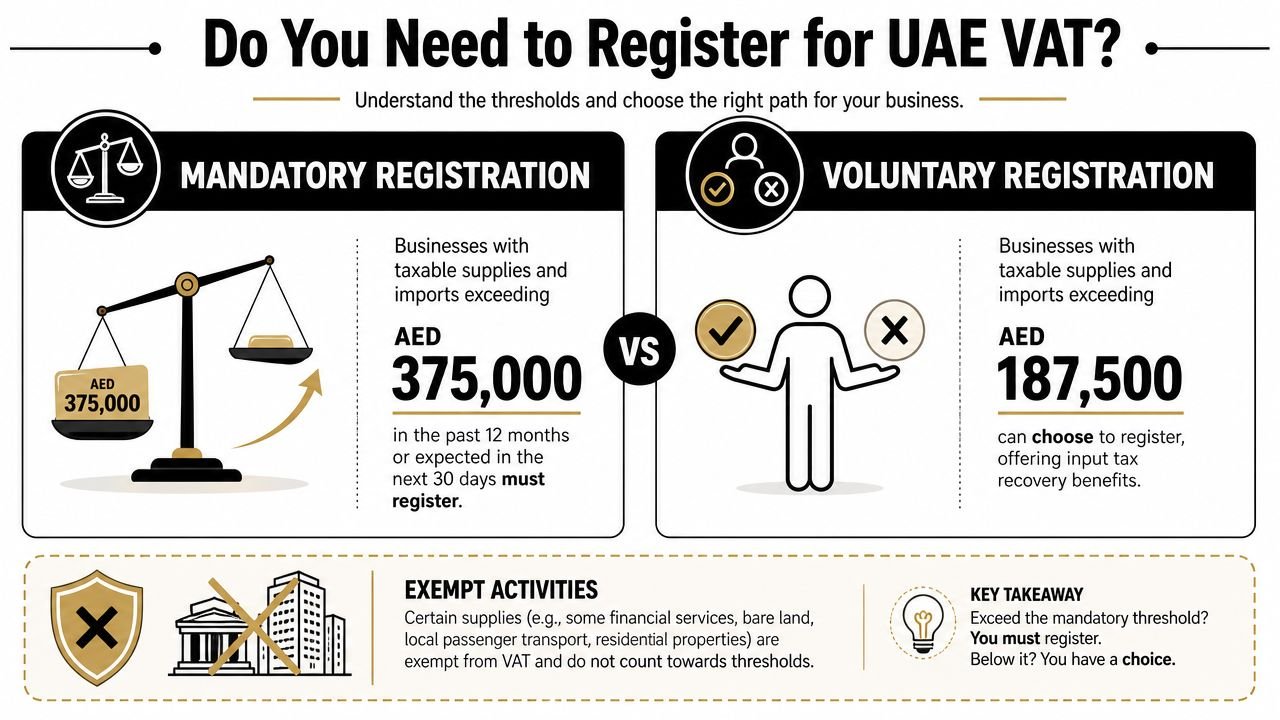

The UAE introduced 5% VAT on 1 January 2018, with mandatory registration at AED 375,000 in annual taxable supplies and imports, and voluntary registration at AED 187,500. Foreign businesses making taxable supplies in the UAE may need to register regardless of value if no other person is liable to account for the tax, according to the UAE government's VAT overview.

Read the thresholds as a business decision

Most founders know the thresholds. Fewer apply them properly.

If your business has crossed the mandatory line, registration is not optional. If you're above the voluntary line but below the mandatory one, you have a choice. That choice should be driven by how your business buys, sells, and contracts.

A simple way to think about it:

| Position | What it means | Strategic effect |

|---|---|---|

| Above mandatory threshold | You must register | Delay creates compliance risk |

| Above voluntary threshold only | You may register | Can support input VAT recovery and B2B credibility |

| Below voluntary threshold | Usually wait | Early registration without a commercial reason often adds admin |

Use a practical look-back and forward view

Founders get stuck because they treat VAT as a historic accounting exercise. It isn't only that. You need both a backward and a forward view.

