Most advice on how to open an offshore account is outdated the moment it tells you to start with a jurisdiction list.

That approach belonged to an earlier era, when founders treated offshore banking as a shortcut. In the UAE context in 2026, it works the other way around. The bank first wants to understand your business, your cross-border flows, your ownership chain, and why an offshore account is commercially necessary. The jurisdiction comes after that, not before it.

The serious reason founders pursue an offshore structure today is practical. They need cross-border treasury, multi-currency transactions, and asset segregation through an account outside their home jurisdiction, and banks will only consider that request after detailed KYC, AML, business-document, and proof-of-funds review, as outlined by Airwallex's overview of offshore bank accounts. In the UAE, that scrutiny is even more visible because offshore banking is usually tied to company formation, holding structures, or international trade activity, not everyday retail banking.

Table of Contents

- Why Open an Offshore Account Means Something Different in 2026

- Choosing Your Offshore Jurisdiction Strategically

- Assembling Your Compliance-Ready Documentation Pack

- Corporate vs Personal Offshore Account Differences

- Navigating the Account Opening Process with a Partner

- Red Flags, Reporting Rules, and Final FAQs

Why Open an Offshore Account Means Something Different in 2026

The phrase open account offshore still attracts the wrong expectations. Many founders hear it and think secrecy, speed, and minimal questions. Banks hear something else entirely. They hear cross-border risk, beneficial ownership review, sanctions screening, tax-residency checks, and transaction-pattern analysis.

That shift matters most in the UAE because the banking system is strong, internationally connected, and selective. An offshore account is no longer a decorative add-on to a company structure. It's a regulated financial tool for legitimate international business, especially when a founder needs foreign-currency capability, payment rails across multiple markets, or separation between operating cash and long-term assets.

The compliance bar is high for a reason. Banks in and around the UAE are under pressure to reduce fraud exposure and avoid shell-entity relationships that don't show real economic logic. That is why generic promises of a quick approval window should be treated with caution. As NerdWallet's offshore banking guidance notes, de-risking has tightened onboarding, and account approval increasingly depends on detailed KYC and UBO files, a credible business rationale, and transaction history rather than the jurisdiction label itself.

Practical rule: If your plan can be summarised as “I want offshore banking because it sounds flexible”, you are not ready to apply.

Founders who succeed usually present a straightforward commercial story. A UAE holding company needs a separate account to receive overseas dividends. A trading business needs multi-currency collections outside its home market. A group structure wants asset segregation between intellectual property, reserves, and day-to-day operations. Those are legible use cases. Banks can assess them.

What doesn't work is trying to package an offshore account as a status symbol or a vague “global expansion” idea with no underlying operating footprint. In 2026, offshore banking is less about location shopping and more about proving legitimacy. The standards feel demanding because the system is trying to filter for businesses that can stand up to scrutiny after the account is opened, not just on the day the application is submitted.

Choosing Your Offshore Jurisdiction Strategically

A founder shouldn't ask, “What is the best offshore jurisdiction?” The useful question is, “Which jurisdiction gives my business the best chance of securing workable banking for its actual use case?”

That distinction saves time. For UAE-based founders, an offshore company or offshore account isn't automatically the right tool. The result depends on residency, business substance, source of funds, and the bank's AML screening. The UAE also has a highly advanced banking environment, with 7 banks on Forbes' best-banks list and 4 UAE banks ranked among the top 10 safest in the Middle East, as noted in Wise's review of countries for offshore banking. That means founders shouldn't assume “offshore” is better by default. It may be better for a specific treasury or holding need. It may also be the wrong fit.

Start with the banking outcome, not the brochure

Jurisdiction selection should be driven by bankability, not marketing language. In practice, I'd assess four filters first:

- Business purpose: Are you building a holding structure, trade vehicle, SPV, treasury hub, or asset-owning entity?

- Counterparty perception: Will investors, suppliers, and payment partners accept the structure comfortably?

- Compliance readability: Can you explain ownership, activity, and source of funds without forcing a bank officer to decode the file?

- Operational fit: Does the jurisdiction work smoothly with your UAE residency position, licences, contracts, and reporting obligations?

A founder often loses weeks choosing a jurisdiction that looks elegant on paper but creates awkward questions in banking review. A simpler structure with better documentary coherence usually performs better than a more exotic structure with weak substance.

The best jurisdiction is usually the one a banker can understand in five minutes and approve with confidence after full review.

