Most UAE compliance failures don't happen because founders ignore the rules. They happen because businesses treat compliance as a one-time filing exercise, even though 73% of some strategic enterprise risk management frameworks in the UAE failed due to lack of cultural integration, not regulatory ignorance according to 2026 research published on ScienceDirect.

Risk management compliance in the United Arab Emirates is the day-to-day system a business uses to identify risk, meet legal obligations, document decisions, and keep operating without disruption. If you're setting up in Dubai, Abu Dhabi, Sharjah, or a free zone, that system starts earlier than most founders expect. It begins when you choose your licence, structure your shareholding, prepare for banking, and decide who owns compliance tasks internally.

Table of Contents

- Your Introduction to UAE Compliance

- What Is Risk Management Compliance

- Key UAE Regulatory Frameworks You Must Know

- The Core Components of an Effective Program

- Your Implementation Roadmap From Setup to Scale

- Three Compliance Pitfalls That Stall UAE Businesses

Your Introduction to UAE Compliance

Risk management compliance is the organised process of identifying business risks, applying the right controls, and meeting UAE legal and regulatory duties in a way that keeps the company stable and credible. In the United Arab Emirates, that isn't just a legal concern. It affects bank onboarding, licence renewals, tax readiness, visa processing, audit submissions, and how confidently partners deal with your company.

For founders, the main shift in 2026 is practical. Compliance isn't a folder you prepare once the company is live. It's part of setup itself. Your company structure affects tax treatment. Your business activity affects banking questions. Your document trail affects how quickly you can answer requests from banks, free zone authorities, or government bodies.

A good compliance approach makes the business easier to run. Teams that organise records early, assign ownership, and review risks as operations change usually face fewer surprises. Teams that wait for a renewal notice, a bank query, or a tax deadline end up fixing preventable problems under pressure.

Good risk management compliance should make the business calmer, not slower.

That matters in the UAE because the system is regulated but workable. If you build around core operational touchpoints, licensing, immigration, banking, accounting, tax, and reporting, compliance becomes part of how the company runs from day one.

What Is Risk Management Compliance

What is a risk for a UAE business

A risk is anything that could interrupt your ability to operate, meet a legal duty, protect funds, or keep the business in good standing. In the UAE, that can be obvious, such as missing a renewal, or less obvious, such as using the wrong activity description, keeping weak transaction records, or failing to document who approved a payment.

A founder in Dubai might think risk means fraud or cyber issues only. In practice, risk also includes commercial and administrative exposure. If your visa file doesn't match your licence activity, if your accounting records are incomplete, or if your bank can't understand your business model, the result can still be a compliance problem.

What does management mean in practice

Management is the system you use to reduce those risks before they become expensive. It means deciding who checks what, what documents must exist, what gets reviewed monthly, and what gets escalated when something looks unusual.

For a small company, this doesn't need a large department. It often starts with a founder, finance lead, operations manager, or outsourced adviser using a simple control structure such as:

- Owner assignment: One person owns licence renewals, one owns finance records, and one owns employment files.

- Document rules: Every contract, invoice, bank transfer support file, and immigration record is stored in one organised system.

- Review rhythm: The team checks upcoming deadlines, unusual transactions, and open authority requests on a fixed schedule.

- Escalation path: If a supplier, client, or payment creates concern, someone knows who reviews it and what happens next.

What doesn't work is relying on memory. Founders often carry too much in their heads during the first year. That feels efficient until the business adds staff, opens a second revenue stream, or starts dealing with larger counterparties.

How does compliance apply to freelancers and SMEs

Compliance is meeting the rules that apply to your actual business activity, legal structure, and operating footprint. A freelancer in a free zone, a consultancy in Abu Dhabi, and an e-commerce company selling into the mainland all face different questions, even if all three are small.