Use this practical test:

- Look back at actual activity over your recent trading period and total your taxable supplies and imports.

- Look forward at committed business already visible in signed contracts, live retainers, confirmed orders, or launch pipelines.

- Exclude guesswork. Hope is not a forecast. The FTA wants a reasonable basis, not founder optimism.

- Separate taxable from exempt activity before you decide whether a threshold has been met.

For service businesses, this usually means reviewing signed client agreements, monthly recurring invoices, project billing schedules, and imported services. For e-commerce sellers, it usually means looking at actual order flow, marketplace sales, direct website sales, and import activity tied to stock or fulfilment.

Practical rule: If your sales team says revenue is “about to land”, don't use that alone. Use signed paperwork, issued invoices, or defensible commercial evidence.

What founders often misread

The biggest mistake is confusing revenue in the bank with taxable supplies for VAT purposes. Another is counting the wrong activity, especially where a company has mixed income streams.

Watch for these situations:

- B2B service firms: A founder counts only paid invoices and ignores work already invoiced or contractually due.

- E-commerce businesses: The team tracks gross platform settlement but doesn't separate what belongs in the VAT picture.

- Foreign companies: Management assumes low sales volume means no registration issue, even where UAE taxable supplies still trigger an obligation.

- Mixed-activity businesses: Exempt activity gets bundled together with taxable activity, which distorts the threshold analysis.

If you want the cleanest answer to how to register for VAT in UAE, start by deciding whether registration is required, optional, or premature. That single judgement shapes everything that follows.

Assembling Your VAT Registration Document Pack

A weak application usually isn't rejected because the business is ineligible. It stalls because the document pack is inconsistent, outdated, or unclear.

The FTA is trying to verify a few basic things. Does the company legally exist. Who controls it. Who is authorised to act. Is the turnover story credible. Do the contact and banking details line up with the entity being registered.

What to prepare before you log in

This is the document pack most businesses should organise in advance:

- Trade licence copy: This proves the entity is active and licensed to conduct business.

- Company incorporation documents: Formation documents help confirm legal structure, ownership, and authority.

- Identity documents for owners or authorised signatories: Clear passport and Emirates ID copies help the authority match the people behind the application.

- Bank account details: These support basic validation of the operating business.

- Financial records: Management accounts, invoicing records, and turnover support help prove why the company is registering.

- Business contact details: Use an email address and phone number the company monitors.

- Power of attorney, if relevant: If a tax agent or representative submits the application, authority should be documented.

Why these documents matter

The trade licence and incorporation set answer the legal identity question. The identity documents answer the control question. Financial records answer the threshold question.

Bank details and contact data look simple, but avoidable friction often begins with these. If the legal name on one file doesn't match another, or the application uses a founder's casual inbox instead of the company's operating contact, expect follow-up.

Clean scans beat fancy formatting. The portal doesn't care whether your files look polished. It cares whether the information is legible, consistent, and easy to verify.

A few habits make a real difference:

- Name files clearly: Use document names that identify the entity and contents.

- Check expiry dates: An outdated licence or old identity copy can trigger avoidable questions.

- Match spellings exactly: Trade name variations, initials, and shortened names create friction.

- Keep financial support coherent: The numbers in the application should match the underlying records you upload.

Founders often underestimate the strategic value of a well-prepared pack. Good documentation shortens the back-and-forth, reduces the chance of inconsistent declarations, and makes the portal stage much less painful.

