You usually reach this stage at the same point. The trade licence has been issued, the visa process is underway, and the company exists on paper, but money still has nowhere proper to land or leave. A client asks for your invoice, a supplier asks for payment, and the account you planned to use temporarily is no longer a workable option.

Opening a RAK business account starts with the basics banks expect to see. A valid UAE trade licence, clear shareholder and signatory documents, and a business activity the compliance team can understand from real supporting evidence such as contracts, supplier quotations, invoices, or a short business plan. The paperwork matters, but so does the commercial story behind it. If the bank cannot see how the company will earn, receive, and spend funds, delays are common even for licensed businesses.

Founders often assume the main decision is where to submit the application. In practice, the bigger issue is what happens after the account is opened. Monthly minimum balance rules, transfer charges, international payment scrutiny, and transaction limits can affect a small company more than the initial setup fee. I regularly see free zone companies choose an account that looked inexpensive at the start, then run into avoidable operating costs or compliance friction once client payments begin.

Ras Al Khaimah remains a practical base for startups and small businesses because company formation is relatively straightforward and banks are used to seeing both mainland and free zone structures. Approval is still case by case. The strongest files are not always the fastest to prepare, but they usually have a better chance of clearing review without repeated document requests.

That is the part many generic guides miss. Bank account opening in the UAE is not only an application task. It is an approval exercise, and the quality of your file affects both your chances of opening the account and the cost of running it properly afterward.

Table of Contents

- Your Guide to UAE Corporate Banking in Ras Al Khaimah

- Confirming Your Eligibility for a RAK Business Account

- Gathering Your Essential Application Documents

- The Bank Account Application Process Deconstructed

- Choosing the Right Account Not Just the Cheapest One

- Why Applications Fail and How to Ensure Success

Your Guide to UAE Corporate Banking in Ras Al Khaimah

What is a RAK business account

A founder sets up a Ras Al Khaimah company, gets the licence issued, starts speaking to clients, and then discovers the bottleneck is banking. Until the company has a working corporate account, invoicing, supplier payments, payroll, and routine compliance all stay harder than they should be.

A RAK business account is a corporate bank account opened in the name of a UAE-registered company for day-to-day business use. It is used to receive customer payments, pay suppliers, run payroll, and keep company funds separate from personal funds.

For many SMEs, RAKBANK is one of the first banks considered. That is partly because of its long presence in the UAE market and its clear focus on business banking. The bank traces its history to 1976, as outlined on the RAKBANK corporate profile.

Why does your company need one

A business account is not just an admin item. It affects how credible your company looks to banks, payment providers, auditors, tax advisers, and commercial counterparties.

In practice, the account becomes part of your compliance file. The licence, invoices, contracts, and transaction trail should all point to the same business activity and the same legal entity. If they do not, questions come quickly and account review gets slower.

Practical rule: If your trade licence says consultancy, but your first incoming payment reference looks like commodity trading, expect the bank to ask for clarification.

This is also where founders often underestimate cost. The company can be incorporated at a relatively low setup price, but banking brings its own ongoing requirements. Minimum balance rules, transfer charges, international payment fees, card costs, cheque book charges, and the internal cost of answering compliance queries all affect the operating budget. For startups and free zone companies, those costs matter as much as the account opening form.

Why do founders look at Ras Al Khaimah

Ras Al Khaimah appeals to founders who want a UAE company without starting with the highest overheads. That usually includes service businesses, small trading firms, holding structures, and owner-managed companies that need a practical base first and a more complex setup later if the business grows.