This is why risk management compliance is a business advantage, not just a cost. It helps answer basic but high-stakes questions quickly:

| Business moment | Compliance question |

|---|---|

| Licence setup | Does the chosen activity match what the business will really do? |

| Banking | Can the business explain source of funds and expected transactions clearly? |

| Hiring | Are employment and immigration records aligned and current? |

| Tax and accounting | Are books, invoices, and supporting records ready for review? |

| Growth into mainland Dubai | Is the structure allowed to operate where it plans to sell? |

A 2023 study created the first index assessing how listed UAE banks comply with risk management disclosure standards across local and international requirements, showing how seriously the country treats structured risk governance in financial institutions, as detailed in the 2023 UAE banking compliance study on EconStor. Founders don't need to copy a bank's framework, but they should recognise the direction of travel. Regulators, banks, and counterparties expect evidence, not assumptions.

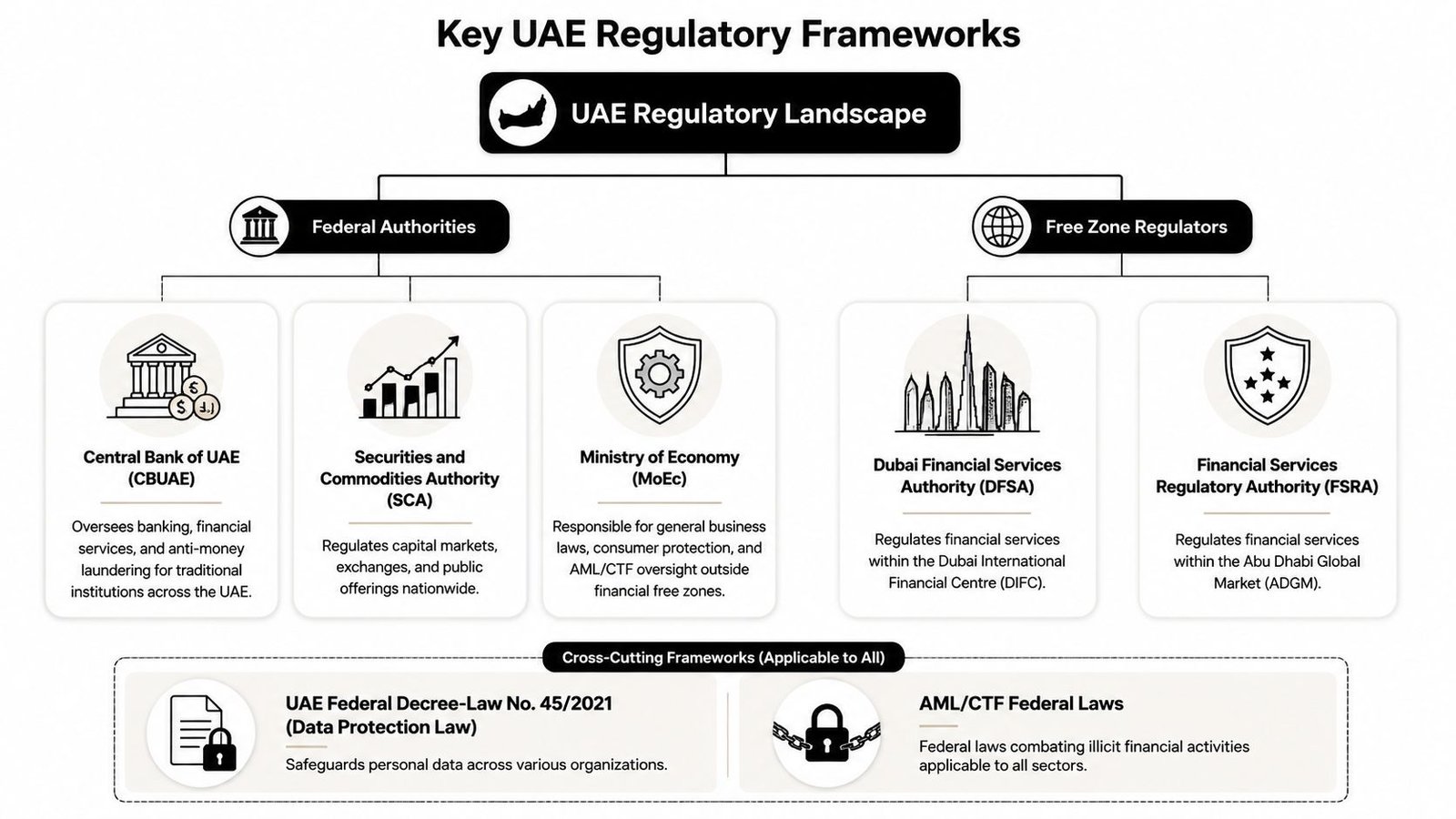

Key UAE Regulatory Frameworks You Must Know

Which authorities matter first

The UAE regulatory map becomes easier once you separate federal authorities from free zone regulators. Federal bodies apply across the country in their own areas. Free zone regulators apply within specific jurisdictions such as the Dubai International Financial Centre and Abu Dhabi Global Market.

This visual helps place the main players.

The names that founders most often encounter include the Department of Economy and Tourism or Department of Economic Development in the relevant emirate for mainland licensing, the Federal Tax Authority for tax registration and administration, and sector regulators where activities are regulated. In financial services, the Central Bank of the UAE, the Dubai Financial Services Authority in the Dubai International Financial Centre, the Financial Services Regulatory Authority in Abu Dhabi Global Market, and the Securities and Commodities Authority all matter depending on where and how the firm operates.

How do corporate and licensing rules affect compliance

Corporate compliance starts with getting the legal vehicle and activity right. A mismatch at formation usually creates problems later in banking, contracts, VAT treatment, employee visas, or expansion.

One area founders often misunderstand is the line between free zone activity and mainland activity. Under Dubai Resolution No. (11) of 2025, free zone companies can operate on the mainland if they obtain a branch licence valid for 1 year and renewable at AED 10,000 per year, or a temporary permit for up to 6 months at AED 5,000, with existing businesses given one year from the effective date to comply, according to KPMG's note on Dubai Resolution No. (11) of 2025.

