You've got the company set up, the licence is issued, and the next bottleneck is obvious. You need a UAE bank account so you can invoice clients, collect revenue, pay suppliers, and show counterparties that your business is operational, not just registered on paper.

Many founders get stuck at this stage, assuming the hard part was incorporation. In practice, the banking phase is when the financial institution decides whether your structure, documents, and commercial story make sense. For a non resident bank account uae application, the question isn't just “Do you have the paperwork?” It's “Would a compliance officer be comfortable defending this approval internally?”

That's the lens that matters. Banks in the UAE do open accounts for non-residents, but they don't approve on goodwill. They approve when the file is coherent, the source of funds is traceable, the account purpose is commercially credible, and the client profile fits the bank's risk appetite.

Table of Contents

- Why You Need a UAE Bank Account for Your Business

- Personal vs Corporate Accounts Choosing Your Path

- The Non-Resident Application Workflow Explained

- Top Banks and Fintechs for Non-Residents in 2026

- Avoiding Common Pitfalls and Application Rejection

- Next Steps From Account Opening to Growth

Why You Need a UAE Bank Account for Your Business

A UAE company without a usable bank account is limited. You can hold a licence, sign contracts, and even issue invoices, but day-to-day operations become awkward fast if clients can't pay locally or if every transaction has to route through another jurisdiction.

That friction shows up in simple places. A local customer may ask for a UAE account name on the invoice. A payment processor may want to see a matching business bank account. A supplier may hesitate if your company is Emirati on paper but your banking sits somewhere unrelated to the transaction.

Banking is part of commercial credibility

Founders often treat banking as an administrative afterthought. Banks don't. Neither do serious counterparties.

A UAE account helps in three practical ways:

- Payment flow: Clients can settle invoices into a local account that matches your UAE entity.

- Operational clarity: Your books are cleaner when business receipts and business expenses run through the correct company account.

- Credibility signal: A banked UAE company looks more established than a company that keeps explaining why payments must go offshore.

The UAE is also a serious banking market, not a fringe option for international founders. According to a World Bank-based UAE banking dataset, total bank deposits reached Dh2,874.6 billion in February 2025, and non-resident deposits grew 5.1% to Dh249.1 billion. That matters because it shows banks in the Emirates already handle substantial capital from both residents and non-residents.

Practical rule: A UAE bank account isn't just for receiving money. It's part of how your company proves it has substance, direction, and a real operating footprint.

The real challenge isn't access

The challenge isn't whether non-residents can bank in the UAE. They can. The actual issue is that banks sort applicants aggressively.

A founder with a clean structure, a sensible business model, and a clear UAE link can move forward. A founder with generic activity descriptions, weak proof of funds, or no obvious reason to bank in the UAE will struggle, even if the incorporation documents are technically complete.

That's why the strongest applications are built backwards from the bank's internal logic. If the account purpose is obvious, if the expected transaction pattern matches the licence, and if the origin of funds is easy to evidence, the file becomes much easier to approve.