There is also a banking reality behind that choice. A RAK company can be perfectly bankable, but approval is never automatic just because the entity is in RAKEZ or another RAK jurisdiction. Banks still assess ownership clarity, business activity, expected transaction profile, client geography, and whether the company looks operational from day one. Founders who treat banking as a paperwork exercise are often surprised. Founders who prepare for the bank's risk review usually move faster.

| Point founders care about | What it means in practice |

|---|---|

| Cost control at setup stage | You can start with a leaner company structure, but banking costs still need to be budgeted separately |

| Access to UAE banking | A Ras Al Khaimah entity can still hold a UAE corporate account if the business profile is clear and acceptable to the bank |

| SME familiarity | RAKBANK has long been associated with smaller businesses as well as larger corporate clients |

| Approval probability | A clear business model, sensible projected volumes, and consistent documents usually matter more than choosing the cheapest licence package |

Confirming Your Eligibility for a RAK Business Account

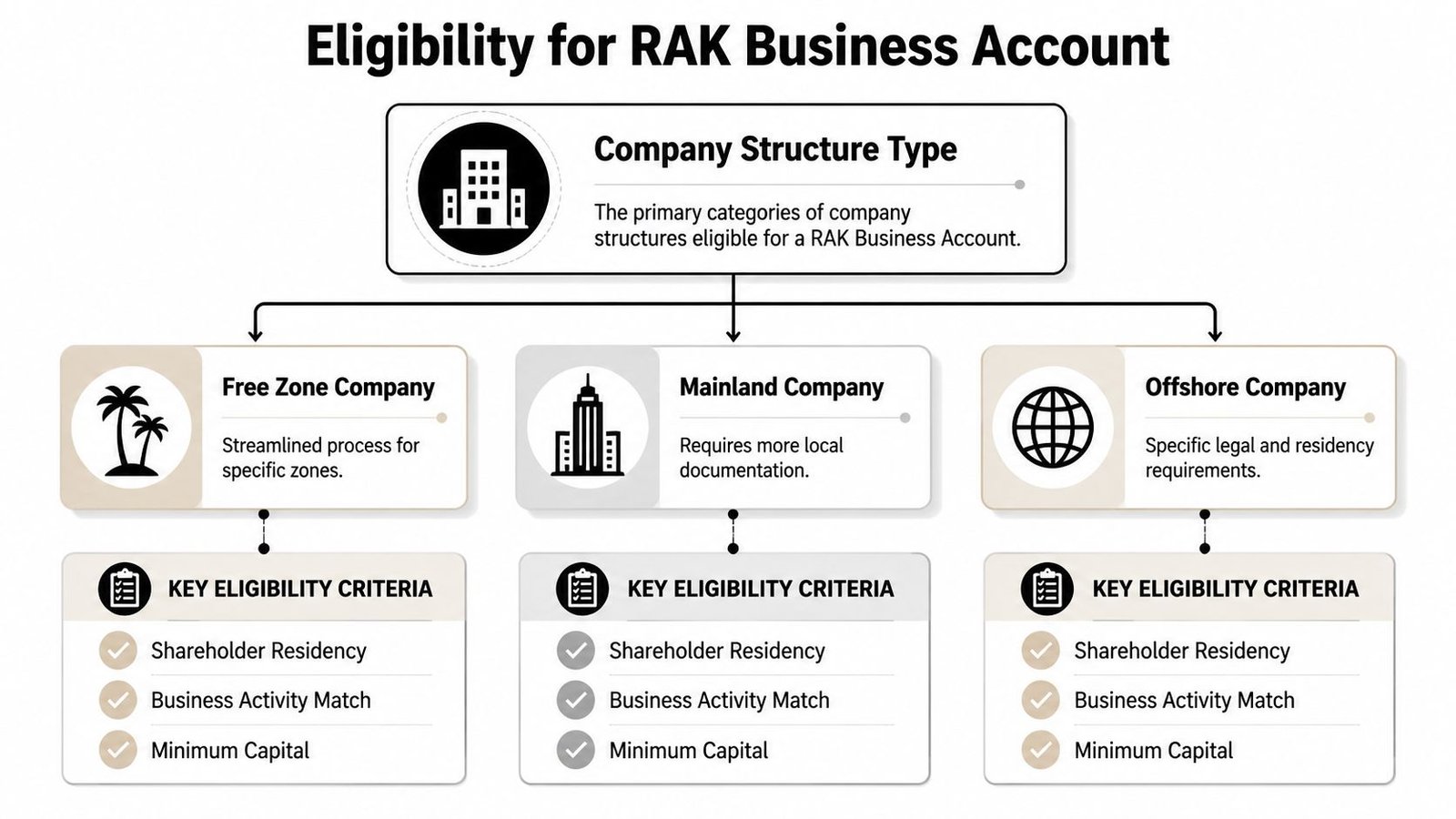

Which company structures usually qualify

Most applications fall into three broad groups: mainland companies, free zone companies, and offshore companies. A mainland company is a business licensed by the relevant local authority to operate in the domestic UAE market. A free zone company is a business incorporated in a special economic zone with its own authority and rules. An offshore company is usually a holding or international structuring vehicle with a different risk profile in banking.

All three may be considered, but they aren't assessed in the same way. The legal form matters less than whether the bank can understand ownership, activity, and expected fund flows.

Does your jurisdiction affect approval speed

Yes. Jurisdiction can affect both speed and smoothness.

For example, RAKEZ, the Ras Al Khaimah Economic Zone, says its partnership with RAKBANK allows clients to open business accounts more quickly by sharing verified e-KYC data through a blockchain platform (RAKEZ and RAKBANK partnership announcement). That tells you something useful. Banks are often more comfortable when the company comes through a setup channel they already recognise and can digitally verify.

If you're outside that ecosystem, don't assume rejection. But do expect more manual review. A free zone company formed in Ras Al Khaimah under a known partner route may feel straightforward. A service company from another zone with overseas shareholders and no trading history may face a slower review even if the paperwork is technically complete.

Digital onboarding helps after the bank is comfortable with the profile. It doesn't remove the need to pass the bank's internal risk checks.

What do banks look at beyond the licence

Founders often think eligibility means one thing: "I have a company, so I qualify." Banks look deeper than that.

They usually assess points like these:

- Shareholder profile. The bank wants to know who owns the company, where they live, and whether the ownership chain is easy to verify.

- Business activity match. Your licence activity should match what you say you'll do, what your website says, and what your first payments are likely to look like.

- Substance. Substance is the evidence that the business is real. That can include office arrangements, contracts, supplier relationships, a functioning website, or a clear plan for how the company will earn money.

- Signatory presence. Some account openings still require personal attendance by a shareholder or account signatory, especially where the file needs closer review.

A practical self-check before you apply is simple. Can you explain the company in plain English, identify the owners, and show how money will enter and leave the account? If the answer is vague, the bank will probably slow the file down.

Gathering Your Essential Application Documents

Which corporate documents are usually required

The process of handling most files often dictates their ease or difficulty. The bank isn't collecting paperwork for formality. It is checking whether the company legally exists, whether the signatory has authority, and whether the proposed activity makes sense.

A typical document set commonly includes the trade licence, Memorandum of Association (MoA) or Articles of Association (AoA), certificate of incorporation, and a board resolution authorising the account opening where relevant. The MoA is the company document that sets out ownership and powers. The AoA is the rules document that covers internal governance.

According to guidance on RAK business account openings, the main failure point in UAE corporate account opening is weak documentary consistency. The same guidance notes that banks commonly require the trade licence, MoA or AoA, certificate of incorporation, board resolution, and personal identification documents, and that mismatches between the licensed activity and expected transactions can trigger follow-up requests or rejection.

What personal documents do shareholders and signatories need

Banks also want to identify every person who owns or controls the company. That means passport copies, Emirates ID where available, residence visa copies where available, and proof of address for signatories or shareholders depending on the file.

A signatory is the person authorised to operate the account. A Ultimate Beneficial Owner (UBO) is the actual individual who ultimately owns or controls the company, even if another company sits in the ownership chain.

Use this checklist before submission:

- Passport copies. Make sure each passport is clear, valid, and matches the spelling used in company documents.

- Visa and Emirates ID. If a shareholder or signatory is UAE-resident, provide current copies. If the residency file is in progress, prepare to explain that.

- Proof of address. The bank may ask for recent personal or company address proof depending on the profile.

- Authority evidence. If one manager is opening the account for the company, the paperwork must clearly show they have authority to do so.