There is also a hard boundary if a company ignores the licensing rules. Conducting economic activity in Dubai outside free zones without a mainland-licensed entity can trigger fines of up to AED 100,000, and some activities remain prohibited for free zone branch offices on the mainland, as explained by Al Tamimi on doing business in mainland Dubai through a free zone entity.

Practical rule: Choose the structure for where you will actually trade, not just where the setup fee looks lower.

What do tax and financial crime rules require

Tax compliance is now part of basic company hygiene. Under the UAE corporate tax framework effective 2026, every entity must register with the Federal Tax Authority, assess its tax position, maintain proper financial records, and determine whether it qualifies for free zone tax treatment, as outlined in Flyingcolour's guide to UAE free zone corporate tax and AML compliance. Free zone status changes tax treatment. It does not remove compliance duties.

Mainland and free zone businesses also face different tax outcomes depending on how they operate. Mainland companies registered with the relevant Department of Economic Development face a 9% corporate tax rate on profits exceeding AED 375,000 annually and a standard 5% VAT requirement, while free zone companies operating exclusively within their zone may be exempt provided they do not conduct business directly in the mainland without the required structure, according to Ibara Group's mainland versus free zone guide.

Financial crime controls sit alongside tax. For regulated sectors, Anti-Money Laundering duties are active and operational. That includes registration where applicable, appointing a compliance officer, monitoring transactions, and reporting suspicious activity to the authorities.

Where do labour and operational controls fit

Founders often separate immigration, labour, accounting, and audit into different admin buckets. That creates blind spots. In reality, these are linked operational controls. If your staffing records are inconsistent, if payroll support is weak, or if contracts aren't stored properly, the issue often surfaces later during audit, tax review, or banking queries.

Free zone audit rules are a good example. In UAE free zones, statutory audit compliance is mandatory, all entities must submit annual audited financial statements, and failure can prevent licence renewal or continued operations, as detailed in this UAE free zone audit requirements guide. The same source notes that full International Financial Reporting Standards are generally required across major free zones, with limited exceptions for International Financial Reporting Standards for SMEs in some jurisdictions.

For founders, the takeaway is simple. Compliance is not split between legal, finance, and HR. The business has one operating record, and regulators examine it from different angles.