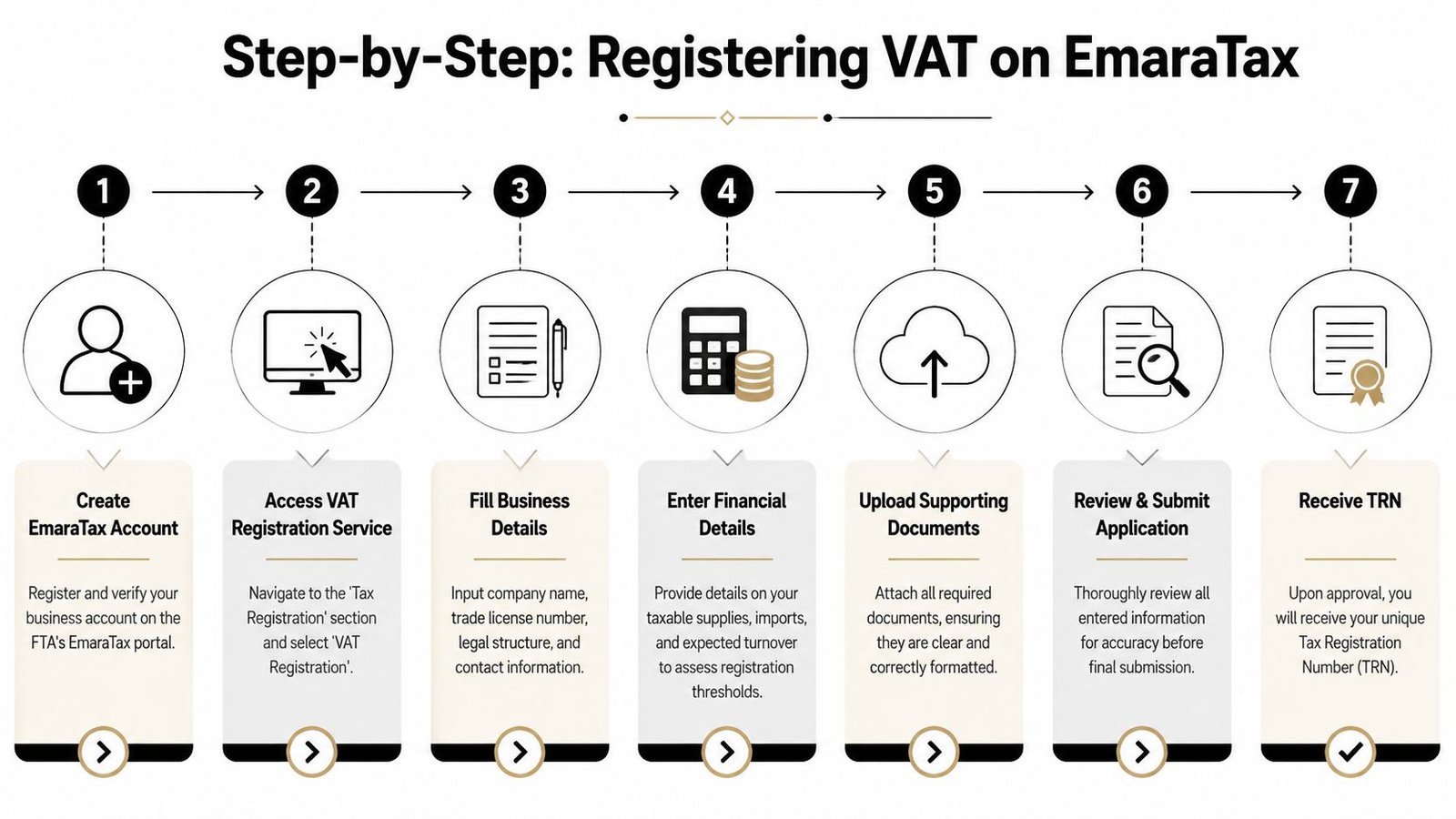

A Walkthrough of the EmaraTax Registration Portal

The registration process runs through the Federal Tax Authority's online environment. In practice, that means your outcome depends less on speed and more on how carefully you enter business facts.

Use the portal only after your threshold analysis and document pack are settled. If you start guessing inside the application, you'll create contradictions that are harder to unwind later.

For a visual overview of the flow, use this reference:

Start with the business profile

Begin by creating or accessing the business account in EmaraTax. The profile stage is where many applicants make the first avoidable error. They rush through legal details because they want to get to the VAT form.

Don't.