Offshore Jurisdiction Comparison for UAE Businesses

| Jurisdiction | Primary Use Case | Reputation & Compliance | Typical Banking Fit |

|---|---|---|---|

| RAK ICC | Holding structures linked to UAE planning, asset ownership, cross-border group structuring | Familiar in the UAE context when properly documented and paired with a clear commercial rationale | Often suited to founders who need alignment with UAE corporate planning and can show beneficial ownership and business nexus clearly |

| Mauritius | Investment holding, regional structuring, certain Africa-facing activities | Often considered when treaty access or regional investment logic is part of the structure | Better fit when the founder can show a genuine investment rationale and supporting documentation |

| Cayman Islands | Funds, sophisticated holding structures, investment vehicles | Well known globally, but banks will still focus on substance and legitimacy rather than name recognition | Typically stronger for institutional or investment-oriented use cases than for ordinary SME operating accounts |

A few decision points matter more than founders expect.

Look for credibility, not novelty

Political and economic stability matter because they affect how counterparties and banks perceive long-term risk. Regulatory clarity matters because unclear structures trigger more questions. Data protection and confidentiality matter too, but they should never be the main selling point in a modern offshore strategy.

The founders who get this right usually choose a jurisdiction that fits their actual business model. The ones who get it wrong usually choose based on internet rankings, low-fee marketing, or old assumptions about secrecy. In the UAE market, credibility travels further than novelty.

Assembling Your Compliance-Ready Documentation Pack

The most common mistake in offshore banking is treating documents as a checklist exercise. Banks don't see them that way. They use them to decide whether your profile is internally coherent.

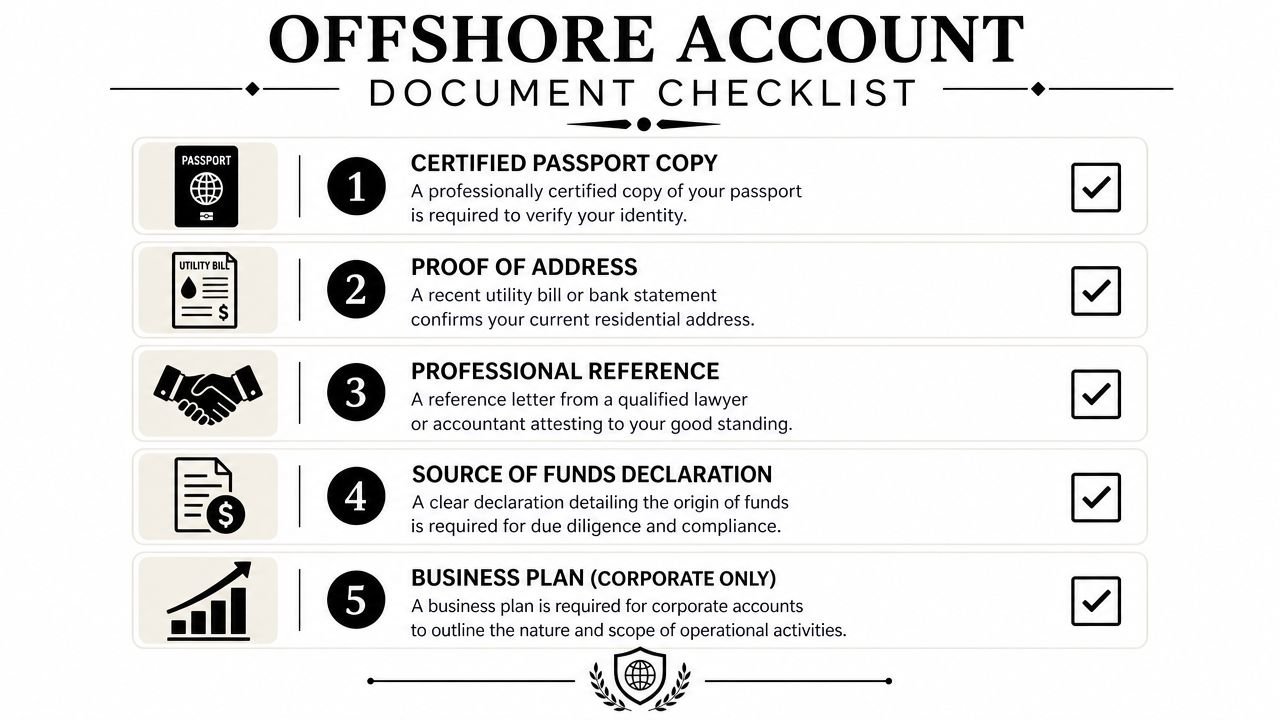

The hardest stage is usually pre-qualification, not form submission. Offshore banking guidance consistently points to the same friction point: banks want a complete file before they seriously review the application, including a passport copy, proof of address, source-of-funds evidence, bank or professional references, and often a business plan. Mainstream offshore banks commonly expect opening deposits around US$5,000 to US$10,000, while premium private banks may require US$250,000+, according to BBCIncorp's guide to setting up an offshore bank account.