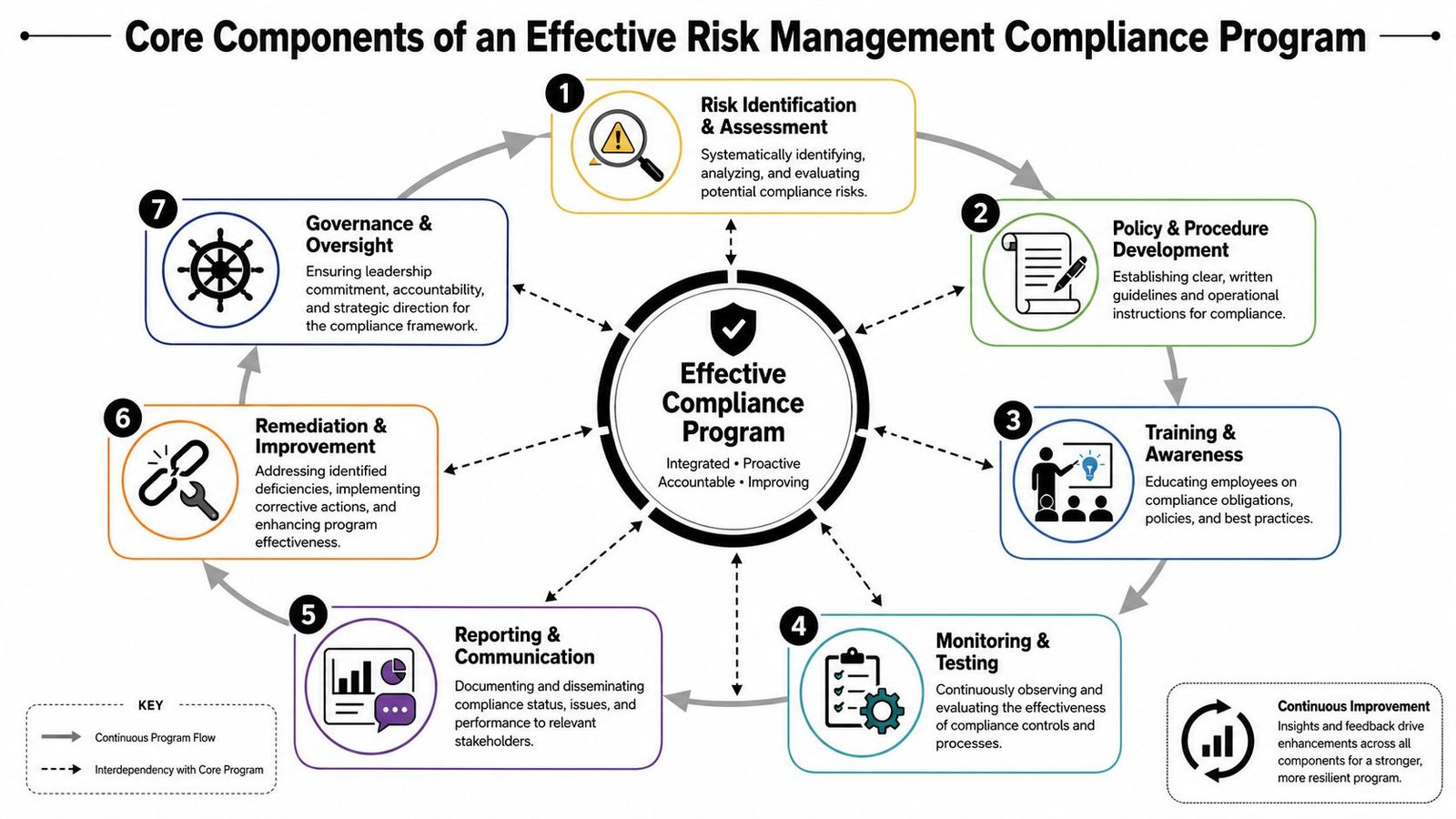

The Core Components of an Effective Program

A working compliance program is less like a policy binder and more like an operating loop. It tells people what matters, who owns each task, what evidence must exist, and how the business reacts when conditions change.

The goal isn't perfect paperwork. The goal is a business that can prove what it does, explain why it does it, and correct problems early.