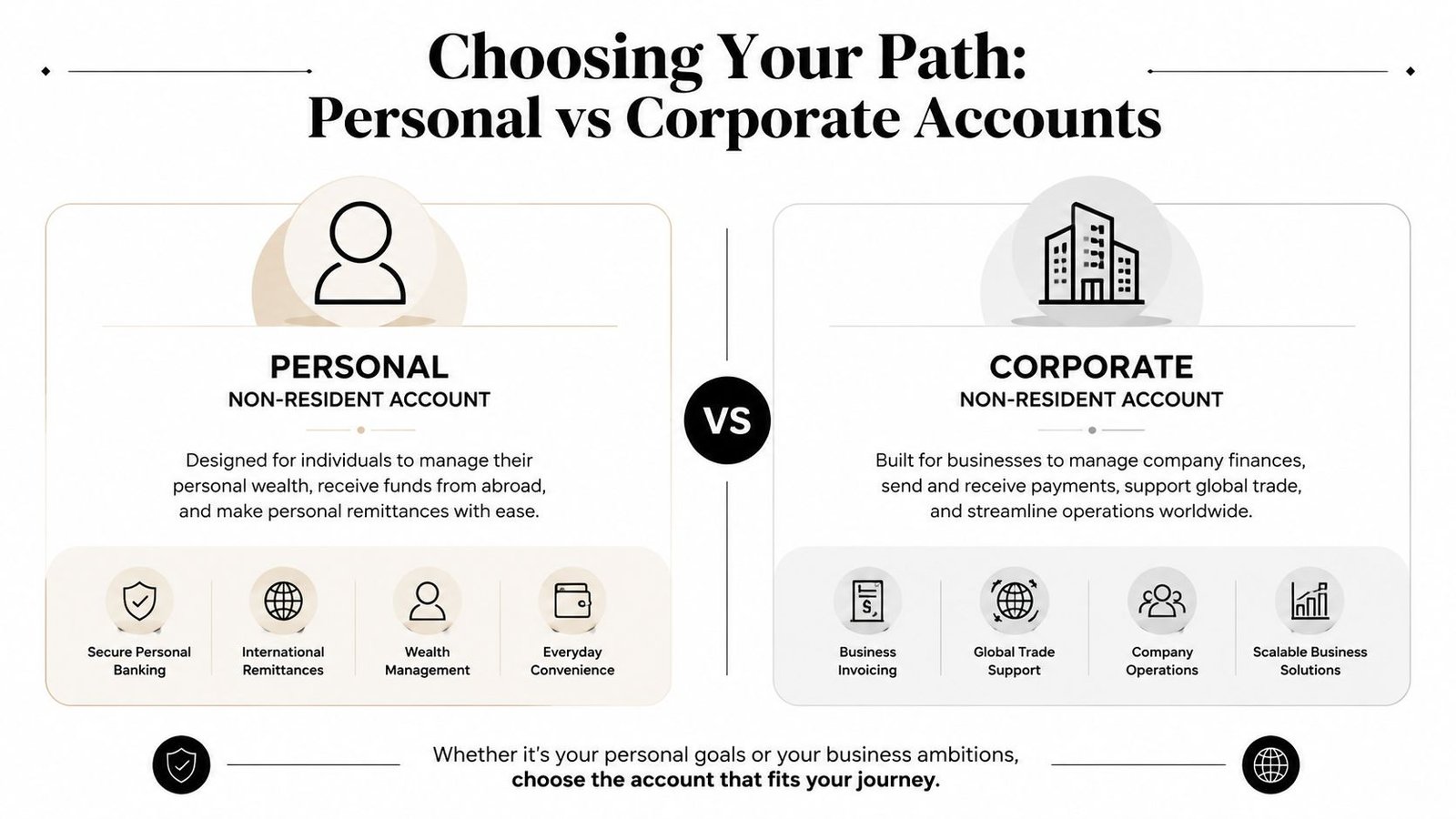

Personal vs Corporate Accounts Choosing Your Path

The first mistake many applicants make is choosing the wrong account type. They ask for a personal non-resident account when what they need is a corporate operating account.

That distinction matters because banks treat personal and business use very differently. If you're trying to run company activity through a personal banking relationship, you're creating a compliance problem from day one.

What personal non-resident accounts are actually for

A personal non-resident account can work if your needs are narrow. Think wealth holding, personal remittance, or receiving income linked to personal investments.

But the product is usually limited. As noted by Nomad Capitalist's overview of UAE banking, a non-resident typically can only open a savings account with a debit card for ATM access, while current accounts, chequebooks, and credit facilities generally require a UAE residence visa.

That tells you almost everything you need to know. If your business needs frequent transfers, vendor payments, collections, payroll, merchant support, or a standard operating setup, a personal account is the wrong tool.

When a corporate account is the correct path

A corporate account is built around company activity. It's the right route if you have any of the following:

- Client invoicing in the company name

- Supplier payments tied to the trade licence

- Cross-border commercial receipts

- A need to separate business and personal funds

- Accounting, VAT, or audit requirements that depend on a proper business trail

A founder sometimes says, “I'll open a personal account first and sort the business account later.” That usually creates delay, not speed. The bank can see the difference between a temporary workaround and an actual operating structure.