What the bank is really testing

A compliance officer is trying to answer a small set of questions.

- Identity: Are you clearly identifiable, and do your personal details match across all records?

- Residency: Can the bank place you in a real tax and address context?

- Wealth origin: Can you explain how you earned the money that will enter the account?

- Business logic: Does the account serve a genuine commercial purpose?

- Expected activity: Will the likely transactions match the profile described in the application?

If one of those answers is vague, the file weakens quickly. A perfect passport copy doesn't rescue an unclear source-of-funds narrative. A polished business plan doesn't rescue an ownership structure that has no obvious operational logic.

How to make the file coherent

The strongest applications read like one story told through several documents.

Start with identity and address records that are current, legible, and consistent. Small mismatches create unnecessary friction. A shortened personal name on one document and a full legal name on another may be explainable, but every explainable issue still consumes review time.

Then focus on your source of funds, an area where founders often underperform. “Business income”, “consulting revenue”, or “investments” is too broad on its own. The bank wants a narrative backed by evidence. If funds came from salary, dividends, retained profits, an asset sale, founder distributions, or investment proceeds, say so clearly and support the statement with matching documents.

For a corporate application, the business plan matters because it tells the bank what transactions should appear after approval. It doesn't need startup theatre. It needs clarity.

- Business model: State what the company does in plain English.

- Counterparties: Identify where clients, suppliers, or portfolio assets are located.

- Account purpose: Explain why this offshore account is needed instead of, or alongside, existing UAE banking arrangements.

- Transaction profile: Describe the kinds of incoming and outgoing payments the bank should expect.

A compliance-ready file doesn't try to impress. It tries to remove doubt.

Reference letters still matter in many cases because they give the bank an external comfort signal. If the bank verifies them, they need to hold up. That is why rushed applications fail so often. The issue isn't just missing paperwork. It's missing narrative discipline.

Corporate vs Personal Offshore Account Differences

Founders often treat this as a form choice. In practice, it is a compliance decision that shapes whether the bank accepts your application at all.

A personal offshore account is built around an individual's own wealth, investments, salary receipts, and private cross-border banking needs. A corporate offshore account is built around identifiable business activity through a legal entity. In the UAE context, that distinction matters because banks are expected to understand the commercial logic behind cross-border flows, not just verify identity documents.

When a personal structure fits

A personal account can work for an internationally mobile consultant, investor, or executive who is managing personal funds and has no reason to book revenue through a company.

The review is still serious. The bank will examine residency, tax exposure, source of wealth, source of funds, and expected transaction patterns. What changes is the scope. The file is centred on the individual rather than on an operating business, shareholder chain, commercial contracts, and underlying counterparties.

The mistake I see regularly is a founder using a personal account for activity that is clearly corporate. Client payments, supplier settlements, platform revenues, or licensing income usually belong in an entity account. Once the bank sees a mismatch between account type and transaction reality, the issue is not paperwork. It is credibility.

When a corporate structure is the right answer

A corporate account is usually the correct route where the business needs legal separation between shareholder funds and company funds, where contracts sit with an entity, or where the account will support genuine international operations.

Common cases include:

- Holding companies: receiving dividends, holding shares, or owning intellectual property

- Trading businesses: collecting revenue and paying suppliers across multiple jurisdictions

- Investment vehicles: deploying and receiving capital through a defined ownership structure

- Group treasury functions: separating reserves, distributions, and operating cash

Corporate accounts face a higher review threshold for a simple reason. The bank is not only assessing one applicant. It is assessing the company, its owners, its controllers, its transaction logic, and the reason the structure exists in the first place. That higher bar is especially visible for UAE-linked founders, because offshore banking is no longer viewed as a privacy product. It is judged as part of a regulated international business setup that must make commercial sense.

Bank type matters as much as account type. As described in Nestmann's offshore banking overview, some offshore banks ask for very high minimum deposits, particularly in private banking and investment-focused segments. Those institutions are built for wealthy private clients and large balances, not for every founder with a new free zone company.