Check the legal entity name, licence details, contact information, and authorised person data against your company records before you move ahead. If your profile data and VAT application don't align, the application becomes harder to defend.

A good working sequence looks like this:

- Confirm the entity: Make sure you're registering the correct company, not a related entity with a similar name.

- Validate contact access: The email and phone number should be controlled by the business, not just by a founder who may become unavailable.

- Confirm authority: The person submitting should have internal authority and, where relevant, formal supporting documentation.

Complete the VAT application carefully

The VAT application itself is not difficult. What makes it difficult is that it asks business questions in administrative language.

The fields that deserve extra care are usually these:

- Business activities: Describe what the company does, not what sounds broad or impressive.

- Turnover basis: Use figures you can support with records already in your files.

- Imports and supplies: Make sure the tax logic is internally consistent with your business model.

- Bank details: Enter them exactly as held by the bank and the entity.

If you run a consultancy, say that clearly. If you operate software subscriptions, trading, logistics support, or marketplace sales, describe the commercial activity with enough precision that an external reviewer can understand the VAT position.

A portal field is not the place to “future-proof” your company profile. Register the business you have, not the one you plan to become next year.

The same applies to estimates. If the form requires forward-looking information, base it on contracts, recurring revenue, purchase orders, or other defensible evidence. Aggressive projections may seem harmless, but they can create questions if they don't match the file.

This is also a good point to keep your evidence beside you while entering the form:

| Portal area | Best supporting reference |

|---|---|

| Legal details | Trade licence and incorporation documents |

| Signatory information | Passport, Emirates ID, authority documents |

| Commercial activity | Licence activity, contracts, invoices |

| Financial details | Management accounts, sales records, import records |

| Bank section | Bank confirmation or statement |

Later in the process, video guidance can help users who prefer to see the interface in action:

Review before you submit

The review stage is where disciplined founders save time.

Read the application as if you were the authority seeing the company for the first time. Does the activity description match the licence. Do the financial declarations match the records. Is the signatory the same person shown in the identity and authority documents. Are the uploads legible.

Use this short review filter:

- Consistency: The same company name, same signatory, same contact trail throughout.

- Supportability: Every key declaration should be backed by a file.

- Clarity: No vague activity descriptions or unexplained mismatches.

- Completeness: No missing uploads or half-finished sections.

Submitting quickly feels productive. Submitting accurately is what usually works.

Strategic Choices VAT Grouping and Voluntary Registration

Most registration guides stop once the TRN is issued. That misses the more useful question. What registration model best fits how the business operates?

Two choices deserve more attention than they usually get. The first is whether to register voluntarily when you don't yet have to. The second is whether related companies should stay separate or consider a grouped approach where available and appropriate.

When voluntary registration makes sense

Voluntary registration can make commercial sense for founders selling mainly to VAT-registered businesses, especially where early-stage spend is meaningful and clients expect tax invoices from established suppliers.

That doesn't mean every startup should do it. Sometimes voluntary registration improves procurement discipline and lets the business reclaim input VAT where eligible. Sometimes it only creates filing work before the company has enough process maturity to handle it cleanly.

A useful decision lens:

| Scenario | Voluntary registration may help | Better to wait |

|---|---|---|

| B2B startup with supplier spend | Yes, often commercially useful | Less so if spend is minimal |

| Consumer-facing early venture | Only if the VAT impact is understood | Often yes |

| Business pitching larger corporate clients | Often helpful for onboarding and credibility | Less relevant if clients don't require it |

If your buyers are experienced procurement teams, being VAT-registered can remove friction. If your business is still validating product-market fit and has light overhead, the admin burden may outweigh the benefit.

When a group approach helps

The more complex question arises when a founder controls multiple related entities. One company invoices clients. Another holds staff or intellectual property. A third manages distribution. On paper, each looks separate. Operationally, they move together.

That structure can create duplicated VAT administration and tax treatment questions around intercompany transactions. A grouped approach can simplify the operating model in the right circumstances, but it also centralises responsibility. If one company in the structure is messy, the group filing process won't fix that. It will spread the pain.

