You’ve probably already had this moment. Your company is active in the UAE, you’ve seen the headlines about corporate tax, and you know registration matters. But the immediate question is more basic and more urgent. What is your actual UAE corporate tax registration deadline, and what happens if you’ve treated it like something to sort out later?

That uncertainty is common, especially for founders juggling licensing, banking, payroll, visas, bookkeeping, and investor reporting at the same time. The problem is that corporate tax registration isn’t just another admin task. It’s the point where your legal structure, ownership records, licence history, and accounting setup all meet. If those pieces don’t line up, registration becomes slower, riskier, and more expensive than it needs to be.

In practice, the businesses that move through this cleanly are rarely the ones reacting at the last minute. They’re the ones that treat registration as a strategic checkpoint. They use it to confirm who owns the entity, which documents control, what their financial year-end is, and whether their current setup still makes sense in the UAE’s new compliance environment.

Table of Contents

- The UAE Corporate Tax Deadline Is Here Are You Ready

- Decoding the Deadlines Who Must Register and By When

- Your Step-by-Step EmaraTax Registration Workflow

- The Cost of Delay Penalties for Non-Compliance

- Beyond Registration Transitional Rules and Free Zone Myths

- Practical Tips for a Smooth and Timely Registration

- Frequently Asked Questions about Corporate Tax Registration

The UAE Corporate Tax Deadline Is Here Are You Ready

A founder approves invoices, signs a bank form, and assumes tax can wait until year end. Then the registration file stalls because the licence details, shareholder records, and authorised signatory data do not line up. That is how this deadline shows up in practice.

Here’s the shift. The UAE corporate tax registration deadline is not just an admin date on a compliance calendar. It is a checkpoint that tests whether your business is structured and documented properly inside the Federal Tax Authority system.

For many UAE businesses, the original setup was built for speed. Get the licence issued. Open the bank account. Start billing. That approach was workable before corporate tax became part of the operating reality. Now, weak records create friction early. A mismatched trade name, outdated passport copy, missing MoA, or unclear ownership trail can slow registration and expose bigger governance gaps you will have to fix later anyway.

The legal shift is already in place. Under Federal Decree-Law No. 47 of 2022, effective from 1 June 2023, the UAE introduced a corporate tax regime and moved tax registration into the normal lifecycle of running a company. For founders, the practical implication is straightforward. Setup quality now affects tax execution.

Practical rule: Treat registration as a diagnostic test for your company records.

That matters because registration drives decisions beyond the portal entry itself. It forces clarity on which entity is taxable, which records support that position, and whether your current structure still makes sense under the new rules. I have seen founders discover during registration that the operating company, holding company, and Free Zone entity were never documented with the discipline needed for tax compliance. Fixing that under deadline pressure is slower and more expensive than fixing it upfront.

Here’s your move. Before asking whether the form has been submitted, check the points that usually decide whether registration is clean or messy:

- Entity position: confirm exactly which UAE juridical person is registering

- Record accuracy: match the trade licence, MoA, shareholder details, and signatory information

- Authority chain: make sure the person handling the filing can legally act for the business

- Compliance path: confirm the financial year and basic post-registration reporting setup

Businesses that handle those points early usually get through registration with fewer surprises. Businesses that leave them unresolved tend to learn the same lesson late. The deadline is about filing, but it is also about whether the company behind the filing is properly set up for the new tax rules.