The bank reads your file as one story. If names, addresses, activities, or ownership percentages shift from document to document, that story stops making sense.

Why do banks ask for business proof and source of funds

This part surprises new founders. A zero-balance or startup-friendly account doesn't mean low compliance.

Banks often ask for supporting items such as:

- A short business plan. This can be simple. What do you sell, who are your clients, where will payments come from, and what countries will you deal with?

- Contracts, proposals, or invoices. These show that your company activity is not theoretical.

- Existing bank statements or financials where available. A new company may not have these, but if the shareholders run related businesses, context helps.

- Source of funds evidence. Source of funds is proof of where the company money or shareholder capital is coming from.

The strongest applications are not always the biggest. They are the clearest.

| Document category | Why the bank wants it |

|---|---|

| Corporate records | To confirm legal existence and authority |

| Identity documents | To verify owners, signatories, and control |

| Business support | To understand activity, counterparties, and expected transactions |

| Source of funds | To satisfy anti-money laundering checks |

The Bank Account Application Process Deconstructed

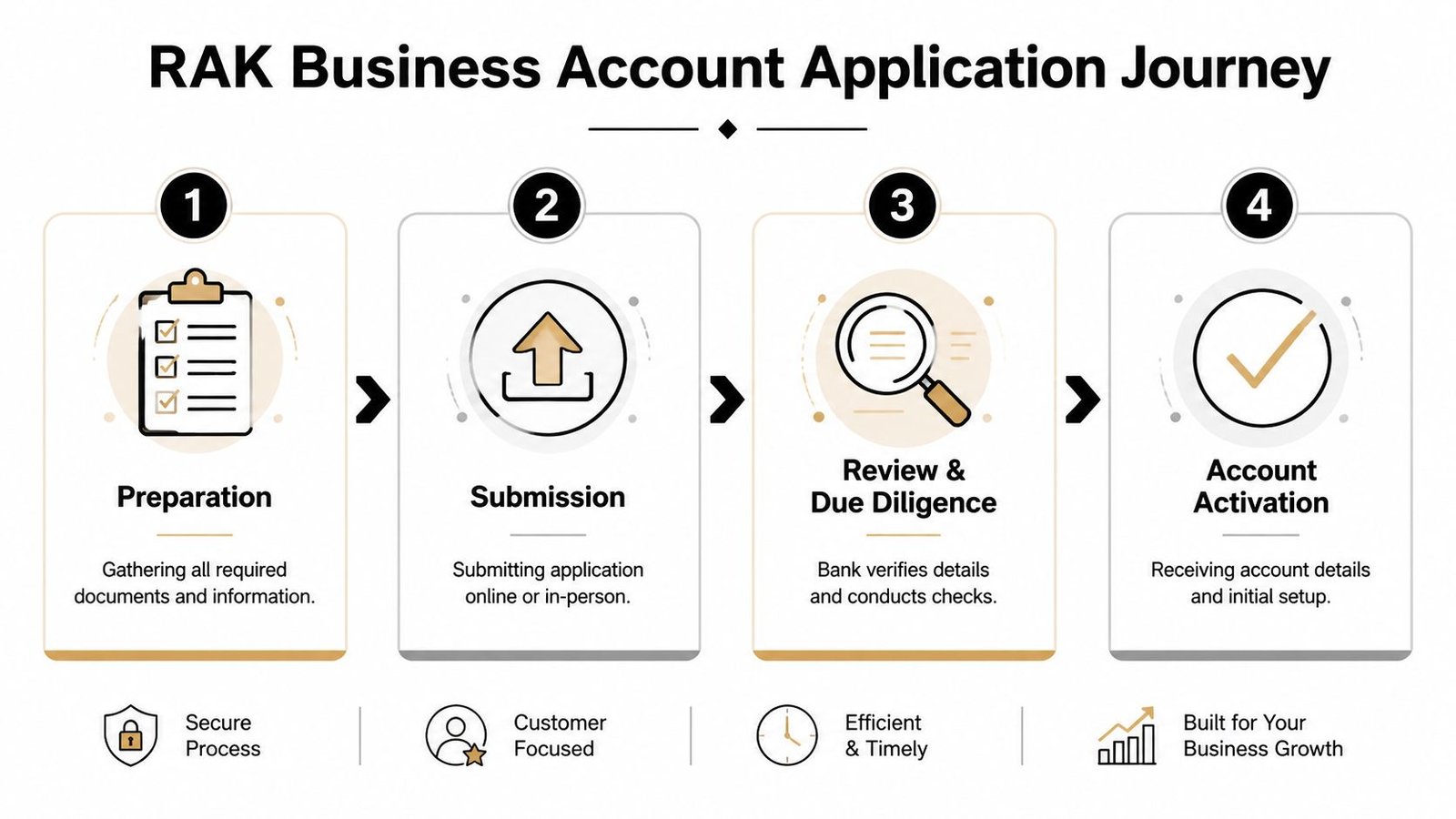

What happens before you submit the application

A founder sets up a RAK company on Monday and expects to invoice from a new bank account by Friday. Sometimes that happens. Often it does not, especially for new free zone entities with no trading history, overseas shareholders, or unclear transaction flows.

Approval starts before the form goes in. The bank wants a file that makes commercial sense on first reading, not a pile of documents that still need interpretation. If the licence says consultancy, the website says trading, and the shareholder profile suggests a different line of business, the file slows down before anyone discusses account features.

The first decision is account fit, not just account access. A startup may focus on the entry threshold, but the better question is whether the account still works once supplier payments, client receipts, low-balance months, and compliance reviews start. That is where many early banking choices become expensive.

A practical pre-submission pack usually includes:

- Corporate set. Licence, incorporation papers, constitutional documents, and signing authority documents where required.

- Ownership summary. A clean chart showing shareholders, UBOs, and authorised signatories.

- Business profile note. What the company does, who it will bill, where payments will come from, and which countries are involved.