A practical comparison:

- Separate registrations: Better when entities operate independently, have distinct risk profiles, or may be sold separately.

- Grouped approach: More useful when related companies are tightly managed, transact regularly with each other, and want a cleaner internal VAT position.

This is the point where founders should stop treating VAT as a filing issue and start treating it as part of company architecture.

Life After Registration Your Ongoing VAT Obligations

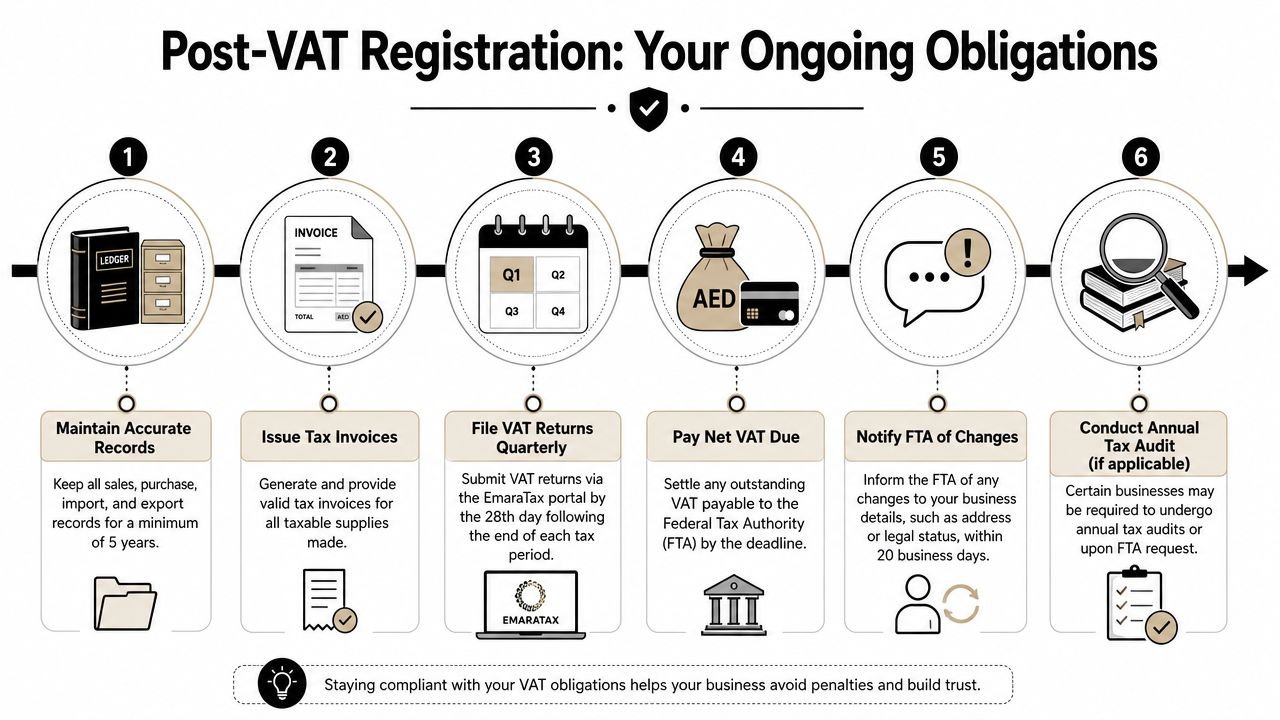

A TRN solves one problem and creates a discipline. From that moment, the business needs repeatable habits around invoices, records, and return preparation.

The distinction between good companies and stressed ones becomes clear. They don't scramble at filing time because the finance trail is already organised.

Build habits around invoices and records

Your first operational job is to issue proper tax invoices and keep support for what you buy and sell. That means sales invoices, supplier invoices, import records, contracts, and internal reconciliations should all be retrievable without drama.

The article is about how to register for VAT in UAE, but the actual test comes after registration. If your team can't explain a transaction from invoice to ledger to bank trail, your VAT process is weak even if the registration was perfect.