That is why account strategy has to match reality. An early-stage operator with moderate volumes needs a bank that understands trading flows, services income, or group expansion from the UAE. A founder building a holding structure or treasury platform needs a bank that can assess ownership chains, board control, and cross-border fund movements without treating normal commercial activity as suspicious.

The account itself is only part of the decision. The larger question is whether your structure, transaction profile, and jurisdiction story are coherent enough for the bank to defend internally. That is where good advisers earn their fees. They do not sell secrecy. They help position a legitimate international business in a way a compliance team can approve.

Navigating the Account Opening Process with a Partner

Founders usually lose time before they lose the application.

The problem is rarely simple ineligibility. It is poor sequencing, a weak bank match, or a file that does not explain the commercial logic clearly enough for a compliance team to defend internally. In the UAE context, that standard is high for good reason. Banks are expected to understand who is behind the structure, why the account sits offshore, what funds will move through it, and whether the activity fits the stated business model. Offshore banking now functions as infrastructure for legitimate international trade, holding, and treasury activity. It is not treated as a privacy product.

A capable adviser changes the process from trial and error to case preparation. The work starts with whether the structure is bankable, not with a list of banks to try. That sounds obvious, but many founders still approach offshore banking as a shopping exercise. In practice, banks in 2026 want a defensible rationale tied to real operations, especially where a UAE company, UAE resident founder, or UAE group structure is involved.

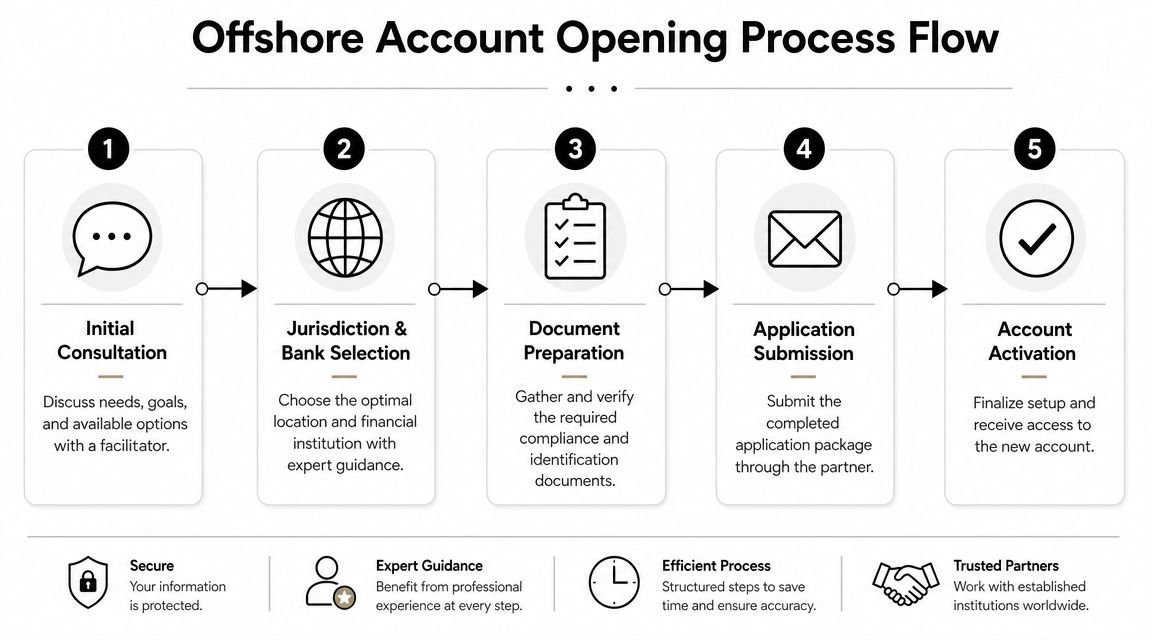

A useful visual summary of the workflow looks like this:

What the journey looks like

The process is rarely linear. Strong applications still tend to move through five predictable stages.