Who owns the program

Governance is the assignment of responsibility. In a founder-led business, that usually means one accountable owner at leadership level, then named owners for finance, immigration, client onboarding, and document control.

That matters because some obligations are personal in effect even if they sit within the company. In regulated sectors, AML duties are strictly enforced and include UAE AML registration where applicable, appointment of a compliance officer, ongoing transaction monitoring, and suspicious activity reporting, as described in the earlier linked tax and AML guidance. If no one owns those steps, they don't happen consistently.

A light governance model often works best for SMEs:

- Founder or director: Owns risk decisions, approves policy, signs off on escalations.

- Finance lead or accountant: Keeps books, reconciliations, invoice support, and tax files in order.

- Operations or HR lead: Maintains visa, employment, and document validity records.

- External specialist when needed: Reviews gaps in banking files, AML setup, tax registration, or audit readiness.

How do policies controls and reporting connect

Policies are the written rules. Controls are the actions that prove the rules are being followed. Reporting is the evidence that lets management see whether the controls are working.

Here's where many SMEs get stuck. They write a policy copied from a template, but they don't convert it into a daily action. A policy may say client due diligence is required. The control is a checklist before onboarding, document capture, and approval before the first invoice. The reporting is a monthly review of exceptions, pending files, and unusual transactions.

This video gives a useful practical frame for how program elements work as a cycle in real organisations.

A simple example for a UAE consultancy:

| Program element | Real action |

|---|---|

| Policy | No client is onboarded without signed engagement terms and identity records |

| Control | Operations checks documents before account creation |

| Monitoring | Finance reviews first payment against expected activity |

| Reporting | Director receives a short monthly exception list |

What does good monitoring look like

Monitoring is where compliance becomes real. It means someone checks whether records are complete, whether transactions fit the profile of the business, whether suppliers have changed, and whether a new service line creates a new risk.

The strongest SME programs are usually simple and repetitive. They rely on calendars, approval logs, reconciliations, document naming standards, and short management reviews. They don't rely on a founder remembering everything after midnight.

What doesn't work is treating compliance as a file that only appears at renewal time. Businesses change faster than annual forms do. New staff join. Payment patterns shift. A free zone company starts pitching mainland clients. A dormant entity begins trading. The controls need to move with the business.