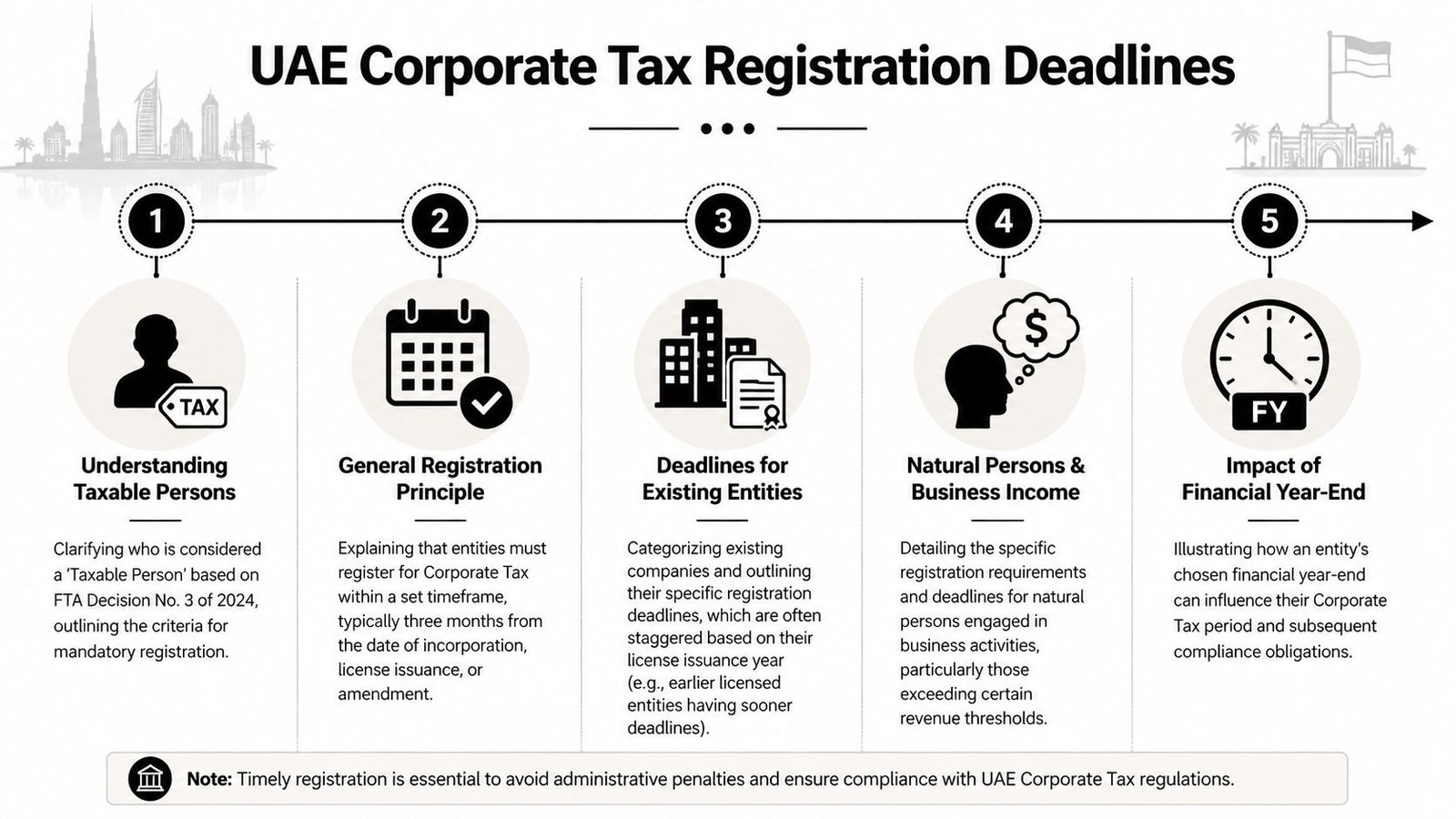

Decoding the Deadlines Who Must Register and By When

A common founder mistake shows up here. The team assumes the deadline starts when the business begins trading, invoices its first customer, or opens the bank account. For UAE corporate tax registration, the date that matters is usually tied to the entity’s legal existence, not commercial activity.

Here’s the shift. This deadline is not only an admin date to clear. It is a checkpoint that confirms whether you understand which entity sits inside the UAE corporate tax regime, and which legal document controls that position.