Profile review

The adviser reviews residency, nationality, business model, ownership chain, expected counterparties, payment corridors, and source of funds. They should also challenge whether an offshore account is the right answer at all. Sometimes the better outcome is a mainland UAE banking relationship, an EMI for operating flows, or a different holding setup.Jurisdiction and bank selection

The objective is fit. A founder running a UAE-based consulting group billing clients in three currencies needs a different banking partner from a family office building a holding structure or an e-commerce operator with high chargeback exposure. The bank must be comfortable with the client segment, the jurisdictions involved, and the expected transaction pattern.Pre-vetting the file

Weak cases are exposed early in this stage. Names, addresses, ownership percentages, supporting contracts, invoices, website disclosures, and business descriptions need to line up across every document. Many delays start here, when the founder realizes the structure may be legitimate but the paper trail does not show it well.Formal introduction and submission

Once the file is coherent, the application goes in with a clear account purpose, realistic activity estimates, and supporting evidence that matches the stated use case. A good submission helps the relationship manager carry the file through compliance review without rewriting the client story from scratch.Compliance follow-up and activation

Follow-up questions are normal. Banks ask for clarification because they are accountable for the relationship after approval, not just at onboarding. The difference between a good file and a bad one is not whether questions arrive. It is whether they can be answered quickly with documents that already exist.

This short video gives a simple overview of how account-opening workflows are typically structured:

Where founders usually lose momentum

The predictable mistakes are less about paperwork and more about judgment.

- Applying too widely, too early: Rejections leave a record. A weak file sent to several institutions can narrow options later.

- Choosing the bank by reputation alone: A well-known private bank may be the wrong fit for an operating company with moderate balances and frequent commercial payments.

- Presenting an offshore structure without a business case: “International expansion” is too vague. Banks want to see why the account is needed, how it will be used, and why the structure makes sense from the UAE.

- Treating compliance questions as an obstacle instead of part of underwriting: If a founder becomes defensive when asked about source of wealth, connected entities, or expected counterparties, the file becomes harder to support.

- Using an adviser who only forwards documents: Real value comes from pressure-testing the case before submission, not from acting as a courier.

Banks approve files that a compliance officer can explain in one clear internal memo.

That is the practical role of a partner. They do not give anyone special access, and they cannot promise approval. They improve the odds by matching the case to the right institution, tightening the narrative, and preventing avoidable errors that trigger concern in a UAE-linked file. The benefit is disciplined case construction, realistic bank selection, and fewer surprises after submission.

Red Flags, Reporting Rules, and Final FAQs

Once an offshore account is opened, the compliance work doesn't stop. Banks keep monitoring account behaviour, and founders still have tax and reporting obligations in the places that matter to them personally and corporately.

The most dangerous misunderstanding is believing that offshore means invisible. It doesn't. A well-run offshore structure is transparent to the parties that are entitled to see it, properly documented, and used for lawful commercial reasons.

What gets applications rejected or delayed

A few patterns repeatedly create trouble:

- Vague business purpose: “International business” is not a reason. Banks want an actual commercial use case.

- Inconsistent information: Differences across passports, proof of address, company records, and bank forms create suspicion quickly.

- Weak source-of-funds support: Broad claims with no documentary backing rarely survive review.

- No economic substance: Pure holding structures with no clear rationale, activity, or ownership logic attract deeper scrutiny.

- Transaction expectations that don't match the account story: If the business plan says one thing and the likely payment pattern suggests another, the file becomes harder to defend.

A second risk sits outside the application itself. Reporting obligations can be severe if ignored. For U.S. persons, missing FBAR filings can trigger penalties of up to US$15,611 per non-willful violation as of 2024, while willful violations can reach 50% of the account balance or US$156,107, whichever is greater, according to Piwik PRO's summary of digital account-opening and offshore compliance pitfalls.

Offshore banking is not a substitute for tax compliance. It increases the importance of getting reporting right.

Final FAQs

Is an offshore account the same as a non-resident account?

No. They can overlap, but they are not the same concept. A non-resident account refers to your banking status relative to a country. An offshore account usually refers to an account held outside your home jurisdiction, often for international structuring, treasury, or asset segregation purposes.

Does an offshore account remove tax obligations in my home country?

No. Tax treatment depends on your residency, citizenship where relevant, the entity structure, and applicable reporting rules. The account location alone doesn't eliminate obligations.

Is a UAE founder always better off with an offshore structure?

No. Sometimes a mainland or free-zone operating setup with suitable banking is the cleaner answer. Offshore should be used when it solves a real cross-border or holding problem, not because it sounds impressive.

Can I open an offshore account without strong documentation?

In practice, weak documentation is one of the fastest ways to lose bank interest. Serious banks want a complete and credible file.

What is the right mindset going in?

Treat the process like institutional underwriting. Because that is what it is.

If you're weighing whether an offshore account, a UAE operating account, or a full company structure is the right move, Inpro Corporate Services L.L.C. helps founders assess the practical path, prepare the required compliance pack, and align company formation, banking, visas, and ongoing regulatory support under one UAE-focused workflow.