If the licence is in the company name, the contracts are in the company name, and the invoices are in the company name, the money should land in the company account.

A simple decision test

Use this test before you apply:

| Situation | Better fit |

|---|---|

| Holding personal funds or investment income | Personal non-resident account |

| Trading, consulting, SaaS, e-commerce, agency, or B2B services | Corporate account |

| Property-related personal receipts | Personal account, depending on the bank |

| Active UAE company with counterparties and recurring payments | Corporate account |

For most founders, startups, and SMEs, the conclusion is straightforward. A personal non-resident account may exist, but it won't replace a proper corporate setup for business operations.

The Non-Resident Application Workflow Explained

Banks want to see an application that is organised before it reaches the branch. If your file only makes sense after a long verbal explanation, it's weak.

For most non-residents, the workflow still starts offline. The process typically involves selecting a bank that accepts non-residents, preparing a full KYC pack, attending in person, and then waiting through compliance review.

What the bank wants to understand

The bank is trying to answer a few core questions.

First, who are the individuals driving the company? That means directors, shareholders, ultimate beneficial owners, and anyone controlling the commercial activity.

Second, what will this account be used for? “General business” is not a credible answer. A bank wants to know what you sell, where your customers are, who pays you, what currencies you expect to receive, and why the UAE is the logical place for the account.

Third, where is the money coming from? This includes startup capital, shareholder funding, retained earnings, consulting income, investment proceeds, or trading receipts. The more direct the paper trail, the stronger the application.

According to SB Advisors' guide to UAE non-resident account opening, the practical workflow requires an in-person branch visit and a complete KYC pack including passport copies, proof of address, bank reference letters, and detailed source-of-funds evidence, and online-only onboarding is generally not permitted because scrutiny is stricter for non-residents.

What to prepare before the branch meeting

Most failed applications are not rejected at the desk. They fail because the file goes into review with gaps.

Build your pack like a compliance file, not a casual application:

- Identity documents: Passport copies for shareholders, directors, and beneficial owners. If the bank asks for entry stamps or visa history, provide them clearly.

- Address evidence: Recent proof of residential address. If the address format is inconsistent across documents, fix that before submission.

- Banking history: Personal or business bank statements that show normal activity and support the source-of-funds story.

- Reference material: Bank reference letters when requested. These help demonstrate existing financial relationships.

- Corporate papers: Licence, incorporation documents, constitutional documents, shareholder register, and any documents showing ownership structure.

- Business explanation: A concise summary of activity, target markets, expected transaction profile, counterparties, and why the UAE entity exists.

- Source-of-funds and source-of-wealth evidence: Contracts, invoices, dividend records, sale agreements, audited accounts, or other supporting records depending on your profile.

The strongest files also include a transaction narrative. Not a spreadsheet full of guesses. A plain-English explanation of what will happen in the account and why it matches the company's activity.

A good KYC pack doesn't just prove identity. It tells a coherent commercial story that survives internal review.

A quick visual summary helps if you're organising multiple stakeholders and documents:

What happens after submission

Once the branch receives the file, the thorough review begins. Relationship managers may appear positive at meeting stage, but that isn't approval. Compliance teams will test whether the declared activity, expected turnover, ownership structure, and funding evidence line up.

Weak applications fail under scrutiny. Common examples include a software consultancy with no client contracts, a holding company with no explanation for incoming transfers, or a trading business that can't explain counterparties and goods flow.

Expect follow-up questions. Banks often ask for clarification rather than rejecting immediately, but the tone of those questions tells you a lot. Narrow, technical questions usually mean the file is alive. Broad questions about basic purpose often mean the bank still doesn't understand why it should open the account.

Top Banks and Fintechs for Non-Residents in 2026

A founder flies into Dubai for two days, meets a relationship manager, hears encouraging language, and assumes the bank is a fit. Two weeks later, compliance declines the file. The problem usually is not the bank's website, the meeting, or even the document list. The problem is that the institution was wrong for the profile from the start.