If your business is a resident juridical person in the UAE, the registration deadline depends on two things. First, whether the entity already existed on 1 March 2024. Second, if it did, the month the commercial licence was issued, regardless of the year of issue.

For entities that already existed as of 1 March 2024, the Federal Tax Authority applied a staggered deadline model. For entities incorporated, established, or otherwise recognised on or after 1 March 2024, the rule is simpler. Registration must be completed within 3 months of that legal date.

The deadline table for resident juridical persons

If your UAE entity existed as of 1 March 2024, use the commercial licence issue month below.

| Licence issue month | Registration deadline |

|---|---|

| January to February | 31 May 2024 |

| March to April | 30 June 2024 |

| May | 31 July 2024 |

| June | 31 August 2024 |

| July | 30 September 2024 |

| August to September | 31 October 2024 |

| October to November | 30 November 2024 |

| December | 31 December 2024 |

If the entity had no licence as of 1 March 2024, the deadline was 31 May 2024, as noted earlier.

For companies incorporated on or after 1 March 2024, apply the same 3 month rule across the usual entity types:

- Mainland entities: Register within 3 months of incorporation.

- Free Zone entities: Register within 3 months of incorporation.

- Offshore structures recognised under the UAE framework: Register within 3 months where that recognition creates the registration obligation.

A simple example shows how this works in practice. If a Free Zone company was incorporated on 16 June 2024, the registration deadline would be 16 September 2024.

Why founders should care about the legal date

Poor structuring starts to cost time.

I often see groups with a mainland operating company, a Free Zone holding vehicle, and an older licence file that does not line up neatly with the formation documents. When that happens, the registration question becomes bigger than “what is our deadline?” The key issue is “which entity are we registering, based on which legal record, and does that align with how the group operates?”

Here’s your move. Use the legal formation document as the starting point, then reconcile it against the licence, establishment record, and any amended constitutional documents before filing. If those dates or entity details do not match, fix that discrepancy first.

That approach reduces two common risks. The first is late registration because the business used the wrong reference date. The second is a technically incorrect registration that creates problems later, especially once return filing, Free Zone analysis, or group structuring questions come into play.

Your Step-by-Step EmaraTax Registration Workflow

A founder opens EmaraTax expecting a 20-minute admin task. Then the portal asks for ownership details, signatory authority, and legal records that do not match the trade licence on file. The delay starts before the first upload.

The practical point is simple. Corporate tax registration is not just a portal exercise. It is a checkpoint on whether the entity is documented the way it is set up and operated. Here’s the shift. Treat the filing as a test of legal and tax readiness, not a box-ticking task.

What to prepare before you log in

Start with a verified entity file. If the underlying records are clean, the portal flow is usually straightforward. If they are inconsistent, registration becomes slower and riskier.

Have these documents ready before anyone starts the application:

- Trade licence: Current, legible, and consistent with the legal entity being registered.

- Memorandum of Association: Or the equivalent incorporation or formation document.

- Owner and manager identification: Emirates ID and passport copies where applicable.

- Proof of address: Supporting the registered business details.

- Financial year-end decision: The portal asks for it, and it should align with how the business keeps its books.

Here’s your move. Reconcile the licence, formation document, authorised signatory evidence, and ownership records in one sitting. If the shareholder list in your internal files differs from the legal paperwork, fix that first. A fast submission with the wrong records is worse than a slower submission built on consistent documents.

How the portal flow works

Inside EmaraTax, the sequence is guided. You log in through the entity’s tax profile, go to Tax Registration, select Corporate Tax, complete the form, upload the supporting documents, confirm the financial year-end, and submit.

The form is not complex. The review risk sits in a few fields that founders often underestimate:

- Entity identity. The legal name, licence details, and registration numbers must match across the uploaded records.

- Authorised person details. The person filing or approving the application should be supported by the documents on file.

- Ownership disclosures. Incomplete or outdated beneficial ownership information can trigger avoidable follow-up.