- Operating evidence. Website, contracts, proposals, invoices, tenancy details, or proof that the business is already preparing to trade.

Banks review clarity as much as completeness. A smaller company with a consistent file often has a better approval chance than a larger one with unanswered questions.

How is the application submitted

The route depends on the bank's current onboarding process and the risk profile of the company. Some applications begin digitally. Others still require a branch interaction, original document check, or a video or in-person verification with the signatory.

Well-prepared files can move quickly. New companies should still plan for follow-up questions rather than assume a fast approval. In practice, the timeline stretches when the bank needs more comfort on ownership, source of funds, expected turnover, or cross-border activity.

Submission is only the start of review.

I tell clients to treat the application as the opening of a compliance file, not the end of an admin task. If you need the account for payroll, visa processing, merchant onboarding, or a key client contract, build in time for questions and re-submissions. That buffer matters more than the headline turnaround you may hear at the sales stage.

What happens during review and activation

After submission, the bank reviews the company on four practical points. Who controls it, what it does, how money will move, and whether that pattern is credible for the licence and shareholder profile.

Expect questions such as:

- What does the company sell

- Who are the expected clients or counterparties

- Which countries will funds come from or go to

- Why was the UAE entity set up in this structure

- Who will run the account day to day

- What is the expected monthly activity in the first few months

This is also where approval probability becomes more realistic. A local service company with resident shareholders, a simple ownership chain, and UAE-based clients is easier for a bank to get comfortable with. A newly formed free zone company with foreign ownership, high expected turnover, and payments involving multiple jurisdictions can still be approved, but the bank usually asks for more support and takes longer to get there.

Activation does not end the process either. Early account use is often monitored closely. If the first transactions do not match the activity described in the application, the bank may ask more questions, delay transfers, or restrict services until it is satisfied. That is why the opening explanation needs to match the way the business will operate in real life.

Other UAE banks may suit some RAK companies better. The right choice depends on approval odds, ongoing charges, transaction pattern, and how much compliance attention the business is likely to attract in its first year.