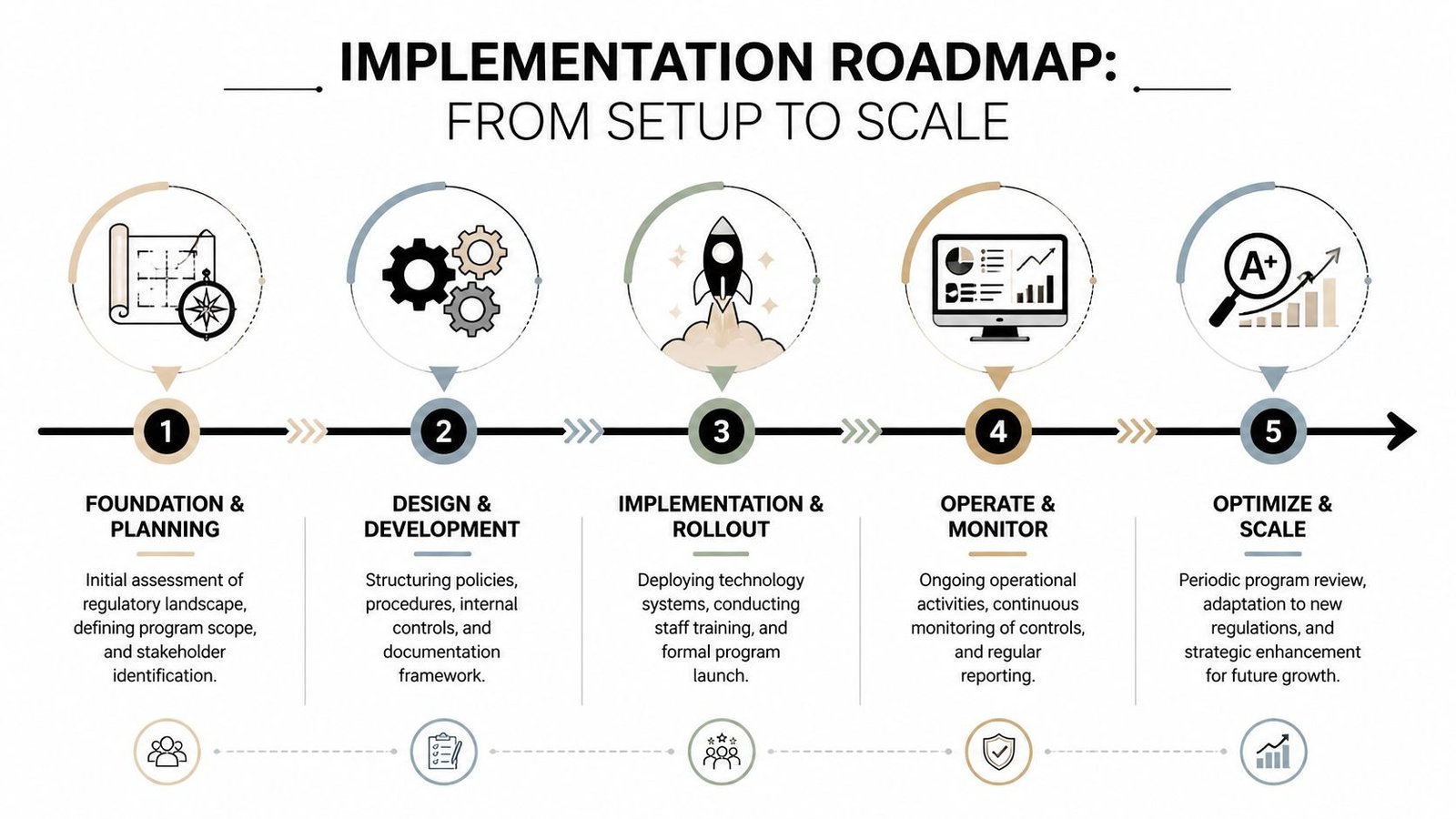

Your Implementation Roadmap From Setup to Scale

The most useful way to build risk management compliance is to attach it to business milestones. Founders already understand setup, visas, banking, accounting, and growth. Compliance should sit inside each stage, not beside it.

A structured roadmap matters because point-in-time checks often miss operational gaps. In 2025, UAE third-party risk management reviews found that only 61% of controls were fully met, according to this UAE third-party risk management review benchmark shared by a UAE compliance practitioner. That doesn't mean small businesses need enterprise software from day one. It means sequence matters.

What should happen before you incorporate

Start with activity, footprint, and counterparties. What will the business sell, where will it sell, who will pay it, and which jurisdictions will it touch? Those answers shape the licence type, banking story, tax position, and document set.

At this stage, founders should pin down:

- Actual operating model: Free zone only, mainland trading, cross-border services, holding structure, or mixed activity.

- Decision rights: Who can approve payments, sign contracts, and respond to authority queries.

- Record design: Where contracts, shareholder documents, passports, corporate records, and finance files will be stored.

- Regulated exposure: Whether the business falls into an activity that triggers extra AML, reporting, or sector requirements.

This early discipline saves time later. Banks usually want a coherent story. So do auditors, tax authorities, and free zone compliance teams.

What changes once the licence is issued

Once the company exists, compliance becomes operational. The licence is only the start. Now the business needs document discipline, immigration alignment, bank-readiness, and a workable accounting process.

A practical post-incorporation checklist looks like this:

- Corporate records: Keep licence, incorporation documents, shareholder records, office documents, and authorised signatory evidence current and accessible.

- Visa and employment files: Match employee roles, permits, and internal records. If details drift, the clean-up usually happens during a deadline window.

- Banking support pack: Prepare contracts, invoices, business plan material, expected transaction patterns, and proof of source of funds in an organised file.

- Accounting setup: Record revenue and expenses properly from the first transaction. Retroactive bookkeeping is slow and risky.