That is how this section should be read. The right question is not which bank is “best.” The right question is which institution is likely to accept your ownership structure, business activity, expected flows, and non-resident status without forcing the file into a risk category it does not want.

Banks and fintechs do not assess non-resident applicants the same way. Some are more comfortable with conventional operating companies that can show contracts, invoices, and a clear UAE business reason. Others work better for digitally organised businesses with simpler payment needs and cleaner onboarding profiles. A compliance officer is looking for alignment. If your file fits the institution's preferred client type, approval gets easier. If it does not, a strong set of documents may still go nowhere.

How to choose the right institution

Start with risk appetite. This is the filter that matters most. A bank may say it opens non-resident accounts, but still avoid certain nationalities, complex shareholding chains, holding companies without active trade, early-stage ventures with thin turnover, or businesses tied to higher-review sectors.

Then look at the relationship model. Some banks still expect a classic banker-client relationship, regular branch interaction, and a profile that justifies internal attention. Others are more process-driven and work better when the company is digitally organised, the activity is easy to verify, and the expected usage is straightforward.

Product fit comes next. This point gets missed often. A company that needs payroll, supplier payments, user permissions, and predictable international transfers should not apply for a product that is better suited to passive balances or basic personal banking.

Preparation also affects bank choice. Some applicants file directly. Others use a corporate services firm to package the case, identify banks that are realistic for the profile, and correct issues before submission. Inpro Corporate Services L.L.C. is one example of a provider founders use for company setup, account opening support, and compliance coordination.

Good applications get rejected every week because they were sent to the wrong institution for the underlying risk profile.

UAE Banks for Non-Resident Accounts Corporate

| Bank/Platform | Typical Minimum Balance | Account Features | Best For |

|---|---|---|---|

| Emirates NBD | Varies by profile and product | Traditional corporate banking, broad recognition, strong local presence | Established SMEs and companies with clear UAE business activity |

| Mashreq | Varies by product and review outcome | Conventional banking services, international accessibility, known non-resident product visibility on the personal side | Founders who want a recognisable bank and can present a clean, well-documented file |

| ADCB | Varies by relationship and account type | Full-service banking for suitable corporate clients | Businesses with straightforward ownership and conventional transaction patterns |

| Wio | Depends on eligibility and onboarding fit | Digital-first business banking experience for eligible companies | Digitally organised businesses that fit the platform's onboarding criteria |

The table helps, but the key distinction is how each option tends to read a file.

Emirates NBD suits companies that can present substance clearly. It helps to show active UAE operations, credible counterparties, and transaction behaviour that looks ordinary for the stated business. Strong name recognition is useful in practice, especially if clients or suppliers prefer dealing with a major local bank. The trade-off is that recognisable banks also tend to have little patience for unclear structures or vague commercial purpose.

Mashreq often appeals to founders who want a familiar bank with decent international usability. Approval depends heavily on how well the business case is framed. I have seen solid files work here when the activity, turnover expectations, and ownership story were easy to verify. I have also seen weaker files fail because the applicant relied on brand preference instead of institutional fit.

ADCB is usually easier to position for conventional businesses than for unusual ones. If the shareholding is simple, the source of funds is easy to evidence, and the company's activity does not require long explanations, it can be a sensible option. If the file involves nominee layers, cross-border holding logic, or projected activity without operating proof, expect heavier scrutiny.

Wio has attracted attention because the onboarding experience is more digital and the operating model suits modern SMEs. That does not mean approvals are loose. Digital-first banks still screen for clarity, expected account behaviour, and eligibility. Wio tends to make more sense for companies that keep organised records, use clean documentation, and do not need complex bespoke banking arrangements from day one.

One practical point matters across all four. Do not apply based on the broadest possible shortlist. Apply based on the shortlist that makes sense to a UAE compliance team reviewing your file in ten minutes. That usually means choosing the bank or fintech that needs the fewest assumptions to understand why your company exists, why it needs a UAE account, and how the money will move through it.

Avoiding Common Pitfalls and Application Rejection

Founders often think rejection means they missed a document. Sometimes that's true. More often, the bank saw a file that raised more questions than it answered.