Choosing the Right Account Not Just the Cheapest One

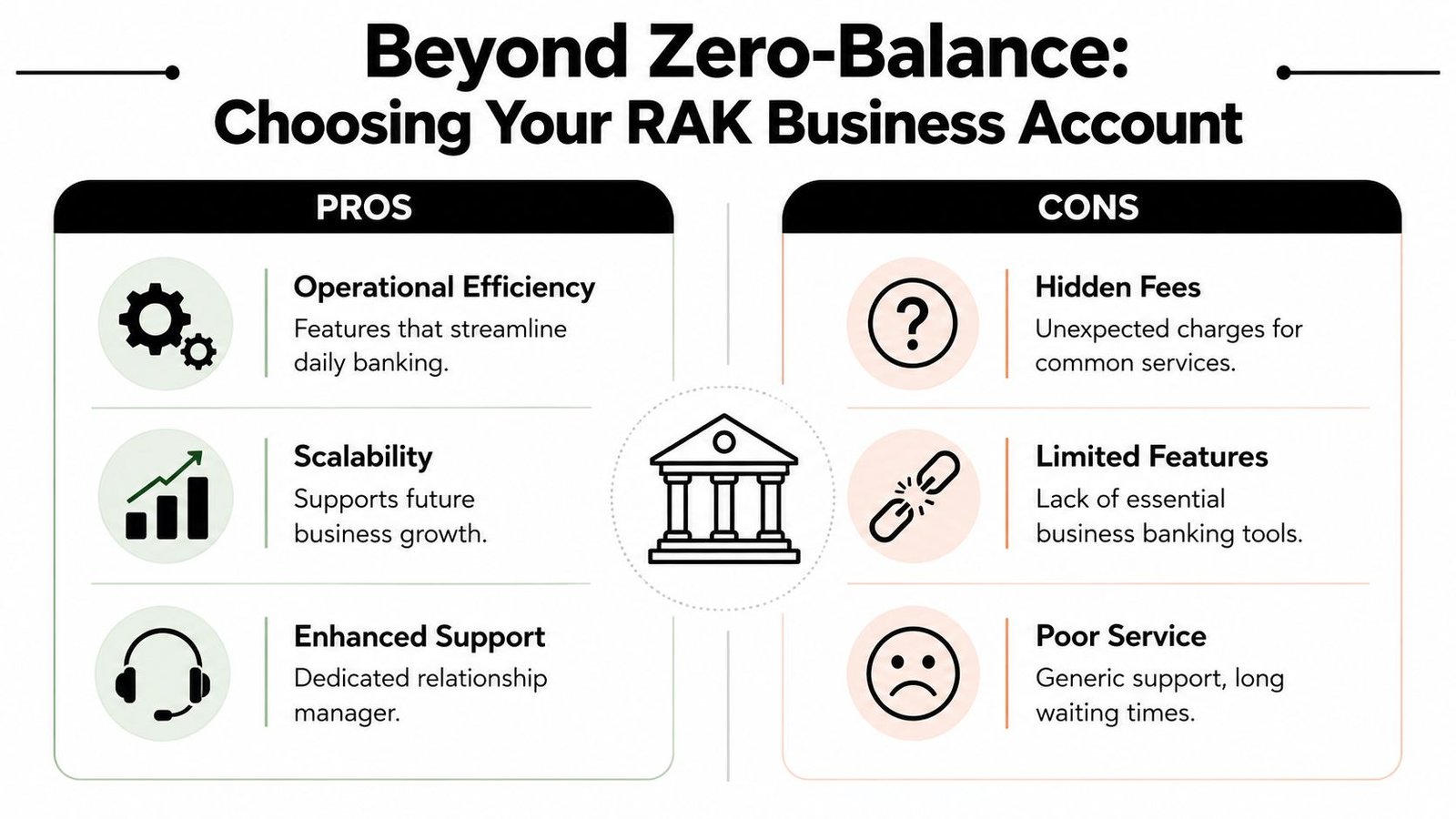

Is a zero-balance account always the best option

Not always. It's often the best marketing hook, but not always the best operating decision.