- Tax readiness: Register where required and keep financial records in a form that supports your filing position.

If the business can't explain who pays it, why they pay it, and where the paperwork sits, banking and compliance friction usually follows.

How should operations mature as the business grows

As the business scales, static checklists stop being enough. New suppliers, outsourced services, expanded geographies, and added product lines create fresh risks. The answer isn't more forms. It's a tighter review rhythm.

A sensible growth-stage cadence often includes quarterly management review, monthly finance control checks, and event-based reassessment when something material changes. That could be a new shareholder, a move from services into trading, an expansion from Sharjah into Dubai mainland, or a shift from local invoicing to higher-volume cross-border payments.

This is also where founders need to pay attention to external dependencies. If you rely on payment providers, outsourced accountants, introducers, fulfilment partners, or nominee arrangements, those third parties become part of your compliance exposure. Review them like business risks, not as admin afterthoughts.

Another mature habit is linking compliance to operating services directly:

| Business function | Ongoing compliance action |

|---|---|

| PRO and government processing | Track expiries, approvals, and document consistency |

| Banking | Review unusual payments, maintain support files, update profile when the model changes |

| Accounting and VAT | Reconcile books, preserve invoice support, prepare for tax and audit reviews |

| Hiring and HR | Keep employee records aligned with permits and company structure |

| Expansion planning | Recheck whether the current licence and jurisdiction still fit the actual activity |

This is the part many founders appreciate once the company is moving. A clean compliance system reduces interruptions. It shortens response time when a bank asks a question, when an auditor requests support, or when the company needs to prove substance and control to an investor or partner.