Use a simple operating checklist:

- Invoice correctly: Make sure the business issues tax invoices through a controlled process, not ad hoc spreadsheets from different teams.

- Centralise records: Keep sales, purchases, and supporting files in one accessible system.

- Reconcile regularly: Match accounting records to the underlying documents before the return cycle closes.

- Control supplier capture: Missing purchase invoices usually become missed input tax positions or messy follow-up work.

The easiest VAT return is the one prepared from records that were organised at the time of the transaction, not reconstructed months later.

Treat returns as a finance process not a deadline event

VAT returns shouldn't be treated as a calendar surprise. They should be the output of an orderly monthly finance routine.

That routine usually includes reviewing sales coding, checking supplier tax treatment, confirming any cross-border activity, and making sure the input and output positions are supportable. Founders don't need to do every line themselves, but they do need a process owner.

A practical responsibility split often works best:

| Task | Owner inside the business |

|---|---|

| Invoice issuance control | Finance or operations |

| Supplier document collection | Procurement or finance |

| Monthly reconciliations | Bookkeeping or accounting function |

| Return review and sign-off | Finance lead or authorised management |

If you leave VAT to the end of the period, the business starts making rushed judgement calls. That's when invoices are chased late, classifications get guessed, and avoidable errors appear in the filing.

The disciplined approach is boring, which is exactly why it works.

Common Pitfalls and When to Seek Expert Help

A common founder scenario looks like this. Sales grow faster than finance. Someone estimates turnover from bank receipts, the VAT application goes in with mismatched figures, and the business gets its TRN before the invoicing, recordkeeping, and review process are properly set up. The registration itself is not the hard part. The hard part is registering on the right basis, at the right time, with records that will hold up later.

The mistakes that cause trouble are usually ordinary, but the consequences are commercial. A weak application can delay approval. A rushed voluntary registration can create reporting work the business was not ready to absorb. A poor structure choice between related entities can affect input tax recovery, intercompany treatment, and how much admin the finance team carries every quarter.

Where founders usually go wrong

The pattern is usually one of four problems:

- Threshold decisions made on rough numbers: Registration status should be based on records you can defend, not management intuition.

- Portal entries that do not match the file: Trade licence details, revenue figures, authorised signatory data, and supporting documents need to align.

- Registering before the business is operationally ready: Getting a TRN without a functioning invoicing and reconciliation process creates avoidable filing risk.

- Ignoring structure at the point of registration: Related entities, shared operations, and mixed taxable activities often need analysis before the application is submitted.

One point gets missed often. VAT registration is not only a compliance event. It changes pricing, customer perception, procurement recovery, and internal finance workload.

That is why voluntary registration deserves more scrutiny than founders often give it. It can make commercial sense if customers expect a TRN or if the business has input VAT to recover. It can also create a reporting obligation that adds friction before the finance function is mature enough to handle it cleanly.

If the VAT position depends on one person's inbox, memory, or spreadsheet habits, the business is carrying more risk than it realises.

When outside help is the efficient choice

A clean single-entity business with orderly books can often complete registration internally. That works best when one person owns the process, the numbers are reconciled, and management has already decided why it is registering and what changes operationally after approval.

External support starts to make sense when the core issue is judgement, not form filling. That includes uncertain threshold timing, weak historical bookkeeping, multiple related companies, foreign ownership complications, mixed supplies, or questions around whether VAT grouping is commercially sensible. In those cases, the adviser's value is in reducing avoidable errors and helping the business choose the least risky path.

A useful adviser should test more than the application form. They should ask whether registration should happen now or later, whether the entity structure creates unnecessary VAT friction, whether the turnover evidence is strong enough, and whether the finance team can support the first return without improvising. That is the difference between getting registered and getting registered properly.

If you are comparing providers, choose one that can support both the filing and the operating model that follows. Inpro Corporate Services L.L.C. handles UAE company setup, regulatory processes, and VAT registration and filing, which is relevant because these decisions often connect in practice.