A startup founder hears "zero balance" and thinks the account will stay cheap and friction-free. What matters more is how the account behaves once the company starts making transfers, asking for cheque books, issuing payroll, or running low balances between projects.

What operating costs catch founders by surprise

This is the part many generic guides skip. The opening requirement and the operating economics are not the same thing.

RAKBANK's own schedule of charges states that a minimum monthly average credit balance of AED 250,000 is required at account level to avoid a cheque book issuance fee for business banking customers (RAKBANK business banking charges). That doesn't mean every startup needs to hold that balance. It means founders should stop evaluating the account only by the entry-level threshold.

If your business is lean, seasonal, or project-based, questions like these matter more than the headline:

| Operational question | Why it matters |

|---|---|

| Will the balance stay stable each month | Falling below thresholds can trigger charges on some services |

| Do you need cheque facilities | Traditional tools may carry costs founders didn't budget for |

| Will you receive international payments early | Cross-border activity often brings closer scrutiny and practical banking needs |

| Are you pre-revenue | A low-friction account may be a better fit than a feature-heavy one |

The cheapest account to open can become the wrong account to operate.

How should you choose the account that fits your stage

A sensible choice usually follows the company's real cash pattern.

For an early startup or solo founder, the better account is often the one that keeps compliance manageable and doesn't punish a modest working balance. For a growing SME with regular inflows and more formal supplier relationships, a standard current account may be worth it if the account features match daily operations.

Use this simple lens:

- Early-stage service company. Prioritise low maintenance burden, digital access, and an account profile that doesn't assume large idle balances.

- Trading or contracting SME. Prioritise transaction handling, documentary support, and day-to-day banking tools.

- Holding or cross-border structure. Prioritise clarity of ownership and realistic expectations about review depth, not speed alone.

The right decision isn't about chasing the lowest barrier. It's about choosing a setup your company can sustain once the first month of formation is over.

Why Applications Fail and How to Ensure Success

A common pattern looks like this. The company is incorporated, the licence is issued, the founder expects the bank account to follow, and then the file sits in review for weeks. In many cases, the problem is not one major red flag. It is a set of small inconsistencies that make the bank unsure how the business will operate in practice.

What usually causes rejection or delay

Banks want a file that is easy to verify and easy to justify internally. Delays usually start when the source of funds is vague, the licence activity does not match the business model, shareholder records conflict across documents, or the company cannot explain expected clients, payment flows, and counterparties in a practical way.

Many free zone companies frequently misinterpret the process. Incorporation proves the company exists. It does not prove the bank will be comfortable with the account profile, transaction pattern, or ownership structure.

Operational reality matters as much as paperwork. A startup that says it will receive overseas client payments, pay multiple suppliers, and maintain only a minimal balance should expect closer review than a simple local service company with a clear owner and straightforward invoicing pattern. Founders often focus on getting approved, but the better question is whether the account will remain workable once monthly charges, minimum balance rules, transfer fees, and compliance reviews start affecting daily operations.

How do you improve your chances from day one

Prepare the file the way a compliance officer will read it. Keep the ownership structure clear, match the licence activity to the business model, prepare a short summary of what the company sells and who pays it, and answer due diligence questions in plain terms.

It also helps to show that the business is commercially coherent. If the company is pre-revenue, explain how it is funded and when income is expected. If international transfers are part of the model, describe the countries involved and why. If the company is a holding structure or has multiple shareholders, make sure every supporting document points to the same ownership story.

Good preparation improves approval odds. It also reduces the risk of opening an account that becomes expensive or restrictive to use after approval.

If the profile is more complex, professional support can help keep the file aligned. Inpro Corporate Services L.L.C. provides company formation, banking support, visa processing, and compliance assistance in the UAE, which is useful when the bank application depends on the licence, residency status, and shareholder documents matching from the start.

The goal is a clean, credible application that can stand up to review on the first submission.

Not sure where to start? Book a free strategy call with the Inpro Corporate Services L.L.C. team if you want help aligning your UAE company setup, shareholder documents, and bank application before submission.