Thinking like a compliance officer changes the outcome. The officer is not asking, “Can I find a reason to say yes?” The officer is asking, “If this account behaves exactly as described, will it make sense six months from now when transactions start moving?”

Why complete documents still get rejected

The market is selective. As noted by Takween Advisory's non-resident banking guide, non-resident accounts often have high minimum balance requirements, from AED 100,000 to over USD 100,000, and banks can reject applications even when the documents are complete if the purpose is vague, the expected transaction profile is too low, or the UAE connection is weak.

That last point matters more than most applicants realise. A bank doesn't just want documents. It wants a reason.

Here are the patterns that most often weaken a file:

- Vague account purpose: “International business” says nothing. Banks want specifics.

- Weak UAE nexus: If you have no clients, suppliers, property, team, or operational reason tied to the UAE, the bank may question why the account belongs here.

- Thin funding story: Source of funds must be provable, not described.

- Mismatch between licence and activity: If the licence says consultancy but the transactions look like product trading, review gets harder.

- Low expected activity: Some banks won't allocate compliance capacity to an account that looks dormant from the start.

- Overcomplicated ownership: Layers of holding entities are possible, but every extra layer must be documented and justified.

What a strong file looks like

A strong application feels unsurprising. Every document supports the same conclusion.

For example, if the company provides software development services, the file should show a software-related licence, founder background in that field, client contracts or proposals, invoices or pipeline evidence, and a source-of-funds trail that matches the founder's financial history.

That doesn't mean every company needs years of operating history. It means the business has to look real, understandable, and properly financed.

A practical approval mindset looks like this:

- Show the commercial logic clearly. Explain why this company exists in the UAE, who it serves, and how money will move.

- Match the documents to the story. If the narrative says consultancy retainers, bank statements and contracts should support that.

- Respect the bank's balance expectations. If the bank expects a meaningful relationship, come prepared for that reality.

- Reduce ambiguity. Simplify ownership charts, transaction descriptions, and supporting materials wherever possible.

The fastest way to lose a bank's confidence is to make them guess. If they have to infer your business model from scattered documents, the file is weak.

One more issue deserves attention. Some founders try to minimise detail because they think less disclosure creates less risk. In UAE banking, the opposite is usually true. Selective disclosure reads like evasion. Structured transparency reads like control.

Next Steps From Account Opening to Growth

Approval isn't the finish line. It's the start of a monitored banking relationship.

Once the account is live, your job is to keep the behaviour of the account consistent with what was presented during onboarding. If you told the bank to expect consulting receipts from specific markets, then a sudden stream of unrelated third-party transfers will create avoidable friction.

How to keep the account healthy

Treat post-opening compliance seriously from day one.

- Maintain the expected balance: If your account carries a minimum balance condition, monitor it carefully.

- Use the account for the declared purpose: Don't mix unrelated personal and business transactions.

- Reply quickly to reviews: Periodic KYC refresh requests are normal. Slow responses can freeze momentum.

- Keep records organised: Contracts, invoices, and supporting proofs should be easy to retrieve if the bank asks questions.

- Update the bank on material changes: Ownership changes, new activities, or major shifts in transaction geography shouldn't surprise the bank.

How banking connects to wider UAE compliance

A working bank account supports much more than payments. It sits at the centre of your operating stack.

Your accounting becomes cleaner when the company has a proper banking trail. VAT registration and filing become more straightforward when invoices, receipts, and expenses are recorded consistently. Internal controls improve when founders stop using personal channels for company transactions.

This is also where many international businesses mature. They start with bank opening as an urgent setup task. Then they realise the account needs to fit a larger system that includes bookkeeping, tax handling, payroll where relevant, and ongoing document discipline.

If you approach the process properly, the bank account becomes more than a utility. It becomes the financial backbone of your UAE operation.

If you need support with a non resident bank account uae application, Inpro Corporate Services L.L.C. can assist with company setup, banking documentation, and the related compliance steps that usually determine whether a file is workable before it reaches the bank.