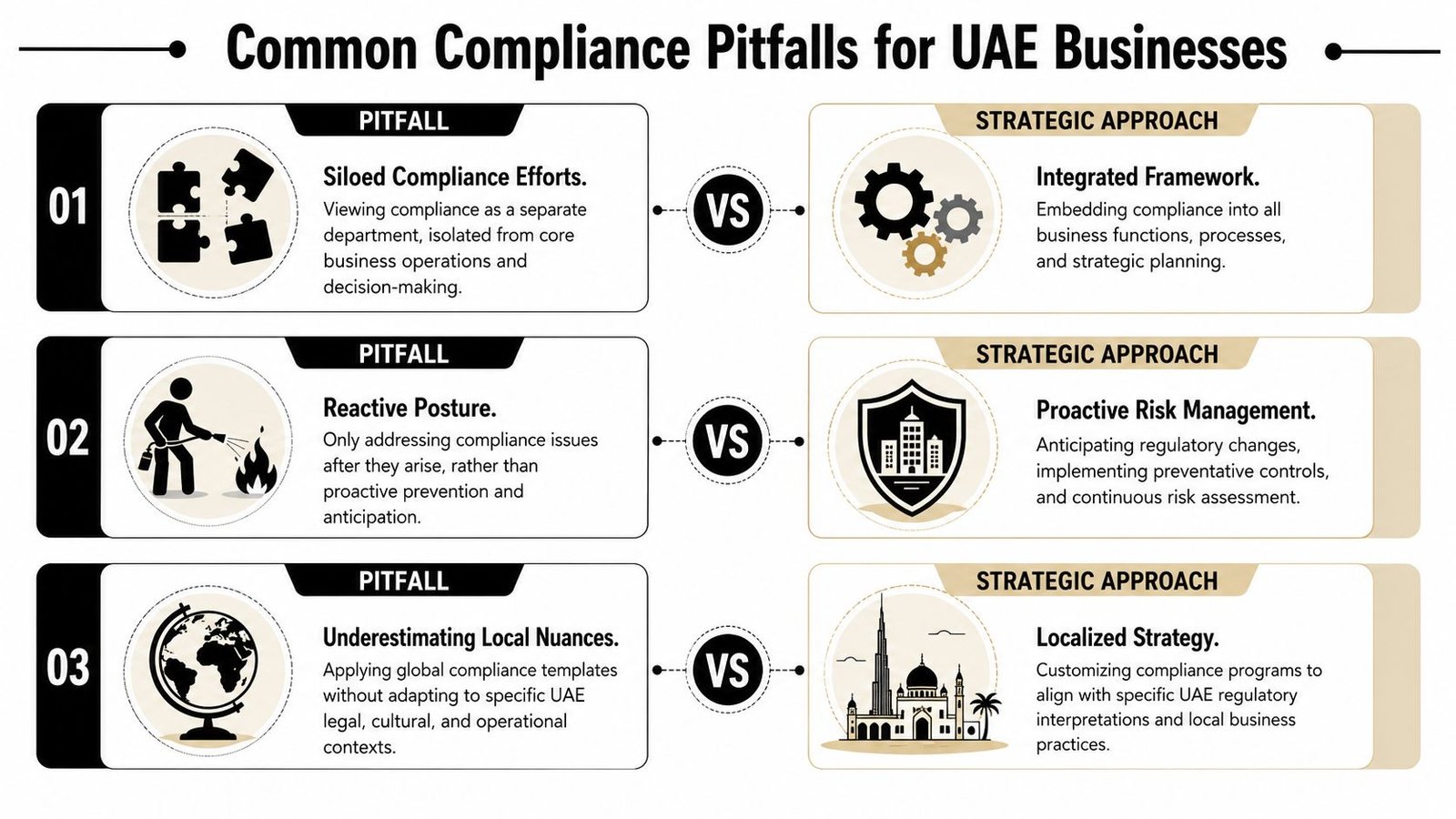

Three Compliance Pitfalls That Stall UAE Businesses

The biggest mistakes are usually mindset mistakes. A business can have the right licence, decent advisers, and enough budget, then still create avoidable exposure because the team treats compliance as occasional admin.

Why does checklist thinking fail

The checklist mentality says compliance happens at setup, renewal, audit time, or when a bank asks for more papers. That feels efficient because it keeps admin out of the way. It usually fails because the business changes in between those moments.

The earlier ScienceDirect research found that 73% of some UAE strategic enterprise risk management frameworks failed because of poor cultural integration rather than regulatory ignorance. That finding matters because it shows the issue isn't usually lack of access to rules. It's that teams don't build the rules into decisions, habits, and accountability.

A better approach is behavioural. Put risk ownership into role descriptions. Review open issues regularly. Ask simple operating questions when anything changes. What new risk did this client, supplier, product, or market create?

What happens when compliance sits in one silo

Some companies push all compliance into one person or one external firm, then assume the rest of the business is covered. It rarely is. Finance sees payment patterns. HR sees staffing inconsistencies. Operations sees document gaps. Founders see commercial pressure that can tempt shortcuts. If those views stay separate, no one has the full picture.

This is why integrated risk management compliance works better than isolated box-ticking. The goal isn't to turn every employee into a compliance officer. It's to make each function responsible for the records and controls that belong to its work.

A simple fix is to give each team one visible responsibility:

- Finance owns evidence: invoices, reconciliations, payment support.

- Operations owns validity: renewals, licences, permits, organised records.

- HR owns alignment: employee files, role consistency, document updates.

- Leadership owns escalation: decisions on exceptions, higher-risk clients, and structural change.

A culture of compliance isn't built through slogans. It shows up when staff know what to check before they click approve.

Why do founders misread local complexity

The UAE is business-friendly, but it isn't uniform. Dubai mainland, a free zone in Dubai, Abu Dhabi Global Market, and a logistics-focused free zone can all operate differently in practice. A template from another country won't capture those local differences.

Founders often assume that if a business is small or early-stage, the rules will be simple. Sometimes they are. Sometimes the opposite is true. A lean structure with cross-border clients, outsourced operations, and free zone status can create more compliance questions than a larger but simpler local trading company.

The right response is not fear. It's specificity. Match the activity to the licence. Match the records to the activity. Reassess when the business changes. Treat PRO, banking, accounting, tax, and immigration as one operating chain, because that's how problems tend to surface in real life.

Not sure where to start? Book a free strategy call with Inpro Corporate Services L.L.C. to map your UAE setup, compliance obligations, and operational next steps with a team that handles formation, visas, banking support, and ongoing regulatory admin.