- Financial year-end. This should match the accounting reality of the business, not just what is convenient to select in the portal.

That last point matters more than it seems. I often see businesses choose a year-end without checking how it affects first tax period mapping, reporting cutoffs, and group alignment. Registration is where a basic admin choice can turn into a larger clean-up later.

If you want to see the interface before filing, this walkthrough helps orient the process:

A controlled process works best. Build one final folder with the approved licence, MoA, IDs, ownership documents, and signatory support. Have one person do a line-by-line check of names, dates, and reference numbers against the application before submission.

Here’s your move. Use registration to confirm the business is structured and documented the way you intend to defend it later. That includes who owns it, who signs for it, what its year-end is, and which legal entity is carrying the tax obligation. That is the strategic value in getting this step right.

The Cost of Delay Penalties for Non-Compliance

A common founder scenario looks like this. The company is trading, contracts are moving, cash collection needs attention, and tax registration gets pushed behind sales, hiring, and banking admin. Then the deadline passes, and the business picks up a penalty that adds no commercial value at all.

The immediate exposure is straightforward. Late corporate tax registration can trigger a fixed AED 10,000 administrative penalty, as noted earlier.

That is the obvious cost. The more important issue is what the delay says about the company file.

In practice, late registration often appears with other weaknesses already sitting in the background. I usually see the same pattern. Ownership records are not fully aligned, signatory authority is unclear, bookkeeping has gaps, or licence details have changed without the supporting records being updated. Registration delay does not create those issues, but it often exposes them at the worst time.

Here’s the shift. The deadline is not just a filing date. It is a checkpoint that shows whether the legal entity, tax position, and operating records match the way the business operates.

That has practical consequences beyond the penalty itself:

- Government process delays: routine filings and approvals become slower when company records do not match across systems.

- Banking and compliance reviews: banks and payment providers look for clean corporate documentation and consistent entity information.

- Counterparty diligence: investors, larger customers, and distributors take a closer look when basic tax compliance is overdue.

- Internal drain on management time: founders end up chasing documents, approvals, and historical explanations instead of focusing on operations.

The trade-off is simple. A few hours spent registering properly is cheaper than paying a penalty and then cleaning up the records that the delay brought into view.

Here’s your move. Treat missed or approaching registration deadlines as a signal to fix the underlying file, not just submit the form. Confirm who holds the tax obligation, whether the records support that position, and whether the company structure still fits how revenue, contracts, and control are arranged. That is how you turn a compliance deadline into a useful control point.

Beyond Registration Transitional Rules and Free Zone Myths

A common founder mistake is treating Free Zone tax status as an exemption from registration. It is not.

Here’s the shift. Registration answers whether the entity is properly inside the UAE corporate tax system. The later analysis answers how that entity may be taxed. Those are separate decisions, and mixing them up creates avoidable risk.

Free Zone status does not remove the registration duty

Free Zone companies still need to register, including entities that expect to qualify for a 0% corporate tax outcome. The practical mistake I see is straightforward. Founders hear “0%” and assume “nothing to do.” In practice, the opposite is often true. The business needs a cleaner file, better activity mapping, and stronger evidence if it wants to support a preferred tax position later.

That is why registration should be treated as a checkpoint, not an admin form. If the company is in a Free Zone, this is the point to confirm what the entity does, where it earns income, who it contracts with, and whether its records support the position management plans to take.

A simple rule helps. Register first. Assess eligibility second.

The same discipline applies to dormant companies. No trading activity does not automatically mean no corporate tax compliance obligation. A dormant entity still exists legally, still has corporate records, and still needs its tax position assessed on the facts rather than assumption.

Transitional rules expose structural weaknesses

Some businesses entered their first tax period before they completed registration. That usually creates pressure in the wrong order. The team rushes to get the Tax Registration Number, then discovers the harder issues sit underneath. Year-end inconsistencies, old licence amendments, outdated shareholder records, or contracts signed by a different entity than the one now registering.

Founders need to slow down just enough to avoid a bigger correction later. A fast submission is useful only if the underlying entity profile is accurate. If not, registration becomes the first place the mismatch shows up.

Here’s your move. Use the registration review to test whether these four points line up:

- the legal entity on the licence,

- the entity invoicing and signing contracts,

- the accounting period used in the books,

- and the ownership and control records held internally.

If those points align, the tax file is usually manageable. If they do not, the registration deadline has done you a favour by exposing the issue early, before the first return, audit query, banking review, or investor diligence process forces the same questions under more pressure.

Free Zone myths usually come from oversimplifying the rule. Transitional problems usually come from oversimplifying the business. Both are fixable if the company treats registration as the point where structure, records, and tax position need to match.

Practical Tips for a Smooth and Timely Registration

Most registration problems are preventable. They come from rushed preparation, not from difficult law.

A working checklist founders can use

Use this as a practical pre-submission review:

- Confirm the controlling date: Check whether your deadline is tied to the old staggered licence-month framework or the newer three-month incorporation rule.

- Match legal names exactly: The entity name on the licence, MoA, portal profile, and supporting documents should be identical in spelling and format.

- Review ownership records: Shareholder details and UBO information should be current and internally consistent.

- Choose the right year-end: Use the financial year-end the business can maintain in accounting and reporting.

- Centralise the documents: Keep one final set of approved files, not several draft versions across email and messaging threads.

A clean registration file usually reflects a clean company file. If your tax registration prep exposes gaps, don’t ignore that signal. Fix the root issue before submission.

What works and what usually fails

Founders often ask what the fastest route is. The honest answer is that speed comes from accuracy. Teams that submit once with complete, matching documents generally have a far smoother experience than teams trying to “get something in” and correct it later.

What tends to work:

- a single responsible owner for the submission,

- one verified source folder for all company documents,

- and an early internal review of signatory, ownership, and year-end information.

What usually fails:

- relying on an old trade licence copy,

- using passports that don’t match the latest records,

- and leaving the financial year-end as an afterthought.

Best approach: Do the document reconciliation before opening EmaraTax. The portal should be the final action, not the place where you discover inconsistencies.

If the company has multiple stakeholders, cross-border ownership, or a setup history that involved changes after incorporation, treat registration with extra care. The more changes an entity has gone through, the more important it is to reconcile the official record before filing.

Frequently Asked Questions about Corporate Tax Registration

Do dormant or zero-revenue companies need to register

If the company is a UAE juridical person within the scope of corporate tax, don’t assume inactivity removes the registration requirement. Dormancy and zero revenue don’t erase the entity’s legal existence. The safer approach is to assess the entity’s status based on its legal form and registration position, not on whether it traded recently.

What should freelancers and sole proprietors do

Freelancers and sole proprietors should first determine whether they are operating through a juridical person or as a natural person. That distinction changes the analysis. If you’re operating through a company, use the company’s legal dates and records. If your activity sits under a personal business structure, get specific advice on how the registration rules apply to that specific setup.

What if the trade licence is expired or under renewal

Don’t leave this until the filing window gets tight. If the licence is under renewal, gather the most current official documentation available and make sure the entity details still align across the file. An expired or inconsistent licence record can slow the process because the tax application depends on the legal identity being clear.

Can you change your financial year after registration

Possibly, but don’t assume it’s a casual amendment. Your financial year-end is tied to how the business reports and complies going forward. Choose carefully at registration stage, and only consider changes with a clear legal and accounting basis.

If you want a clean, founder-friendly route through UAE company compliance, Inpro Corporate Services L.L.C. helps businesses handle formation, licensing, PRO support, visas, banking coordination, and ongoing tax and regulatory administration across Mainland, Free Zone, and Offshore structures. For founders who’d rather avoid document friction and deadline risk, the practical move is to get the setup and compliance stack aligned early.